There were two very important central bank meetings last week, one from the Bank of Japan the other theECB. Bank of Japan press conferences have been soporific affairs for years with a few QE programs not leading to much and no changes to inflation targets. Deflation, a declining workforce and falling aggregate demand have been pretty much the unbroken story for the best part of two decades. Enter Abenomics last December, which promised higher inflation, active fiscal policy and more intrusive monetary policy. That’s when the stock market started a quick 10% rally for the last few weeks of the year. The one remaining piece for it all to work was whether the new Bank of Japan governor, Kuroda, could activate the rest of the central bank to start a new program. The dilemma was, would reactionary forces trump political intent?

We got our answer last week. The bank announced a radical program that includes: i) a doubling of the monetary base from now until the end of 2014 ii) maturity extension of bonds from less than 3 years to up to 40 years iii)JGBpurchases of around $56bn a month for the next 20 months…that’s 65% of the amount purchased by the Fed in an economy less than one third in size iv) purchases of more risk assets, including corporate bonds, ETFs andREITs…can you imagine if the Fed announced they were buying $2bn of ETFs every month? v) scrapping the banknote rule which prevented JGB purchases from exceeding notes in circulation…in the US they do already and by a factor of around 1.5:1.0 and finally vi) a more strident form of communication that intends to "drastically change the expectations of markets and economic entities."

Will it work? In the short term, we saw what you would expect from a QE launch. The yen weakened by 3%. It is now 20% devalued against last September’s level. Bonds rallied 1.5% as yields fell 12bps and stocks ripped by over 2%. In the longer term, Japan has a deflationary bias: a smaller workforce, with more, low spending retirees, and productivity gains. This combination usually leads to lower prices. The averageCPIover the last 20 years has been 0% and core CPI -0.1%. So the QE program will hit asset prices more quickly than broader economic prices. And hopefully domestic asset prices rather than a transfer through to overseas buying. We have seen Japanese initiatives come and go over the years. The stock market is still roughly 70% below its peak. But the combination of fiscal, monetary and inflation targeting has not been tried before. This is a critical juncture and so far so good.

ECB

The meeting at the ECB was the first since the Cypriot blow up where the central bank played a distinctly subsidiary role to the rest of the Troika. So the question was what would the bank do in the face of a flash CPI falling to 1.7%, unemployment rising to 12.0% and big declines in the nationalPMIs? The forecasts were also pretty dim. Here are the official 2013 forecasts compared to a year ago:

|

Projection Made for 2013

|

March 2012

|

March 2013

|

| Inflation | 0.9% to 2.3% | 1.2% to 2.0% |

| GDP | 0.0% to 2.2% | -0.9% to -0.1% |

| Government consumption | -0.1% to 1.3% | -0.9% to -0.1% |

| Fixed capital | -0.9% to 3.7% | -3.8% to -1.0% |

| Exports | 0.7% to 8.1% | -1.3% to 3.5% |

Source: European Central Bank Monthly Bulletin, March 2013, 2012

So in every case, severe downward revisions. The ECB had plenty of options: i) start using Structural Operations (HTto Lorcan Kelly at TrendMacro), which have vastly more flexibility than standard repurchase agreements and can include buying credit claims on non-financial companies and so bypass the banks ii) a rate cut iii)OMTexpansion iv) changes in collateral policies to encourage more bank lending. But while acknowledging problems in the economy, including the access to funding which is seriously impeding the liquidity transmission mechanism, Draghi offered no new solutions. All in all a quiet affair and the ECB did not even bother to post the transcript of the Q&A section on its Web site until the next day.

Fed Speak

There were a number of Federal Reserve governors on point this week. We didn’t read all of them but we started with Kocherlakota of the Minneapolis Fed, certainly one of the more thoughtful of the regionals, expressing real concern about unemployment. His position is the unemployment rate will be 7% until the end of 2014, that a more accommodative policy is required and the threshold unemployment target, the target required before any policy change, should be 5.5% not 6.5%. He also directly linked inflation to wage growth pressures and saw no real upside in thePCEfrom 1.6%.

John Williams, over at the San Francisco Fed, stated that “substantial improvement” in unemployment was needed before any changes but that he saw the possibility of tapering purchases some time in the second half of the year. That seems a little optimistic given the level of claims and economic activity more in line with a 2.5% to 3.0% growth for the year. Still, at least he’s consistent on what would trigger changes in policy.

Janet Yellen pulled no punches. She thinks unemployment is far above what it should be and that it should be “center stage” for everything theFOMCdiscusses. There's no doubt that she feels that there will be no let up in purchases until the “substantial improvement” threshold is met and she also gave a preview on the exit strategy: taper, stop, reduce and raise. And that will be a very long trip.

This year’s serial dissenter, Esther George in Kansas, flat out thinks policy is too accommodative and that asset prices in farmland, high yield and leveraged loans could be a real concern. She is also concerned, not unfairly, that it’s not realistic to ask bank regulators to identify all the risks of accommodative policy. Put these four speeches together and we can see the frustration the Fed is facing on managing growth and employment with only monetary tools. Our own view is that we’re in for many more months of accommodative policy and that it will take several 200,000 plusNFPreports to affect any tightening. Last week’s bond market strongly suggests they see it the same way.

US Economy

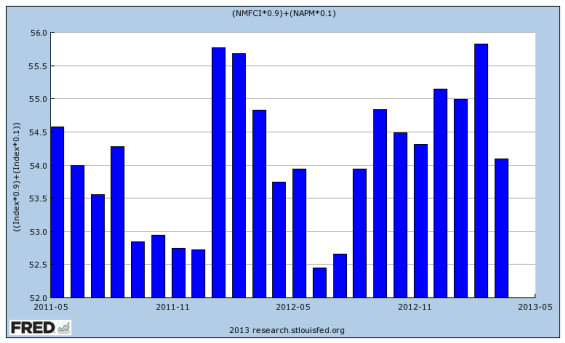

The worry for the US is that for the last three years, spring has brought a weakening in the broad economy and set back for stocks. The average correction for spring corrections has been around 7% to 17%. Is this going to happen again? The first signal of weaker activity came last week with theISMManufacturing and Non-Manufacturing indexes. Both track large employers which is where most of the action in employment and production is centered given the tender state of theNFIBhiring intentions. Here's a quick GDP-weighted look at the two ISMs together with the March downturn painfully evident:

Source: Federal Reserve Bank of St. Louis, Economic Research

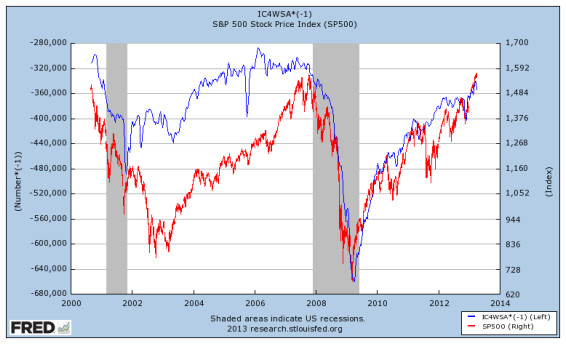

It was discouraging to see that both new orders and employment were down in both series. The claims number was also weaker at 385,000 after being in the 340,000 to 350,000 range for most of the last month. Here's the four week moving average against the S&P[1]:

Source: Federal Reserve Bank of St. Louis, Economic Research

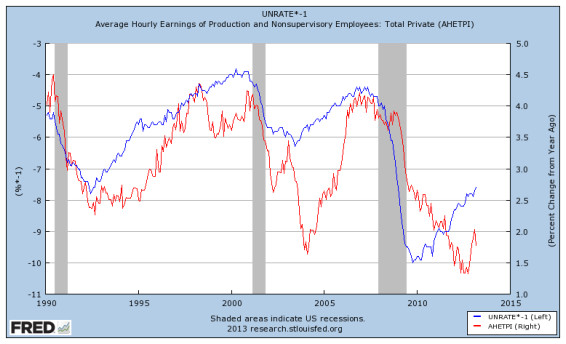

The NFPs on Friday were a clunker. While the headline unemployment rate fell, the number of new NFPs fell to 88,000, the lowest level since last June. The participation rate fell again and the labor force shrank. It’s now half a million smaller than the level of last December. Here's the unemployment rate and hourly earnings. As expected the increase from last month has reversed.

Source: Federal Reserve Bank of St. Louis, Economic Research

We would be wary of another few weeks of disappointing numbers given the stock market’s affinity for good jobs numbers.

Bonds

The GT10 has now backfilled its entire move from December 31st. We saw another point in return over the week as yields dropped 20bp. As of Friday mid session, the 10-year touched 1.69%. Over the last few weeks the 10-year returned 2.8% while equities ran flat. Investment grades,MBSand high yield were also mostly flat. This is not a robust, across the board bond rally. But the bull case for bonds is a combination of eurozone problems, weaker US stats, capital flows into the US dollar, many accounts simply underweight duration and the street generally short of inventory. The quality rally is evident too in i) the rally in JGB 10s, up 3.7% in two months and with the 10-year coupon dropping from 0.8% to 0.45%, and ii) Bunds up by the same amount with yields close to all-time lows at 1.21%. Looking at the US Treasury market from a world view, then, yields at 1.75% look very attractive! From a technical point, 1.70% on the GT10 looks like a bottom. But any more slack in the economic reports, yet alone a geopolitical scare, and we could see more bond upside.

Equities

For the last two months the market has settled into equilibrium of around 1500 to 1570 with the bias very much to the upside. It has been one of the most robust markets in the world with a near straight line up and YTD performance of +9%. Other markets have outperformed, particularly Japan which is up 21% in local terms but only 10% after adjusting for the weaker yen. The US market near term performance has been remarkable but remember we’re only just over the level of several years ago.

The difference between now and 2007 is that profits are higher, yields up and most of the market is cheaper. Investors seem to be in two camps: 1) the can't quite believe it but don’t want to miss it and 2) the it’s fine and use any dips to add exposure. We’re in the latter and have been for some months. There's very little bearish sentiment and none of the innate nervousness we’re picking up from the bond market. The upcoming earnings season will be a test. No one wants to sell ahead but if some of the estimates are revised as a result of the recent weaker economic news, we will see a correction opportunity.

Bottom Line : We peeled some of our equity exposure back mid-week and spent some money on bonds and duration assets. We also traded treasuries during the week. But we’re still over weight in equities.

Sources: Bloomberg, Capital Economics, CRT Ader, Economist Free Exchange, Federal Reserve Bank of St. Louis, IMF Fiscal Monitor, Federal Reserve Bank of Kansas, Federal Reserve Bank of New York, Federal Reserve Bank of Philadelphia, Federal Reserve Board, Bureau of Labor Statistics, Bureau of Economic Analysis, US Department of Commerce, ISI, J.P. Morgan Market Intelligence, High Frequency Economics, Pantheon MacroEconomic Advisors, ISM Chicago, TrendMacro, Tim Duy’s Fed Watch, Bank of America, Merrill Lynch, Federal Reserve Bank of Minneapolis, Bank of Japan, CLSA, European Central Bank, Sentinel Asset Management, Inc.

[1] Standard & Poor's 500 Index is an unmanaged index of 500 widely held US equity securities chosen for market size, liquidity, and industry group representation. An investment cannot be made directly in an index.

© Sentinel Investments

http://www.sentinelinvestments.com