Eye of the Beholder: Dissecting the Variety of Price-Earnings Ratios

Key Points

- Valuation is in the eye of the beholder … and a function of the version of earnings you plug into the P/E denominator.

- I'll share some warnings about certain popular P/E ratios and point out my favorites.

- The net is that I think the market remains relatively cheap.

Ask a bear about valuation and he'll likely say the market is very expensive. Ask a bull about valuation and he'll likely say the market is quite cheap. What gives? Assuming by "valuation," you mean price-to-earnings (P/E) ratio, the answer is in the eye of the beholder, and/or a function of the denominator (E, or earnings) you opt to plug in. There are three popular P/E ratios:

- Forward P/E (on subsequent 12-month earnings forecasts)

- Trailing 12-month (TTM) P/E (on most recent 12-month past earnings)

- Robert Shiller's Cyclically Adjusted P/E (CAPE)

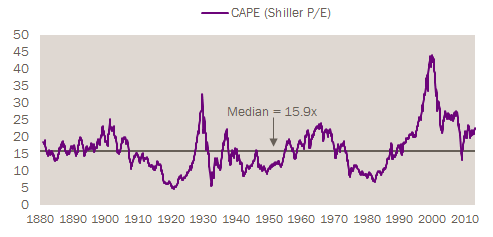

The CAPE uses earnings from the prior 10 years and has become a widely followed valuation measure. Yale professor Robert Shiller defines the numerator of the CAPE as the real (inflation-adjusted) price level of the S&P 500® Index and the denominator as the moving average of the preceding 10 years of S&P 500 real reported earnings, where the US Consumer Price Index (CPI) is used to adjust for inflation. The purpose of averaging 10 years of real reported earnings is to control for business-cycle effects. The CAPE is also sometimes referred to as the P/E10.

Before I share my thoughts on how to use valuation to assess the market (and which is my preferred metric), I want to pick a little at the CAPE and express some caution about following it too dogmatically. First, take a look at the chart of the CAPE below, all the way back to the 19th century. Comparing today's reading of 22.7 to the long-term median of 15.9 suggests the stock market is about 43% over-valued, assuming a mean-reversion to the "norm."

CAPE Signaling Stock Market Overvaluation

Data and methodology courtesy of Professor Robert J. Shiller (www.econ.yale.edu/~shiller/data.htm), as of March 27, 2013.

CAPE Crusader

There are several problems with the construction of the CAPE, detailed in a terrific report by Steve Wilcox for The American Association of Individual Investors posted on the Seeking Alpha site in 2011, from which I'll pull some data.

In their classic 1934 book Security Analysis, Benjamin Graham and David Dodd noted that traditionally reported P/Es can vary considerably because earnings are strongly influenced by the business cycle. To control for cyclical effects, Graham and Dodd recommended using multi-year averages of earnings. Shiller opted for a 10-year series.

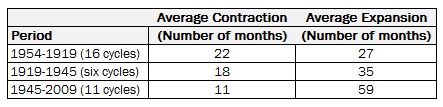

The problem with using a 10-year period for earnings is that the average business cycle only lasts about six years. More recently, recessions have become shorter and expansions longer (notwithstanding the long "Great Recession" which ended in 2009), as you can see in the table below. As a result, CAPE tends to overestimate "true" average earnings during a contraction and underestimate "true" average earnings during an expansion.

Source: National Bureau of Economic Research.

There are also problems with the deflator for CAPE's real earnings since the Bureau of Labor Statistics frequently changes the manner in which the CPI is determined, so, there's an apples-to-oranges problem using a static CPI within the CAPE.

Finally, both accounting standards and corporate taxation policies have changed significantly over time. Public accounting in the United States was still in its infancy in the late 1800s, and it's questionable how useful these early earnings numbers are to any analysis using them as inputs.

More recently, the move toward fair-value accounting standards resulted in security losses having a devastating effect on the reported earnings of financial institutions during the recent financial crisis. Yet that effect now appears to have been transitory. If an accounting item is deemed non-recurring, it's common practice to ignore it when determining underlying earnings (i.e., using "operating" instead of reported earnings). But CAPE continues to reflect the effect of non-recurring items for the 10 years that follow their initial recognition in reported earnings.

The punch line is that one has to question the validity of the CAPE long-term median when many of the major factors affecting reported earnings are peculiar to specific time periods. One final point: Even if you follow CAPE as a valuation tool, be mindful of the simple fact that the stock market can become "overvalued" and stay that way for a long time.

In the present bull market, the first month the CAPE crossed into overvalued territory (i.e. went above its median) was May 2009, just two months after the market's bottom, since which time the market has more than doubled. Even more dramatic was the cross into overvalued territory by the CAPE in February 1991, a mere nine years shy of the top of the great 1990s' bull market.

Shorter time frames

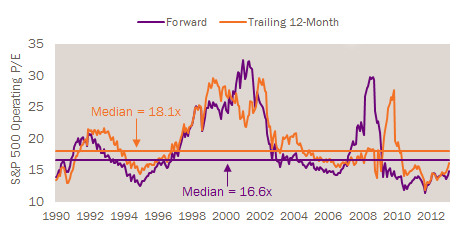

The other common P/E ratios used to value stocks look at a shorter time frame for earnings. Below are the forward P/E and the trailing 12-month P/E, both relative to their long-term medians, and showing a relatively cheap market. The peril of using forward earnings is of course the notoriously bad forecasting ability of the analyst community; however, there's presently a "cushion" built in given that the P/E is below its median.

Forward and TTM P/Es Signaling Stock Market Undervaluation

Source: FactSet, Standard & Poor's, as of March 27, 2013.

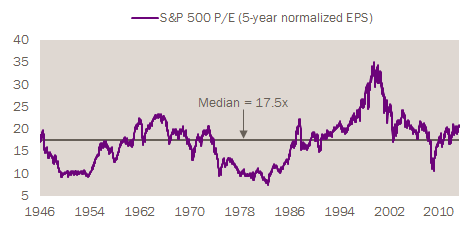

One of my favorite P/E ratios, created by Steve Leuthold, uses five-year "normalized" earnings in the denominator. What I like about this measure is that it looks both back and forward by using four-and-a-half years of historic earnings and two quarters of estimated earnings. In addition, the five-year span is closer to the six-year average business cycle than the CAPE. Finally, it takes the mid-point between reported and operating earnings, unlike CAPE, which only looks at reported earnings.

Five-Year Normalized P/E Signaling Slight Stock Market Overvaluation

Source: The Leuthold Group, as of March 15, 2013.

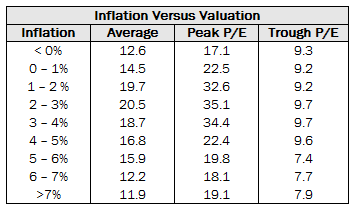

On this basis, the market is a few points overvalued—but there is a caveat: When looking at historic inflation zones, we're presently in a zone that's seen this version of P/E hit an average of more than 20, suggesting that today's valuation is about in-line.

Inflation Versus Valuation Signaling Reasonable Market Valuation

Source: Bureau of Labor Statistics, FactSet, The Leuthold Group, 1946-February, 2013.

Valuation, another way

Valuation can also be calculated in relative terms by comparing the stock market's value to bonds or the risk-free rate, and one way to do that is to compare yields. But since some companies don't pay dividends—and those that do pay out a small percentage of their earnings—dividend yields can understate companies' ability to boost shareholder wealth and stock-price appreciation.

A better measure of stocks' long-term potential is "earnings yield"—the reciprocal of the P/E ratio, or the ratio of earnings to price. You can then compare that to the yield on a bond or the risk-free rate.

In a recent memo from Oaktree's Howard Marks, he reviewed a few key points:

- The post-World War II average trailing P/E on the S&P 500 is about 16, for an E/P ratio of 1/16, or an earnings yield of 6.25%. Assuming a "normal" risk-free rate of 3%, the yield differential is 3.25%. The ratio of the yields is therefore 2.1 (6.25% divided by 3.0%).

- At the market high in 2000, the trailing P/E on the S&P 500 was about 32, for an E/P ratio of 1/32, or an earnings yield of 3.12%. The risk-free rate at the time was about 2%, so the yield differential was 1.12%. The ratio of the yields was therefore 1.6 (3.12% divided by 2.0%).

- Today, the trailing P/E on the S&P 500 is back to about 16, so the earnings yield is 6.25%. The risk-free rate is near-zero, but let's round up to 0.5% (Howard Marks rounded fully up to 1.0% in his analysis). As such, the yield differential is 5.75% and the ratio of the yields is 12.5.

To sum it up:

The yield comparison is highly favorable for stocks today and is actually the best it's been in the past century. Although much of stocks' current attraction is because interest rates are so low, history shows that when rates begin to rise from a very low absolute level they tend to be accompanied by rising stock valuations.

The moral of the story…

Valuation is often in the eye of the beholder, and one can likely find a version of the P/E to support any view. I do still side with the bulls on the market. We never recommend investors use any valuation metric (or any indicator for that matter) as a market-timing tool. I'm often asked whether investors should "get in" or "get out," often on the basis of valuation. Neither "get in" nor "get out" are investment strategies…they're gambling on a moment in time, whereas investing should be a continual process.

Important Disclosures

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

© Charles Schwab