One of the most important lessons I learned during my days at UCLA came from my freshman philosophy professor. He told us that should you find yourself engaged in a debate, the surest way to defeat your opponent is to attack his base principles. If those base principles aren’t fundamentally sound, any case built on top of it, no matter how convincing, is at risk of crumbling all at once.

You can only imagine how that impacted me, an economics student, who was simultaneously being taught that every single thing I was about to learn in the next four years was contingent upon one principle: that individuals act rationally. But that’s a story for another time.

When it comes to developing a set of concrete strategies and implementing the right asset allocation mix to combat inflation, we need to be mindful of our foundation. If inflation is extremely unlikely to occur any time soon, which -- SPOILER ALERT -- is the conclusion we’ll arrive at today, what use are strategies to fight it? Every point I’ll make about strategy will be irrelevant before I have a chance to even write it.

So before we get started, we need to do two things to build a philosophically-sound strategy. First, we need to figure out just what kind of probability we’re dealing with. And second, assuming the probability is small, we need to prove why it still matters.

What to look for when looking for inflation

The good news is that the second part of that is easy. Even if inflation is a tail risk, it’s critically important to have strategies at the ready or implemented on the margins to deal with it. If we’ve learned anything in the last decade, it’s that tail risk matters. Simply ignoring it is irresponsible risk management.

So while the probabilities may in fact be small, the potential costs in terms of wealth destruction could be monumental. I can think of few big picture risks more important and systemically-destructive right now than out-of-control inflation. Especially if it's accompanied by economic contraction.

Can you?

In a sense, every portfolio manager in the country is being forced to play a modified version of Pascal’s Wager. Either wild inflation will happen or it won’t, and you must bet on it or against. If you bet against it, and you’re wrong, the costs will be catastrophic or possibly career-ending if you’re in the business of managing money professionally.

The only rational solution, therefore, is bet on inflation. The trick is to bet on it in such a way that doesn’t get you killed should inflation never materialize and it turns out we are living in a prosperous era of endlessly low inflation that can be controlled as easily as loosening or tightening the faucet. We’ll reveal this trick on how to bet properly in Part 3.

Now that we’ve proven that this discussion matters, we can turn to the first objective of assessing probability. Unfortunately, this is a substantially more difficult task. It’s impossible to assign any sort of mathematically-derived quantitative metric.

The best thing we can do is monitor an array of warning signals. Depending on how many are flashing orange we can qualitatively assess how seriously we should take the threat and how aggressively we should implement our counter-strategies.

We begin with the most popular signal of them all.

The Bond Market

If you polled 100 investors about the single biggest warning indicator for inflation, at least half would point to the 30yr Treasury Bond. Once you tossed out all the yo-yos who think gold prices are indicative of future inflation (more on that in a minute) maybe 90% of the people left over would say that Treasury Yields are the best thing to watch.

Theoretically, this is true. We’ve all heard the campfire yarns about the “bond vigilantes,” a powerful Illuminati that supposedly will dump Treasuries onto the market en masse and drive up yields at the first whiff of inflation. They’re the philosophical free-market Yin to the world’s central banks’ Yang. But I’ve never actually met one of these guys. They may exist. They may not. Like the Higgs Boson, I’d kinda like to see one first before going all-in on the ways in which they’re supposed to make the world a safer and more awesome place.

We can also scroll back through history and put the bond market under an actual microscope.

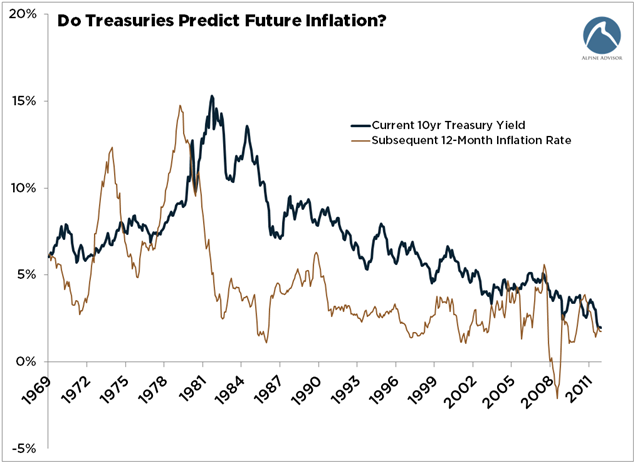

The following chart compares the current 10yr Treasury yield to the subsequent 12-month change in inflation. It’s a very crude experiment, but if Treasury yields can truly, accurately signal future inflation, then these two lines should move more or less in lockstep. As inflation rises, or is expected to rise in the future, the interest rates of today need to rise in response. That’s what we allege the bond vigilantes to do, right?

Obviously, there’s a difference in time inputs. Treasury yields are based on 10 full years of present value while inflation in this study and real-life is a year-to-year phenomenon. In fact, this philosophical distinction alone should make you re-assess using long-term bond yields to predict a few years’ worth of inflation.

Think about that concept for a minute. Why do we believe 10 or 30 years of present value will necessarily tell us what will happen in the next year or two? This is a powerful blow to the foundation of the case for using Treasuries as an inflation indicator.

You can also see that current Treasury yields generally lag actual future inflation. Using less awkward verbiage: Treasury yields move more in response to how inflation has increased in the recent past instead of how it will actually change in the future. We shouldn’t be surprised. This is how everything else works in the market. As it turns out, Treasuries might not be as good at predicting future inflation as we thought.

I want to tell you to pay attention to Treasuries. I really do. But with such a spotty track record as an inflation hound and with the market today so heavily manipulated by global central banks, I question their actual utility for such a task.

The corollary to this point -- a notion that should send a shiver up your spine -- is that just because interest rates are low, doesn’t necessarily mean that the probability of inflation is low. In 1974, inflation clocked in at 12%. Treasuries began that year yielding a relatively tame 7%.

I realize that none of you bond investors need more worries to keep you up at night. But if you think that we can’t get 6% inflation with Treasuries yielding 2%, think again. Investors in Treasuries (or bonds in general) must battle a two-headed risk monster: even if interest rates don’t rise in response to inflation, eviscerating their principal in the short run, they’re still getting paid back with less valuable dollars.

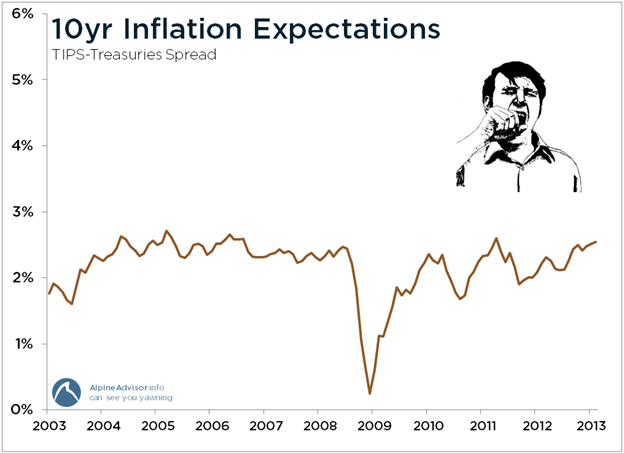

That brings us to the 5yr/5yr forward spread, which is what the Fed claims to look at to detect inflation worries. This spread is a much better indicator than Treasuries alone because of the way it’s constructed. It isolates the inflation portion of the yield.

I take a longer-term approach to portfolio management, so I follow a similar metric, the simple spread between 10yr TIPS and Treasuries.

Pretty boring, I know. But that spread has absolutely nailed inflation over the last decade. And it has done so while receiving zero appreciation amidst an atmosphere of abnormally dramatic rhetoric.

Keep in mind that this spread is forward looking, too. I just wish there was more data. We didn’t have TIPS in the 70’s. Will this spread accurately react to worry about inflation? I have no idea. But you’d better believe I’ll be watching anyway.

Gold

I can only say one thing about gold with confidence: gold is a very, very long-term hedge against inflation.

And when I say long-term, I mean a half century or longer. As a Dollar-denominated asset, it should (and does) move against the value of the Dollar denominating it. The problem is that it only does so reliably over extremely long windows of time.

Over the short run, gold does crazy things for crazy reasons. It went up over 1,000% in the 1970s, an era where the CPI “only” increased 160%. It then spent the next twenty years going down, an environment of unquestionably positive inflation. Since 2003, gold has been on a tear. The last decade has featured some of the lightest inflation we’ve ever seen in this country, as well as the only window since the Great Depression where we had a legitimate scare with de flation.

Gold prices are so volatile and noisy they are effectively useless at telling us anything about the very thing that we want to know about. Relative to gold, inflation acts slowly and deliberately.

Perhaps the last decade of 300% price appreciation in Gold really does suggest a few hundred percent inflation growth in the next decade? If so, it contradicts what the bond market and bond spreads are saying. It also contradicts our next two warning indicators.

Capacity Utilization

When we have nightmares about inflation, it’s systemic inflation that haunts us. Systemic inflation and dollar-devaluation are the things that can really ruin a person’s wealth.

We see individual pockets of inflation all the time and they’re as random as any other supply & demand driven market. Fortunately, systemic inflation is much easier to understand. To have systemically rising prices, several pre-conditions must be satisfied.

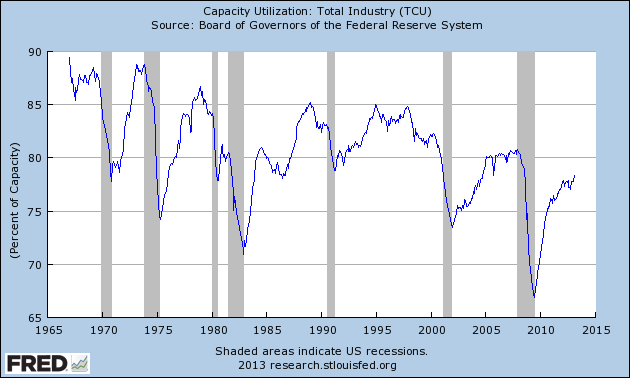

The first is capacity utilization. Theoretically, if prices start to rise and there’s still slack in the industrial system, capacity will increase to take advantage of the rising demand and higher prices. It’s pretty simple. When the price of widgets goes up, widget manufacturers respond by making more widgets. Make enough widgets and the prices stay constant or fall back closer to the point at which marginal revenue equals marginal cost.

The catch is that if industrial production is running at or close to full capacity, supply cannot meet demand. Rising prices are the only way to equilibrium. We see this all the time in specific markets like crude oil or corn. But if you’re interested in systemic inflation, it makes a whole lot of sense to keep your eye on systemic capacity utilization.

These days there’s still plenty of slack in the system and I have a really hard time envisioning some sort of inflationary scenario where domestic or global manufacturers don’t respond by making more stuff. We’ve got hundreds of years of data and economic theory that suggests that more supply is one of the best cures for rising prices.

Capacity utilization today is 78%. Back in the 1970’s during the specific windows when inflation was running hottest, capacity utilization was in the mid 80%s. It almost touched 90% several times during the decade.

We should recognize that high capacity utilization will not cause inflation in and of itself. But it’s the kind of thing that works in conjunction with other factors. If the Federal Reserve has stacked a room full of kindling with its aggressive monetary policy, capacity utilization at 85% would be like covering everything in gasoline. You’d still need a match, but just about anything could set it off.

I’d be extremely skeptical about any kind of inflation or inflation worry that wasn’t accompanied by a manufacturing sector that was running closer to full capacity. If prices were going up quickly and you had capacity to make more widgets, you’d make more widgets, wouldn’t you? You’d run your assembly line 24x7.

Wages

There’s another component that goes hand in hand with price inflation. Wages.

It is absolutely critical to understand that extreme, sustained price inflation cannot be sustained without corresponding wage inflation. I can’t over-emphasize the importance of this point.

You can get pockets inflation in specific places – crude oil or even real estate – without corresponding wage inflation. Consumers can juggle and re-allocate the spending of their dollars. But you simply cannot have systemic price inflation without higher wages to support it. Wage-earners are the ones who ultimately have to pay these prices anyway.

Therefore, trends in wages are one of the most important things look at if you’re watching for inflation.

These factors go hand in hand and create a virtuous (vicious?) cycle. Consumers can’t consume more than their wages allow. At least not forever. If their wages rise, they can either buy more stuff or buy the same stuff at higher prices. Prices can rise indefinitely so long as wages are rising too.

Watch wages. But also pay attention to some of the factors that influence wages. Yes, I’m talking about Washington D.C. There is a distinct political component to the inflation bogeyman and Congress may be a better place to watch for signs of it than the markets or the Federal Reserve.

Now that we have a list of foundation signals to monitor -- none of which are suggesting immediate inflation at present, I should add -- we can start to brainstorm about what might cause these factors to change.

In Part 2 of this series, we will discuss these potential catalysts in greater depth and begin building a basic philosophic framework for addressing the challenges of preserving wealth in inflationary environments.

Then, in Part 3, we’ll apply the final hardware and draw up a detailed blueprint for what to buy and sell while anticipating inflationary environments. Some assets will be obvious, others less so. None are outright bets on inflation – a key distinction for a risk management strategy – and none will get blown up should inflation not materialize. As a bonus, all of these strategies can be implemented on the margin with additional benefits.

Jeffrey Dow Jones is the founder of Alpine Advisor, a portfolio strategy service for independent investors and RIAs, and is also the author of the book, The Trade of the Decade: A Guide to Investing in the 2010s. He has spent the last decade working in the alternative investment industry and consulting with hedge funds and RIAs. He holds a degree in Business Economics from UCLA. His weekly market newsletter is available for free at AlpineAdvisor.info.

© Cornice Capital