The Interest Rate Environment: Comparing High Yield Bonds and Bank Loans

Introduction

It has been over four years since the Federal Open Market Committee (“FOMC”) voted to lower the overnight rate at which banks lend to each other (“fed funds rate”) to a range of 0.00% - 0.25%. The FOMC has maintained this target ever since and Treasury rates of all maturities have persisted near record lows as a consequence. The prevailing environment has prompted many investors, Hotchkis & Wiley included, to question how long it will be before interest rates rise once again.

Based on discussions with economists, strategists, and other industry experts, the consensus view appears to be an inevitable rise in interest rates but with highly uncertain timing. In its most recent meeting minutes, the FOMC stated that it will keep the target fed funds rate at the current level until employment improves, inflation remains in check, and “other” market conditions comply. Such an opaque framework is unsettling. The timing and direction of interest rate movements, while nearly impossible to forecast precisely, has material implications for investment returns. Interest rate changes can affect equity markets but influence fixed income markets disproportionately—particularly when the change is unexpected. We recognize that there is a risk of rising rates, but given the headwinds facing the economy, we also understand that rates could persist at low levels for an extended period. Because our outlook for interest rates is rather ambiguous, we will contrast two credit instruments in a variety of interest rate environments: high yield bonds and bank loans. Our goal is to ascertain whether one, the other, or both are appealing investments in today’s environment.

The first step in our exercise will be to contrast the high yield bond market and the bank loan market. It will reprise the main conclusions drawn from the 2011 2Q Newsletter, “A Synopsis of the Bank Loan Market” (which we are happy to resend if requested). Once we have summarized the two asset classes, we will evaluate historical, current, and potential interest rate environments. Finally, we will analyze the behavior of the high yield market and the bank loan market in these different interest rate environments to determine whether we can make any sensible conjectures about the future.

Quick Review: High Yield Bonds vs. Bank Loans

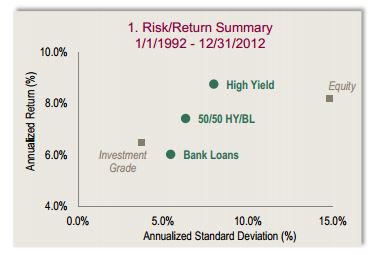

High yield bonds and bank loans are undeniably nuanced, but both are generally classified within the same realm: high yielding credit instruments. Because both asset classes exhibit greater default risk than investment grade bonds, investors demand higher yields. Because both asset classes are senior to equity in the corporate capital structure, they exhibit lower volatility than stocks. For investors seeking greater yields than those offered by investment grade bonds but who are unable or unwilling to tolerate the volatility of equities, both high yield bonds and bank loans may appear interesting.

High Yield Bonds

The high yield bond market began to proliferate in the 1980s. The basic structure is simple: a company (the borrower) issues bonds that are purchased by investors (the lender). In return for lending money, investors are entitled to receive payments. These predefined payments are fixed and made regularly (semiannually) until the bond matures or is called by the company/borrower. Typically, the bond has an 8 or 10 year maturity, and is callable halfway to maturity (i.e. 4 or 5 years from issuance). The high yield bond market is large, well-established, and quite liquid.

Bank Loans

The bank loan market, as it is currently structured, began to proliferate in the late 1990s and early 2000s. Its expansion coincided with the increased popularity of collateralized loan obligations (“CLOs”), which are bank loans that are pooled together and split into tranches with varying risk/yield profiles. Hedge funds, investment banks, and insurance companies were among the primary CLO investors.

The structure of basic bank loan is nearly as simple as a high yield bond: a company borrows money from a bank, which in turn, sells a portion of the loan to investors. In return for lending money, the bank and the investors are entitled to receive payments (pro-rata). Payments are made regularly (quarterly), but unlike a high yield bond, these payments are variable/floating and typically stated as a spread over a benchmark rate (LIBOR). Typically, the loan has a 5 or 7 year maturity, and is callable at its par value from day one. The bank loan market is private, which often translates into limited transparency and lower liquidity than the high yield bond market. Bank loans typically represent the senior-most portion of a company’s capital structure and are often accompanied by extensive covenant packages designed to protect the loan holder.

From the investor’s vantage point, the benefits of high yield bonds relative to bank loans include a knowable coupon rate, call protection for the first half of the bond’s life, and a highly liquid marketplace. The benefits of bank loans relative to high yield bonds include increased coupons in the event of rising interest rates, greater seniority in the event of default, and covenants designed to prevent destructive management behavior.

The Interest Rate Environment

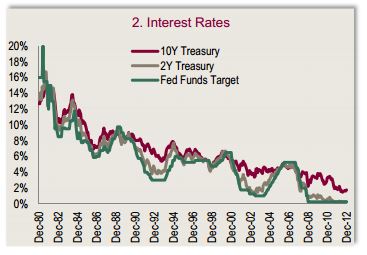

As depicted in Chart 2, U.S. interest rates have been in secular decline for more than three decades. This has provided a welcomed tailwind for bond investors, particularly those invested in high grade bonds/Treasuries which are interest rate sensitive (as opposed to high yield corporate bonds which are credit sensitive). With investment grade indices exhibiting yields well below 2%, we are skeptical that this market can replicate the compelling risk/return it has achieved in recent decades.

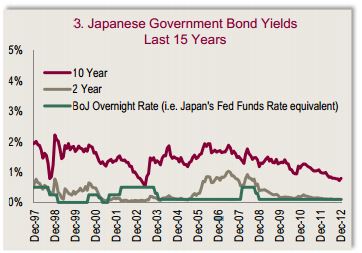

With the Fed funds rate essentially zero, there is negligible latitude for a further rate reduction by the FOMC. Should the Fed wish to ease monetary policy from here, they are most likely compelled to do so by alternate means (e.g. change reserve requirements). Most market observers believe that the FOMC’s “Quantitative Easing” program is a byproduct of persistent, record low interest rates; unconventional tools were required because traditional methods had been exhausted. Few things persist indefinitely; accordingly, interest rates are likely to rise at some point in the future. Nevertheless, FOMC minutes and slow economic conditions suggest that material rate increases are at least 12-18 months away, which could turn into several years depending on a variety of factors. The low interest rate environment in Japan (see Chart 3), which has persevered for the better part of two decades, is a popular reference for those that argue low rates may be here to stay. There are important fundamental differences between the U.S. and Japanese economies, demographics for instance, but it does show an enduring low rate environment is possible.

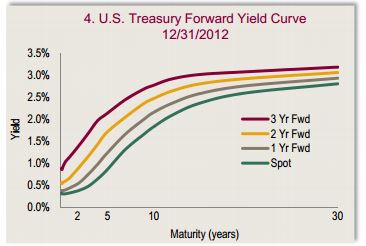

While the direction of interest rates is an important consideration, so too is the shape of the yield curve. The shape of the yield curve reflects expectations about future interest rates, and indirectly reflects expectations about economic growth and inflation. Chart 4 depicts the spot and forward yield curves as of December 31, 2012. The curves are upward sloping, which generally reflects expectations of rising interest rates, positive economic growth, and higher inflation. Based on the forward curves, the market expects the 10-year treasury yield to increase by about 30 basis points each of the next three years.

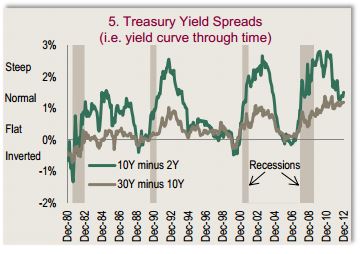

Unlike the level of interest rates over the past three decades, which have declined more or less consistently, the shape of the yield curve has oscillated between steep, inverted, and everywhere in between (see Chart 5). The shape of the yield curve has been a better gauge of economic growth than the level of interest rates. For example, note that each of the recessions shown in Chart 5 was preceded by an inverted yield curve, usually by about 18 months.

Types of Interest Rate Environments

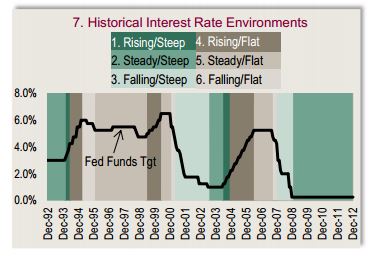

Before we explore how high yield bonds and bank loans perform in different interest rate environments, let’s first define the latter. As discussed previously, changes in the level of interest rates and the shape of the yield curve are both important considerations. Using these two variables, we can classify each interest rate environment into six basic categories. These are outlined in Chart 6.

Steep periods are defined as those where the 10 year / 2 year spread is above median (>1.2%) and flat periods are defined as those below median (<1.2%). The rising/steady/falling classification is simply determined by the changes in the federal funds target rate. This methodology is an oversimplification but it does provide an understandable and systematic means for dissecting various environments.

Chart 7 presents the interest rate environment historically, using these six categories. Over this period, the Fed was raising rates 20% of the time, lowering rates 26% of the time, and maintaining rates 54% of the time. The yield curve was steep half the time and flat half the time. Also note that for the past three years we have been in a Category 2 environment: steady interest rates and a steep yield curve. Historically, a Category 2 environment has been followed by a Category 1 environment: rising rates and a steep yield curve.

Bank Loans v. High Yield: Various Environments

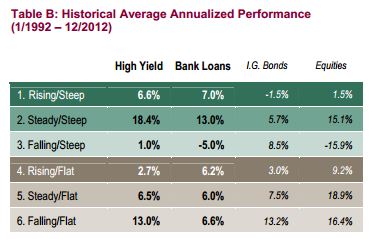

With the basic interest rate environments defined, the next step is to evaluate how bank loans have performed compared to high yield bonds in each environment. Table B summarizes the results, which include investment grade bonds and equities for additional perspective.

Historically, the high yield bond market is the only of the four asset classes to exhibit positive returns in each of the six interest rate environments. Excluding interest rate environment 3, the bank loan market has exhibited the most consistent returns across the various environments. Interest rate environment 3, falling rates with a steep yield curve, has been the worst environment for both high yield bonds and bank loans. This environment has historically coincided with the end/peak of economic expansion. As economic growth slows/contracts, the Fed lowers interest rates in an attempt to reinvigorate expansion (e.g. 2000 tech bubble, 2007/08 financial crisis).

We have been in interest rate environment 2 for the past several years—steady interest rates and a steep yield curve. Based on comments from the Fed, this environment could persist for some time. If history is a reasonable indicator, this would be conducive for both high yield bonds and bank loans. Our view, which is consistent with historical cycles, is that interest rates will eventually increase, and we will find ourselves in an environment with rising rates and a steep curve (environment 1). Short rates have typically increased disproportionately, which could result in an environment with rising rates and a flat curve (environment 4). Typically, both of these environments involve economic expansion which is constructive for credit markets.

Historically, the performance of high yield bonds and bank loans in these three environments has ranged from moderately positive to impressive—with bank loans tending to outperform when rates are rising and high yield tending to outperform when rates are steady. High yield bonds, however, perform better than many would expect given their fixed coupon feature. This is generally due to improving credit conditions and compelling bond valuations at the outset of such cycles.

Conclusion

High yield bonds and bank loans each have benefits and drawbacks but both are influenced by credit market dynamics. High yield has outperformed over time but has also exhibited greater volatility. The prevailing interest rate environment can exert meaningful influence on both markets, but confidently predicting the interest rate environment—let alone the timing of its transition—is a difficult endeavor at best. If history is a guide, however, a rising/steep environment seems at least as likely as any other, which should bode well for both the high yield and bank loan markets—particularly compared to investment grade bonds.

Whether we can control it or not, it is crucial to understand the environment in which we operate. Credit selection is the common thread in all environments that will continue to matter. So whether we are enjoying a tailwind or fighting a headwind, credit selection will remain our bread and butter. After all, “the only thing that overcomes hard luck is hard work” – Harry Golden (1902-1981).

Mark Hudoff, Portfolio Manager

Ray Kennedy, Portfolio Manager

Patrick Meegan, Portfolio Manager

Ryan Thomes, Portfolio Analyst

All references to High Yield bonds based on Credit Suisse High Yield Index; Bank Loans based on Credit Suisse Leveraged Loan Index; Investment Grade based on BofA Merrill Lynch U.S. Corporate, Government & Mortgage Index; Equities based on S&P 500 Index.

The indices assume reinvestment of dividends and capital gains, and assume no management, custody, transaction or other expenses. Data source(s): Tables - A: Credit Suisse, JPMorgan, CreditSights, H&W; B: Bloomberg, S&P, H&W. Charts - 1: Bloomberg, Credit Suisse; 2-4: Bloomberg; 5: Bloomberg, H&W; 6: H&W; 7: Bloomberg, FOMC, H&W.

All investments contain risk and may lose value. Investing in high yield securities or

bank loans are subject to certain risks, including market, credit, liquidity, issuer,

interest-rate, and inflation risk. Lower-rated and non-rated securities involve

greater risk than higher-rated securities. Bank loans, high yield bonds, investment

grade bonds, equities, and other asset classes have different risk profiles, which should be considered when investing. Historical interest rates are not indicative of future yield curves. Any discussion or view on a particular asset class or investment type are not investment recommendations, should not be assumed to be profitable, and are subject to change.

© 2013 Hotchkis & Wiley. All rights reserved. Any unauthorized use or disclosure is prohibited. This presentation is circulated for general information only, and does not have regard to the specific investment objectives, financial situation and particular needs of any specific person who may see this report. The research herein is for illustration purposes only. It is not intended to be, and should not be, relied on for investment advice. The opinions expressed are subject to change and any forecasts made cannot be guaranteed. H&W has no obligation to provide revised opinions in the event of changed circumstances. Information obtained from independent sources is considered reliable, but H&W cannot guarantee its accuracy or completeness. For Investment Advisory clients.

Past performance is no guarantee of future results.

© Hotchkis and Wiley