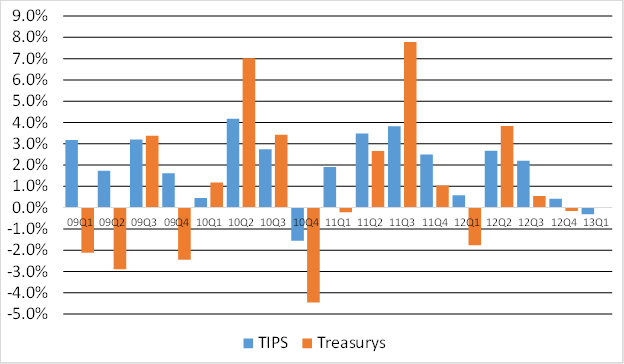

TIPS returns turned negative in the 2013 first quarter. The average loss was 0.31%, according to our estimates. By comparison, the return on comparable maturity straight Treasurys was flat.

This was only the second time since we began tracking TIPS in 2009 that the asset class has delivered a negative quarterly return. The previous negative quarterly return was in the 2010 fourth quarter, when both TIPS and Treasurys gave back some of the “flight-to-safety” gains that they had booked during the summer sell-off that year.

This is also only the third quarter since 2010 that TIPS have underperformed comparable maturity straight Treasurys. In 2010, flight-to-safety buyers made Treasurys the clear winner. Since then, investors have been looking for inflation-protection, driving yields on TIPS to negative levels across the maturity spectrum, except for the longest maturity TIPS.

Table 1

Yields, Spreads and Returns on TIPS vs. Treasurys

First Quarter 2013

|

TIPS |

Comp. |

Q1 Return |

Q1 Return |

||

|

13Q1 |

Yield |

Treas. Yld. |

Spread |

on TIPS |

on Treas. |

|

2013-2015 maturities |

-2.45% |

0.16% |

-2.60% |

0.23% |

0.10% |

|

2016-2023 maturities |

-1.48% |

0.96% |

-2.45% |

0.26% |

0.42% |

|

2025-2043 maturities |

0.08% |

2.59% |

-2.51% |

-2.02% |

-1.11% |

|

Totals |

-1.34% |

1.16% |

-2.50% |

-0.31% |

0.00% |

Source: Prices for TIPS and Treasurys taken from the Wall St. Journal. Yield and total return calculations by Lark Research

In the 2013 first quarter, returns on longer maturity TIPS were clearly negative and longer maturity TIPS underperformed straight Treasurys by much more than the short- and medium-term TIPs issues.

Those short and medium-term TIPS managed to eke out a slight positive return, as their prices rose by a little over one half of a point in the quarter and despite a slightly negative inflation-adjustment. The returns on these securities were positive because their coupons more than offset the amortization of purchase price premiums and the small negative inflation adjustment. Yields on these TIPS became more negative due to the modest price gains and also because they moved one quarter closer to maturity.

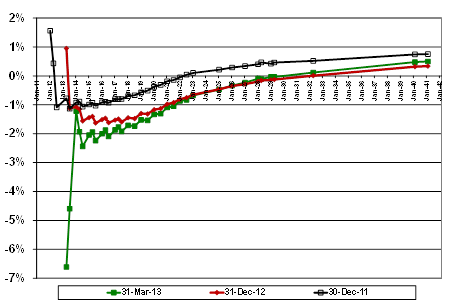

The slight shift in yields – more negative on the short-end and positive on the long-end – can be seen in the TIPS yield curve chart below.

Yield spreads between TIPS and straight Treasurys also widened to 250 basis points, the largest spread since we began tracking the sector in 2009. Most of the increase was due to a drop in TIPS yields deeper into negative territory. This suggests that investor expectations for inflation have risen slightly.

Chart 1

The TIPS Yield Curve

At December 30 2011, December 31 2012 and March 28, 2013

Source: Prices obtained from the Wall Street Journal and Barron’s. Yields calculation by Lark Research

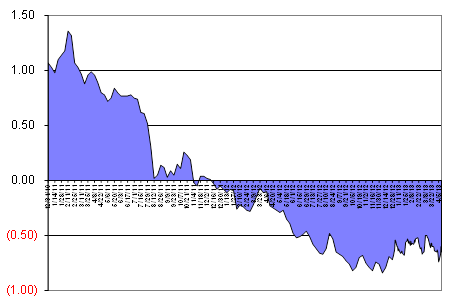

Yields on 10-year constant maturity TIPS appear to have bottomed out, as suggested in the chart below:

Chart 2

Yield on Constant Maturity 10-Year TIPS

December 31, 2010 to April 11, 2013

Source: U.S. Federal Reserve

As noted, TIPS prices ended the quarter slightly higher in the short- and medium-term maturities, but clearly lower in the longer-maturity issues. Spreads also widened. The decline in longer maturity TIPS was enough to push yields slightly higher, from the lowest yield level ever recorded on longer maturity TIPS of -0.06% in the 2012 fourth quarter to +0.08% in the 2013 fourth quarter. Although one quarter is not enough to define a trend, the price and yield action on TIPS in the 2013 first quarter is consistent with the notion of an improving economy and the prospect that interest rates may soon begin rising again. The wider spread also suggests a modest increase in inflation expectations.

We have been here before, most recently a year ago, when stocks got off to a great start and the market began pricing in a return to economic normalcy. Those expectations were dashed by the summer, as the crisis in Greece and U.S. presidential elections heated up. It remains to be seen whether some new crisis will cause another course change for stocks and the Treasury sector, including TIPS. If the economy continues to show steady improvement, we would expect that returns on TIPS and straight Treasurys will become more negative for a stretch, until yields begin to gravitate toward what the market views as a sustainable level.

Chart 3

Quarterly Returns on TIPS vs. Treasurys

2009 First Quarter to 2013 First Quarter

Source: Prices from the Wall St. Journal and Barrons; calculations by Lark Research

© Lark Research, Inc.