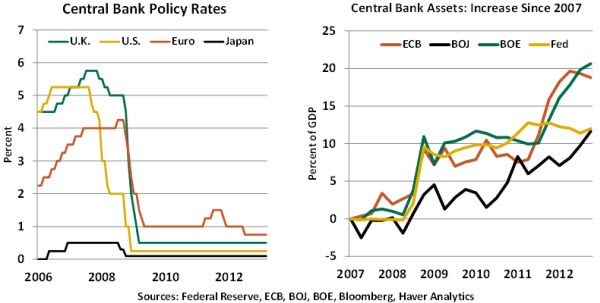

It is certainly a stretch to compare central bank campaigns to warfare. The stakes are much lower, and the weaponry is much less threatening. But the results of major central bank meetings this week revealed quite a spectrum of battle plans: one attacking aggressively, another waiting patiently and a third very much on the defensive.

Policy interest rates have been reduced to very near zero in many key markets. This forces central banks to consider alternative strategies as they seek to address unsettled financial systems and underperforming economies. The different postures they have adopted may reflect varying degrees of self-knowledge and knowledge of the enemy.

Taking the offensive this week was the Bank of Japan (BOJ), which announced plans to extend its quantitative easing program until it reaches roughly 60% of gross domestic product (GDP).

The Japanese outline was notable on several fronts. First, the size exceeded expectations by a considerable margin (it will ultimately be roughly three times the Federal Reserve’s large-scale asset purchases). Second, the program seeks to raise inflation to a target of 2% within two years. Many central banks have inflation targets, but they have always been thought of as maxima. This is the first time that policy will explicitly aim to increase the price level.

Finally, the Japanese effort will find the BOJ purchasing a wide variety of assets including exchange traded funds and real estate investment trusts. Central banks typically have carefully avoided overly favoring one sector versus another with their acquisitions, so this aspect will have to be implemented with care.

The BOJ aimed to send a strong market signal, and it was clearly effective on this front. As my partner Ieisha Montgomery wrote in ourMarch 29 weekly, the success of the BOJ effort will depend critically on fiscal and structural reforms whose implementation is far from certain. Nonetheless, the BOJ has chosen action over inaction, noting that past efforts have failed to rouse the country from two decades of difficulty.

Occupying neutral territory was the Bank of England (BoE). With U.K. GDP contracting for the fourth time in the last four years, there have been calls for the BoE’s Monetary Policy Council (MPC) to reopen its quantitative easing program. Minutes of recent MPC meetings reveal that BoE Governor Mervyn King favored this step but was outvoted.

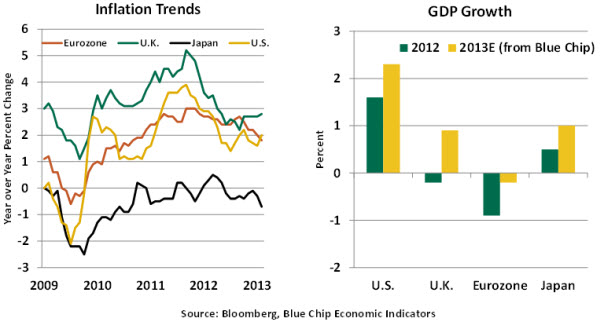

Among the reasons for the hesitance was inflation, which is running well above the official 2% target. To provide a little bit more room to maneuver, U.K. Chancellor of the Exchequer George Osborne recently announced changes to the MPC’s mandate. Higher inflation may be tolerated when the economy is struggling, and the range of allowable quantitative easing strategies will be expanded. Many analysts expect the new arsenal will be mobilized no later than July, when incoming BoE Governor Mark Carney takes the helm.

Hunkering down in the trenches was the European Central Bank (ECB). Amid deteriorating economic news and fresh off the crisis in Cyprus, the ECB declined to offer any additional support. President Mario Draghi counseled patience, noting that existing programs should facilitate improvement over time. But while the ECB’s efforts have restored a modicum of financial stability, they have not proven overly helpful to economic conditions.

There is a critical difference between QE programs in the United States and the eurozone. While American efforts have focused on bond purchases, ECB efforts have centered on lending directly to banks. In Europe’s case, the impact on economic activity therefore depends on banks taking funds obtained from the ECB and extending them to borrowers. But many European banks have been losing deposits and are trying to rebuild capital, muting this translation.

Mr. Draghi called on national governments and central banks to aid the cause, but the former are almost uniformly engaged in austerity and the latter are limited by the poor health of some local financial institutions. And some European policy-makers still see inflation as the only enemy raising concern. Unfortunately for the eurozone, Mr. Draghi does not have the fully compliant colleagues that his Japanese counterpart does, which limits him from taking the bold steps that many think are necessary.

While it is tempting to seek similarities in the challenges faced by leading world economies, there are important differences. Further, not all quantitative easing programs are the same; they operate through different channels based on the mandate of the central bank and the texture of the local credit markets. So some divergence of approach is to be expected, based on knowledge of the problem and self-awareness of what quantitative easing can and can’t do.

So at present, some central banks are advancing more forcefully than others. Time will tell whether an aggressive posture will produce a stronger economic advance.

March Employment Situation – Sustained Job Growth Is Not Here Yet

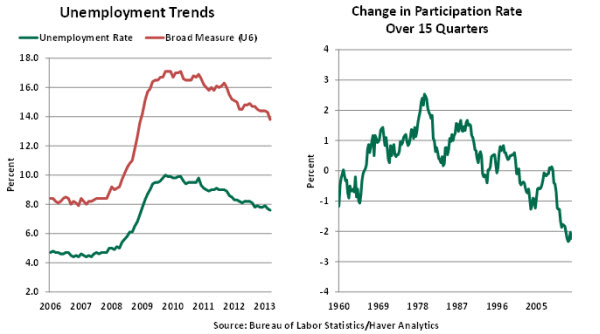

The 7.6% U.S. unemployment rate for March and lackluster 88,000 increase in payroll employment are disappointing headlines, and the details will do little to alter the Federal Reserve’s dedication to quantitative easing.

The drop in the jobless rate from February’s level (7.7%) reflects a decline in the labor force (employed + those looking for employment), not an increase in hiring. A decline of 350,000 part-time jobs led to a sharp reduction in the broad measure of unemployment.

The labor force participation rate slipped to 63.3% in March, a new cycle low. The teenage participation rate recorded a slightly larger decline compared with adult men and women. It is widely expected that a turnaround in the participation rate should follow as the economy expands, but a persistently low participation rate continues to haunt policy-makers.

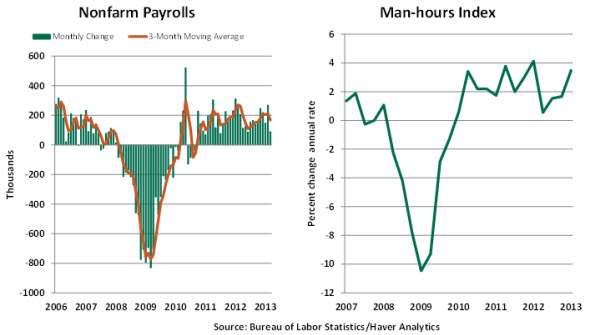

The soft 88,000 gain in payrolls was partially offset by revisions to payroll estimates of January and February that added 61,000 new jobs. Nevertheless, the latest three-month moving average at 168,000 is lower than the 209,000 gain posted in the three months ended in December.

On an industry basis, construction hiring rose 18,000 in March, continuing the upward trend that commenced last fall, consistent with improving housing market data. Factory jobs slipped 3,000, the first loss since September 2012. In the service sector, retail employment fell 24,000 following a string of gains recorded since July 2012.

Most of the 14,000 decline in federal government employment came from postal service employment, which is not related to sequestration. State government employment advanced 9,000, while that of local governments fell 2,000.

Average hourly earnings have risen 1.8% from a year ago. The man-hours index rose at an annual rate of 3.5% in the first quarter. Projections of real GDP growth for the first quarter now exceed 3%. Putting these two pieces of information together, it appears that productivity in the first quarter may not be impressive.

The economic recovery is middle-aged by historical standards but hiring is not on firm footing yet. At the cost of being repetitive, this feature of the labor market is persistent and remains the driver of the Fed’s policy. Market participants, for the most part, were carried away by recent Fed rhetoric which raised expectations of a tapering in large asset purchases sometime soon. The March employment report underscores that labor market fundamentals have yet to improve adequately to justify such a step in the near term.

China: Bubble, Bubble, But Where Is the Trouble?

At the beginning of the year, a number of heavyweight economists and financial gurus made convincing arguments that the Chinese real estate bubble was about six months from bursting. They predicted that this inevitable collapse would be a high-casualty event for the banking sector. However, this fearless prediction was also made at the beginning of 2012 and in 2011 as well, all without the much-anticipated reckoning. So with 2013 starting off with more of these prophecies, should they be taken with a grain of salt, or has something changed that should make us listen to Cassandra for a change?

To understand the Chinese real estate market requires examining the underlying forces. The first part of the price equation, as we learned in Economics 101, is the supply side, and in China there is no shortage of real estate for sale. Despite the talk of $50 million luxury estates littering the coasts from Beijing to Hainan Island, most of the properties on the market and under development are intended for the urban, middle-class worker. More than a decade of 10% annual economic growth has swelled the ranks of the middle class, and provisioning homes and goods for these millions of people is very much a growth business. Intuitively, it seems like creating enough supply would be the real problem; in fact, that is where we must examine the other half of the price equation – demand.

Unquestionably, the middle class wants to move to the Big City and live the Chinese dream of a home, a car and a family. Urban real estate is a social statement of success that can open many doors for a new entrant to the ranks of the middle class. However, over the past few years, a new demand factor has leapt into the pricing equation, and this is where the distortion comes in – speculation.

Chinese banks are notorious for offering low interest rates on savings (the benchmark deposit rate has been below 2% since 1996), as they are traditionally flush with cash. This leaves investors with few options for real returns without extending their risk appetite. This is where the real estate boom comes in. As an asset, property is seen as a one-way bet to appreciate (sound familiar?), and in the Chinese market there are few costs related to carrying properties – virtually no real estate taxes, utility expenses or other tradeoffs for sitting on a property. Investors looking for a return are now plowing money into real estate in the same way that other people might buy precious metals or art – little economic utility but a (perceived) store of value. Well-to-do families are now known for owning several houses though they only ever use one, and any excess savings are targeted toward gathering more properties rather than earning 35 basis points in a savings account.

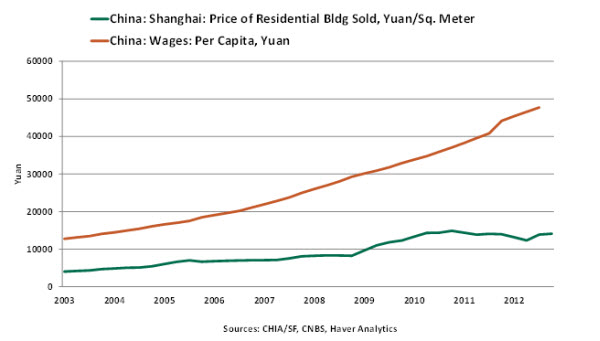

The speculative demand distortion is what has caused prices to rise rapidly and to such lofty heights, so much so that the average residential property is out of reach of the average worker. Even using the most conservative estimates of real estate costs, in metropolitan Shanghai, one year’s average wages can buy a mere 3.4 square meters of residential property – hardly a situation that invites more Chinese to get their first home.

Plenty of anecdotal reports suggest that the main force in the Chinese real estate market is now the speculator rather than the potential first-time homebuyer, and this demand distortion will not correct easily. The main concern for now is how to tamp down speculation without triggering a reversal of the inflow of funds – never an easy task. The government is experimenting with capital gains taxes on property sales and real estate taxes to create a carry-cost disincentive for speculators. But officials are approaching this with the utmost of caution because they know just how much is at stake. Given the vast differential between savings returns and the potential gains from expected real estate profits, it will take some significant push from the government to offset the current distortions. And as in so many cases, bubbles burst when challenged by a sudden force.

The opinions expressed herein are those of the author and do not necessarily represent the views of The Northern Trust Company. The Northern Trust Company does not warrant the accuracy or completeness of information contained herein, such information is subject to change and is not intended to influence your investment decisions.

© Northern Trust