Value back in vogue

The benefits of focusing on attractively priced, well managed and growing businesses, irrespective of their inclusion in an index, continued to aid fund performance. Thus it was virtually flat in March (versus the index -1.8%), capping a strong quarter in absolute and relative terms with a gain of over 10%, again beating the 5% gain by the index. These returns have been accompanied by low volatility (see page 3) - achieved through a combination of a valuation discipline that sets the entry and exit prices and the focus on quality businesses. Not surprisingly, stock selection has been a consistent factor behind the outperformance, both this year and previously. Given the continued rich equity valuations in several parts of the developing world it is timely to outline where the fund is still able to find attractive opportunities as well as the

risks it is looking to avoid.

In the first quarter emerging market equities underperformed developed, with the MSCI Emerging Markets index -1.6% in dollar terms, versus a rise of 10% for the S&P 500 and 9% for the Nikkei. This should not come as a major surprise. One of the problems that face investors is the high valuations that exist in certain pockets of emerging markets having been boosted by record low interest

rates. Investors now need to be much more selective. In recent years money has focused on growth at any cost. We are entering a period where the value investor is now likely to prosper. This should hold the fund in good stead. Fortunately the emerging market universe is a deep enough asset class, ensuring there are enough opportunities that still fit the fund’s investment remit, and allowing it to avoid the over-inflated companies.

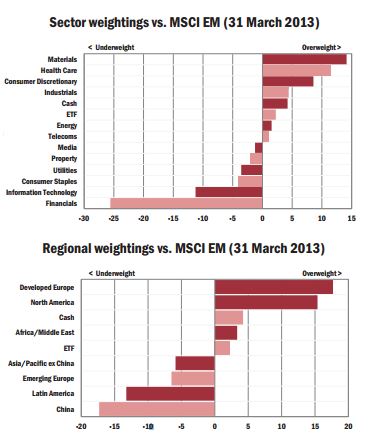

Bedlam’s emerging markets’ strategy has the added bonus of being able to capture attractively priced earnings growth through companies listed in developed countries (up to a maximum 35% of the fund) on the proviso that at least half of their profits or revenues are generated from emerging markets. This avoids any pressure to buy second-rate companies simply due to their place of listing. In addition, sometimes it is only possible to gain exposure to a favourable emerging market trend through companies listed in developed countries. Agriculture would be a good example. Currently the fund has an 8% exposure, of which 6% is in companies listed in developed markets (Agco, Syngenta and Yara). The lack of value in many parts of Latin America ensures that the fund remains underweight the region. While the Mexican economic outlook appears favourable, valuations – with the odd exception such as Genomma Lab - leave little room for earnings disappointment. Meanwhile, in Brazil discussions with several companies have pointed to slowing earnings growth. This comes at the same time as evidence points to interest rates having to rise from their current 7.5%, having been cut from 12% in 2011. Last month’s inflation hit 6.6%, breaching the top end of the central bank’s target range. Brazil is one of the worst performing markets this year, down over 10%. Latin America was reduced in the third quarter of last year with the cash being rotated into the cheaper opportunities in Asia ex-Japan. Here the fund is concentrated on stock specific stories in Hong Kong (18%) and Malaysia (11%), away from frothy markets such as Thailand, Indonesia and the Philippines.

These stock opportunities are increasingly being shaped by shifts in government policy. In China the government’s new policies are in the healthcare and energy sectors. There is a clear initiative to boost consumption and narrow the large income gap between rich and poor. Hence the desire to boost the number of people covered by social security payments such as health care. Given the ageing society this will significantly increase the amount that the government spends on drugs. Currently 1.5% of China’s GDP is spent on health care, versus 4% for education. To mitigate the increase in spend the government will most likely squeeze the price of basic and imported drugs. The beneficiaries are the domestic producers of high end generic drugs that have similar efficacy as those imported but are significantly cheaper (Sino Biopharmaceutical and CSPC Pharmaceutical). Meanwhile, the highly publicised pollution in Beijing has propelled the government to take action and promote clean energy such as gas. The policy involves increasing gas usage from 120b/mcf in 2012 to 230b in

2015. This will benefit companies such as Kunlun Energy (Petrochina’s 65% owned gas distribution arm), that are geared to the huge build out in the infrastructure required to import and transport gas.

The biggest risk for emerging markets equities lies in the bond market. Bond yields in many countries are at record lows, often ignoring weak fundamentals. Despite these huge bond inflows the growth in foreign reserves is virtually zero, down from over 20% two years ago (see page 4). If these bond flows reverse it would place pressure on their currencies, forcing interest rates up. Indonesia is already showing signs that interest rates will have to rise. Here reserves have fallen from $125b in mid-2012 to currently $104b. Their current account deficit has widened to 3.6% of GDP in the fourth quarter of 2012 with over 40% of the deficit being funded by short term money.

The major problems are in Emerging Europe. There are several countries with large current account deficits accompanied by high ratio of foreign debt-to-GDP (see page 4), most notably Hungary, Croatia, Ukraine and Poland. Turkey and South Africa also have major headwinds with large current account deficits. Despite the risks, Turkey’s 10-year domestic government bond yield trades at

6.6% (10% in 2010) and its equity market trades on a PE of 17x. The portfolio continues to avoid those countries, instead focussing its 12.4% weighting to Emerging Europe in a handful of companies listed in a diverse range of countries, such as Kenya, Israel and Russia.

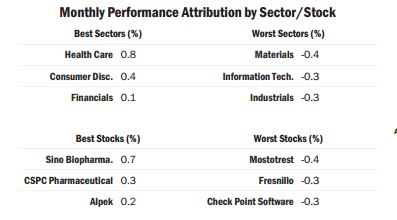

The fund saw some strong stock performers over the month, despite the decline in the index. Pleasingly this was spread across several sectors, most notably consumer discretionary (Shuffle, Padini and Samsonite), health care (CSPS Pharmaceutical and Sino Biopharmaceutical) and commodities (Goldcorp and Yamana Gold). Given our view that interest rates in many countries have reached unsustainably low levels, the fund retains a zero weighting to the interest rate sensitive sectors of financials and property. In many emerging market countries property prices are back up to historical highs having benefited from the abundance of cheap credit. The other notable event was the Bank of Japan firing off their equivalent of a monetary “bazooka”. Although this may have a positive kicker as Japanese savings move offshore in search of yield, a weaker yen is negative for the more industrialised exporting countries of Taiwan and Korea. The fund has zero weighting to Korea and 2.5% to Taiwan.

The best performer - up 21% for the month and 46% for the quarter - was

Sino Biopharmaceutical. Earnings were well ahead of expectations, driven by very strong sales growth; management signalled their confidence by doubling the dividend. Sticking with the Chinese pharmaceutical sector, CSPC Pharmaceutical’s full year results showed the benefits of the recent merger and its transformation into a faster growing, higher margin business. A subsequent meeting with management revealed that earnings growth will accelerate. Disappointing numbers from Lee’s Pharmaceutical resulted in the stock being sold, locking in a healthy gain for the year. The Malaysian retailer Padini reported solid earnings as it continues to expand through out-of-town stores. Shuffle reaffirmed their anticipated sharp acceleration in sales and operating margins on the back of their entry into the US slot machine and internet gambling markets. Gamuda looks likely to sell off its toll road assets, valued at approximately 20% of the market capitalisation. Following a strong earnings

announcement, Samsonite posted solid profits for 2012 with North American revenue remaining strong and Chinese demand showing a notable improvement in the second half. Sales are already ahead of budget and they are well positioned for additional sensible bolt-on acquisitions.

There were two sales and four purchases over the month. Shangri-LaAsia was sold having hit its target price. Of the purchases, Millicom is an African and Latin American telephony company; earnings are set to recover on the back of telephone banking and data/broadband growth. Old Town, the Malaysian coffee manufacturer and retailer, should see profits accelerate as its store outlets increase and it gains halal certification. Hutchison China Meditech has a strong consumer and pharmaceutical franchise. Both divisions are showing steady improvement with drug pipelines set to reach key milestones, boosting royalty payments. There is increasing evidence that Petrobras’s profits have troughed and should rebound as production growth resumes and the refining moves back into profit.

© Bedlam Asset Management