Any thoughts that the stock market was going to extend its rally were also shortened last week by a truly horrendous jobs report. In an economy that needs 250,000 new jobs each month just to replace retirees, we only had slightly more than 80,000 in March. The economists’ expectations were bunched around 200,000, so the disappointment in the air was palpable when the market opened and swiftly sank 150 points on the Dow Industrials.

With the number of people abandoning the workplace outpacing by far the new jobs created and the percent of citizens even participating in the labor market falling to a new low, it is easy to be sanguine about the financial markets’ prospects.

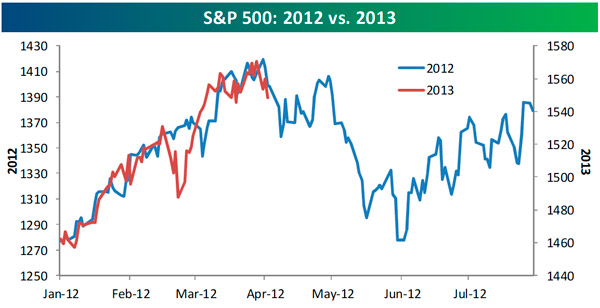

I have been regularly reporting on how this year’s stock market action has mirrored last year’s start – they have been virtual twins. That was great for the first quarter, as the S&P 500 zoomed higher on double-digit returns both years.

Source: Bespoke Investment Group

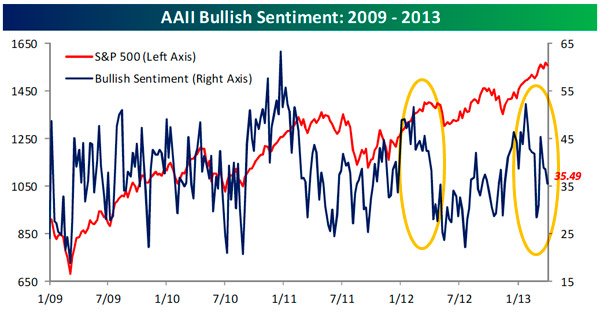

But if the duplication continues – look out below. Last year’s second quarter saw equities fall 9.9% from 4/2/2012 to 6/1/2012, erasing all of the first quarter gains. Investor sentiment seems to be signaling that this is about to happen again. Like last year, the AAII Bullish Sentiment Index is plunging heading into the new quarter.

Source: Bespoke Investment Group

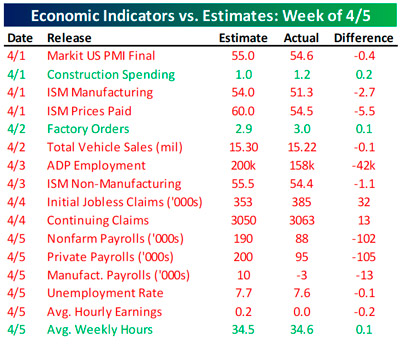

And just like last year, reports on the economy, as we have also been reporting, have been very weak. Few economic indicators are topping expectations and, like the jobs report, are instead disappointing. Last week only three of the sixteen were better than expected. Look at all the red ink:

Source: Bespoke Investment Group

Yet the sea of red, and even the jobs report, does come with some blue sky. The Federal Reserve easing, represented by over $80 billion in bond purchases per month, has generally been credited with responsibility for this year’s stock market rally.

The Fed’s actions, in turn, have, according to the Fed members’ own statements, been motivated by a desire to increase employment. Remember, the Federal Reserve has twin statutorily imposed responsibilities – inflation and employment.

This is another case of bad being good. Bad news on the employment front suggests that the Fed will not, contrary to the opinions of most commentators of late, be taking its foot off the economy’s gas pedal in the near future.

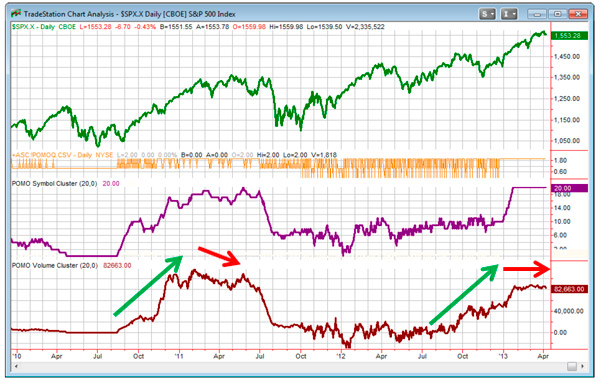

As we can see from this graph of both the Fed buying volume and the S&P 500, the increase in activity (the green arrows) was good for the stock market in both 2012 and so far this year. However, note that last year’s sell-off was preceded by a decline (red arrows) in the Fed’s buying (easing) activity.

Encouragingly, there is no similar slowdown this year. Instead, the Fed seems fully engaged in supporting the economy. With $20 billion being added each week, this makes it a potentially very different world from last year.

Source: QuantifiableEdges.com

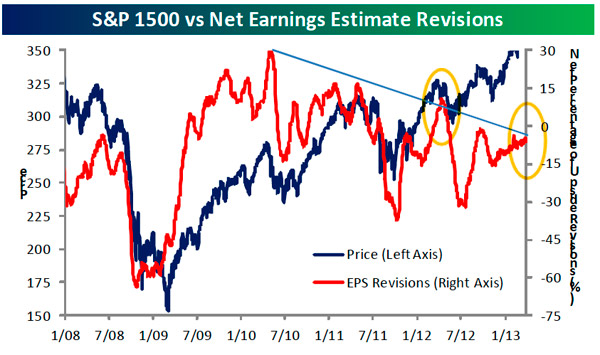

In addition, earnings are positioned differently this year. Last year, going into earnings reporting season, analysts were generally positive. When earnings disappointed, the market sold off severely. For most of this year, analysts have been negative in previewing the first quarter earnings reports. This does open up the opportunity for more positive earnings surprises that could restart the rally.

Source: Bespoke Investment Group

Only time will tell. Identical twins don’t always dress the same (except when they really want to confuse the rest of us). Many times identical twins will dress differently as each tries to assert his or her individuality. Let’s hope this is one of those times.

In the meantime, our technology keeps analyzing the numbers and calling the shots. And strategic diversification, owning five or more of our strategies that behave differently in the various market environments, is, in my opinion, the best defense for financial market double vision.

All the best,

Jerry

© Flexible Plan Investments