FOMC MINUTES LEAD TO MARKET GAINS

Equity markets resumed their upward climb last week, despite weaker than expected economic data. Minutes from March’s Federal Open Market Committee (FOMC) meetings indicated that officials remain committed to accommodative monetary policy, including the open-ended asset purchases of $85 billion per month (as well as the reinvestment of maturing principal from existing securities). This led to robust gains Wednesday in capital markets. For the week, the S&P 500 rose 2.3%, while the Dow Jones Industrial Average increased 2.1%.

Earnings got underway last week with releases from Alcoa, J.P. Morgan, and Wells Fargo. Each beat consensus estimates, although there is some concern that margins are compressing for the major financials. Both banks saw revenues dip below estimates. At this point in the reporting period, analysts expect a slight decline of 0.3% in earnings growth for the S&P 500 in the first quarter.

The National Federation of Independent Businesses (NFIB) reported on Tuesday that small businesses became more pessimistic in March. The NFIB Small Business Optimism Index declined 1.3 points to 89.5, as six of the index’s 10 components deteriorated. NFIB Chief Economist Bill Dunkelberg noted, “Overall, it appears that there will be little growth coming from the small business half of the economy; as the world economy slows, even big business may suffer.”

Small businesses saw the greatest weakness in labor market indicators, inventory investment plans, and sales expectations. The segment also continues to list taxes and government regulations as its biggest headwinds.

One of the few bright spots last week was a sharp drop in weekly jobless claims, although the series is quite volatile on a week-to-week basis. Nevertheless, initial jobless claims fell by 42,000 in the April 6 week to 346,000 – one of the lowest levels of the recovery period. The four-week moving average, however, actually increased by 3,000 in the latest report.

The most disappointing indicator last week was March retail sales, which contracted by the most in nine months. The 0.4% decline was well below the consensus estimate for a flat reading, driven by weakness across the measure’s subcomponents. Adding insult to injury, the Census Bureau revised both January and February lower.

Core Retail Sales

Source: Barclays Research

Although there was a 2.2% contraction in gasoline spending in March, other declines occurred across core sectors such as electronics, department stores, and health & personal care. According to Barclays Research, discretionary components such as electronics and department stores have contracted in every month of the first quarter, illustrating a clear cutback in spending by consumers.

Opinions vary on what drove weakness in the retail data. Some point to the abnormally cold March as one reason. Others believe the elimination of the payroll tax cut is filtering through to consumers. Whatever the cause, March’s results and the negative revisions to January and February led many economists to cut their outlooks for first quarter GDP.

In China, there were also several important data points that impacted markets.

On Monday, market participants were pleasantly surprised to see that consumer prices in China eased in March, following a period of rising inflation. The country’s official measure contracted by 0.9% in March, down from 1.1% in February. The year-over-year level declined to 2.1%, ending a steady uptrend that started late in 2012.

After the week’s conclusion, however, a triumvirate of Chinese data released late Sunday night disappointed market participants. Equity markets sold off sharply to start the new week as a result.

First quarter GDP in the world’s second largest economy expanded 7.7% year-over-year. This was 0.3% below expectations, and 0.2% below fourth quarter levels. Industrial production in March, meanwhile, expanded “only” 8.9%. While robust from an absolute standpoint, the reading was a full point below last month and 1.1% below expectations. Industrial product continues to trend downward after hitting a recovery peak of 15.1% in mid-2011.

Chinese consumer data also missed estimates, coming in at 12.6% for the month of March. The combination of disappointing data furthered investor concerns about China’s economy as it transitions under new President Xi Jinping. The MSCI China index is down 5.9% in 2013 through last Friday, compared to double digit gains in the US markets.

TAX DAY AS POLARIZING AS EVER

Tax season is once again upon the American population, and this year, just as in years past, people are less than enthusiastic. It is estimated that the average taxpayer contributed slightly more than $11,000 dollars to federal taxes in 2012 and those figures are on the rise. As might be expected in the current backdrop, however, not everyone shares the same opinion on taxes.

In fact, only 5% of the population actually professes a “love” for doing taxes. Another 29% of Americans say they “like” doing taxes. The reason most often given is the receipt of a tax refund.

On the other end of the spectrum, plenty have an utter disdain for the process of filling out a tax return. More than half of Americans either hate or dislike tax returns. The most commonly cited reasons are the complexity, inconvenience and concern with how the government spends the money.

Source: Pew Research Center

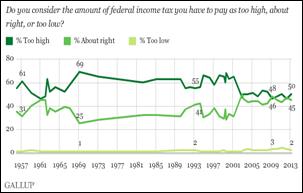

Despite strong attitudes towards the process, there is a sharp division between people who feel taxes are too high and those who think they are just right. Gallup surveyed 1,000 Americans and determined that 50% think taxes are too high, while 45% feel they are just right. That leaves a small percentage of the population who expresses an opinion that taxes are too low.

Source: Gallup

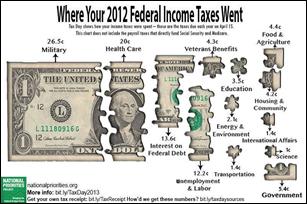

Where do those tax dollars go? Nearly two-thirds of every tax dollar is spent on a combination of defense, health care and interest on our federal debt, according to the National Priorities Project. Other major expenditures include unemployment costs, veterans’ benefits, education, energy, and food & agriculture.

Source: The Big Picture

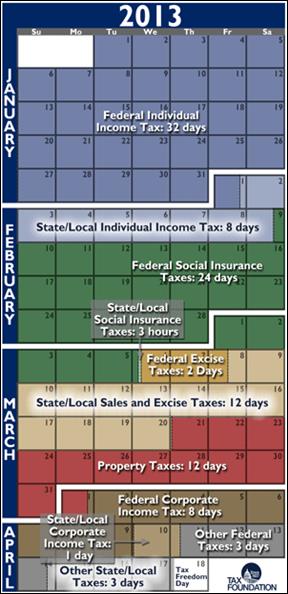

In order to pay the aggregate tax bill, including state and local, it will take the typical American 108 days of work in 2013, according to the Tax Foundation. By those calculations, come April 18, taxes for the entire year of 2013 will already be paid. That suggests there is more to be thankful for come mid-April than just completing your tax returns.

Source: The Tax Foundation

The Week Ahead

There are a handful of important economic indicators to watch for this week, spanning several sectors. On Tuesday, the consumer price index, housing starts, and industrial production are released. The Beige Book, a compendium of economic activity from across the country, will also be released by the Federal Reserve on Wednesday.

Earnings season continues this week with reports from Citigroup, Goldman Sachs, Coca-Cola, Morgan Stanley, Bank of America, eBay, Google, Microsoft, and PepsiCo.

Central banks delivering updated rate guidance this week include Turkey, Brazil, Sweden, and Canada. Turkey is expected to cut rates in its Tuesday announcement.

About Fortigent

Fortigent, LLC delivers a fully integrated and customizable business-to-business outsourced wealth management solution to banks, trust companies, and independent advisory firms. Services include a comprehensive investment platform with particular expertise in alternative investments, a flexible unified managed account program, and consolidated wealth reporting. Fortigent's web-based portal interface allows access to proposal and rebalancing tools, client portfolio reporting and accounting, as well as industry articles, research papers, and other practice management and business development resources.

For more information, please visit our website at http://www.Fortigent.com.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value

© Fortigent