Absolute Return Letter: The Need for Wholesale Change

“A comedian leading the largest party in Italy is simply a manifestation of a process that has been at work for some time and is becoming the new norm”

Patrick Barron, Economist

On 5 March 2013 the Dow Jones Industrial Average set a new all-time high, surpassing the previous high of 14,165.50, established back in October 2007. Only the stock market doesn’t seem to recognise that the world is a very different place today when compared to 5 ½ years ago. Many investors talk the bearish talk, yet they walk the bullish walk. This apparent inconsistency is a function of the widespread belief that central bank policy, whether emanating from Tokyo, Frankfurt, London or Washington, provides an effective volatility hedge, allowing investors to ignore the underlying economic and financial problems that continue to simmer. Chart 1 landed in my inbox a few weeks ago, courtesy of Simon Hunt. A chart often says more than a thousand words; it certainly does in this case.

Chart 1: Now and Then – 2013 vs. 2007

Source: Charles de Trenck, Transport Trackers. U.S. data unless otherwise indicated.

Deleveraging? What deleveraging?

Admittedly, not all governments have demonstrated as much profligacy as they have on Capitol Hill. By and large, it is an ‘old world’ disease. Faced with a private sector intent on deleveraging, governments from Tokyo to Washington have sanctioned a massive increase in public spending, and thus debt, in order to protect the economy from falling into an outright depression – a very Keynesian response to a balance sheet recession.

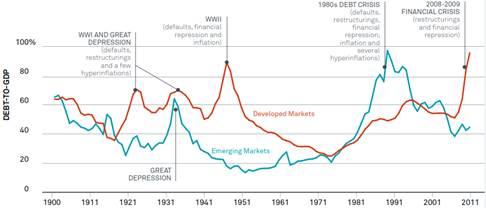

Meanwhile EM economies, still smarting from their own mistakes of previous regimes, have been much more disciplined and actually managed to keep debt-to-GDP levels largely stable since the outbreak of the credit crisis in 2007-08 (chart 2).

Chart 2: Govenment Debt-to-GDP in Developed and Emerging Markets, 1900-2011

Source: Blackrock, Reinhart & Rogoff.

Now, we all know that the public sector represents only part of the overall picture. The other two main sectors of the economy are the household and the corporate sectors. As Reinhart & Rogoff have repeatedly reminded us, it is total debt that matters at the end of the day. (As it happens, I only partly agree with that view. Governments can take a strategic view that corporates and households cannot necessarily afford to do, and they can at least partly control the cost of servicing the debt which the other two sectors cannot.)

With that in mind, let’s take a look at what has been achieved so far. The short answer is nothing! In the U.S. the household sector has managed to reduce its debt meaningfully but primarily due to write-offs and debt forgiveness. In Europe, large amounts of debt have been transferred from the private (financial) sector to the public sector. Yet, on balance and despite all the austerity talk, most countries are worse off today when compared to pre-crisis levels (chart 3).

Chart 3: Deleveraging? What Deleveraging?

Source: Boston Consulting Group. Total debt includes gvt., non-financial corp. and household debt.

1 Japanese debt through 2010. All other countries through 2011.

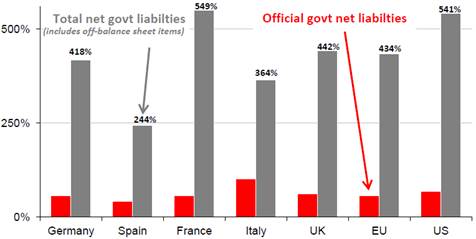

As if that wasn’t bad enough, if one were to include off-balance sheet items, an even bleaker picture emerges (chart 4). These items are largely age-related and include pension obligations, social security programmes, etc. With a rapidly ageing population in most OECD countries, this is destined to make an already bad situation much, much worse. Drastic action is desperately needed, but the appetite to do something about it just doesn’t seem to be there.

Chart 4: Total Government Liabilities

Source: Societe Generale Cross Asset Research.

Send in the clowns

I started this letter by quoting the brilliant Patrick Barron. Allow me to bring a longer excerpt from his recent paper ‘Send in the Clowns’ which sums up the situation quite succinctly:

“The Italians have just given more votes to a new political party, the Five Stars Party, with Beppe Grillo, a professional comedian as its spokesman. Caretaker Prime Minister Mario Monti, called a technocrat, was punished for attempting to instil some sort of discipline in the Italian budget. The electorate would have none of it.

“The Slovenians just threw out their prime minister for recommending what has come to be called ‘austerity’, meaning fiscally responsible government. Even the usually responsible Dutch have announced that they will not meet the European Monetary Union's goal of a three percent or less government deficit this year… Maybe next year… Or maybe never!

“The new prime minister of Japan has announced that he will appoint a new head of the Bank of Japan based upon the nominee's promise to drive the yen lower and generate more inflation. And in America Fed Chairman Bernanke just testified before Congress that he will keep interest rates at zero until unemployment meets his goal. Monetary responsibility? Ha!”

It is not only about monetary responsibility, though. Regrettably, the problems go much deeper than that. From where I sit there are (at least) two fundamental issues both of which must be addressed:

- The economic structure itself is fundamentally unsound, not only in Europe (where it is particularly bad) but elsewhere too.

- Policymakers, particularly those in Europe, are demonstrating a dangerous cocktail of ignorance and unwillingness; ignorance of how the economy and financial markets work and an unwillingness to address the structural problems we are faced with.

The comedy called Cyprus

I have long argued that the creation of the European Monetary Union was akin to reintroducing the gold standard. The eurozone member countries are effectively locked into a system very similar to the one that proved so hopelessly inadequate during the great depression in the early 1930s. A monetary union is quite simply the wrong model for a rapidly ageing Europe, but a combination of ignorance and stubbornness means that those in charge refuse to see the writing on the wall.

The last couple of weeks have provided ample evidence that the political leadership in Europe is utterly clueless as to how to resolve the crisis. If there were any trust left between the public and our elected leaders that has now been unequivocally broken with the disastrous handling of the crisis in Cyprus.

On the other hand, we also know now (if we ever doubted it) that the political leadership in Europe is prepared to do pretty much anything to save the euro. The fact that they were inclined to sacrifice deposits under €100,000 doesn’t bode well for the future of our continent. With capital controls now in place in Cyprus, a Cypriot euro is no longer the same as a German or Dutch euro. What will they do when the crisis moves to France (which it will do)? See here for some interesting observations made by JP Morgan on that subject.

It is a well known fact that European banks depend more on deposits for their funding requirements whereas U.S. banks tend to primarily use capital markets. The fact that European policymakers were prepared to sacrifice small depositors in Cyprus demonstrates a shocking lack of knowledge of this reality. How do they think depositors in other eurozone countries will interpret this blatant attack on private savings? At a time where banks need access to funding more than ever?

An invisible line in the sand has been crossed and there is no way back. Next time a bank in a major eurozone country runs into serious difficulties, there is likely to be a bank run, primarily because the trust was broken with the shambolic handling of events in Cyprus. As outgoing BoE Governor Mervyn King once quipped (and I paraphrase): “It is irrational to start a bank run but, once it gets going, it is perfectly rational to join in.”

Sadly, the travesty doesn’t stop there. Almost farcically, the London branches of the two troubled Cypriot banks were kept open during the early stages of the crisis, allowing many horses to escape before the stable doors were firmly bolted. In the early stages of the crisis it was widely expected that a hair cut of 20-30% on deposits over €100,000 would raise the capital required for Cyprus to receive the emergency funding - now the talk is 60-80%. Local Cypriot businesses stand to be the big losers from this comedy of errors. Many of them will go bankrupt whereas the Russian oligarchs will be laughing all the way to the next bank.

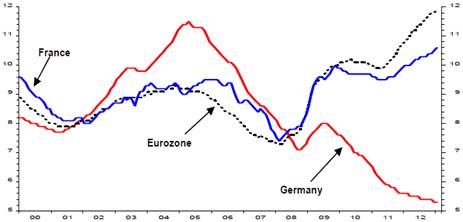

Chart 5: Unemployment in Europe

Source: Societe Generale Cross Asset Research.

The Germans, on the other hand, know exactly what they are doing. Faced with elections in September and an increasingly aggravated populace tired of funding fiscal problems in other countries, the German government obviously needs to tread carefully; however, despite all the spin, Germany is emerging as the big winner of this crisis and has a strong incentive to keep the eurozone intact. Yes, it has had to write a few cheques which happens to be pocket money compared to the competitive advantage Germany has gained vis-à-vis its European neighbours over the past decade. Without a common currency, Germany’s sovereign currency would have shot through the roof over the past few years. No, this crisis has been a big bonanza for Germany (chart 5).

Triffin’s Dilemma

The structural problems are not confined to Europe, though. If only they were! There are other problems that make the world inherently unstable. One of those is what is sometimes referred to as Triffin’s Dilemma. Given the U.S. dollar’s status as the preferred reserve currency of the world, the Federal Reserve Bank acts not only as the central bank to the United States but is effectively the central bank to the world.

It is the central bank’s duty to provide liquidity but, in the case of the Fed vis-à-vis the rest of the world, the liquidity is provided indirectly through the chronic current account deficit that the U.S. runs. (I first discussed this topic in the September 2005 letter – see here.) The U.S. government and central bank may be criticized publicly for its ‘reckless’ economic and monetary policy but, in reality, a chronic deficit is precisely what a growing global economy wants and needs.

Triffin’s Dilemma – first articulated by the Belgian-American economist Robert Triffin in the 1960s – suggests that the proprietor of the global reserve currency faces an inherent dilemma. It must run a structural deficit to feed the world with the liquidity it desires but, in doing so, it undermines its own currency and economy. Effectively the system self-destructs over time.

Triffin proposed the creation of a new global reserve currency in response to this dilemma. Creating a reserve currency which is independent of the U.S. dollar would allow the U.S. to reduce its external deficit without hindering global economic expansion (see more on Triffin’s Dilemma and his solution here).

Some will argue that the problem was fixed by President Nixon taking the U.S. off the gold standard in 1971. I disagree. The chronic U.S. current account deficits of the 1950s and 1960s created a build-up of substantial U.S. dollar reserves in Europe and Asia just like now. Unlike now, however, the creditor nations would redeem those dollars for gold, depleting U.S. gold reserves to the point where they became dangerously low. Today’s creditor nations redeem their dollars for U.S. Treasuries instead.

With the U.S. off the gold standard, the ability for the government to honour its obligations in gold is no longer an issue. It is instead the future purchasing power of U.S. Treasuries that is at stake; hence the system is still intrinsically unstable. There are (at least) four reasons for that:

- Running a chronic deficit undermines your credibility as a debtor nation.

- A disequilibrium where the currency issuer (the United States) suffers when the currency users (the rest of the world) benefit is likely to lead to conflicts over time.

- Having global economic expansion be a function of the currency issuer’s ability and willingness to run a chronic deficit is unstable in itself.

- Having the largest debtor nation in the world provide the world with the primary reserve currency is likely to add to currency volatility.

An emerging dollar bull market?

The last point is an important one. The U.S. dollar has experienced two major bull markets since it came off the gold standard (chart 6). The first one, lasting approximately 5 years from 1980 to 1985, caused massive problems in Latin America. The second bull market, which began in 1995, contributed to the meltdown in Asia in 1997-98. It seems like a strong U.S. dollar is not good for the world.

Chart 6: U.S. Dollar Index

Source: UBS Economic Insights, George Magnus.

More recently the U.S. dollar index has behaved very much like it did in the early stages of the 1995-2001 bull market (see here). George Magnus of UBS has recently produced a very interesting report where he makes the case for a strong U.S. dollar. Should that materialise, investors would be well advised to fasten their seat belts, as it could bring forward the advent of the next crisis.

Central bankers around the world are obviously aware of all these issues and this is where the story gets interesting. In central bank circles there is a growing realisation that monetary policy as prescribed over the past few years has become largely ineffective. The Bank of England buying another batch of gilts or the Fed acquiring yet more Treasuries has simply lost its va-va-voom.

Central bankers are therefore beginning to realise that they are running out of options in terms of propping up the global economy and something altogether different shall be required. It is in that light that the rumour mill is working overtime. Would it be far-fetched to expect a globally coordinated initiative whereby central banks step in with a groundbreaking new plan as to how the global e conomy and monetary system should be run?

For that to occur, our political leaders would have to be forced into a corner. That could only happen if the financial system became overwhelmed by yet another crisis. Policy makers simply won’t make the difficult decisions unless there is no other choice. Following that logic, central bankers actually have an interest in, and could do the world a favour by, ‘creating’ another financial crisis. Religiously targeting ZIRP is a good starting point. Near zero percent interest rates encourage risk taking to the extreme as we have seen over the past few years. Extreme risk taking leads to asset bubbles which will ultimately feed a crisis somewhere.

You may think that I have lost my marbles. I am not so sure. None of this is taken out of thin air. I have friends and acquaintances in many strange places around the world and this has come through one of the more trusted channels. Will it happen? I honestly don’t know but it is probably the best shot we’ll have at profoundly changing the monetary infrastructure of the world and for precisely that reason I hope it does happen.

Conclusion

So what would change if the world’s central bankers had it their way? For starters they would introduce a new reserve currency, not based on the U.S dollar. It would be good for the world, but it would also be surprisingly good for the U.S. On this side of the Atlantic, the euro as we know it today would probably cease to exist.

By the time the proverbial manure hits the fan, the majority of government debt in the troubled part of the world is likely to sit on the balance sheets of various central banks, making it relatively easy to control interest rates. This could pave the way for a major restructuring of government debt. I wouldn’t be surprised to see an overhaul of social security and retirement benefits at the same time. Even a quick glance at chart 4 above is enough to conclude that government liabilities are unsustainable in many countries. The largest banks around the world could be broken up at the same time.

Obviously none of this will happen unless the necessary conditions are in place. In plain English that means the patient has to suffer another crisis before the correct medicine can be administered. It goes without saying that all of this is speculation and may never happen but don’t bet on it! In the meantime, the U.S. dollar may be on course to enter another bull phase which could conceivably ignite the next crisis, or the crisis could be caused by something altogether different. Hard to say. The timing is equally difficult to predict. I don’t expect things to go pear-shaped within the first 12 months, but it’s anyone’s guess as to what happens after that.

In the short term, though, a continuation of the currently lax monetary policy is likely to lead to higher assets prices. The investor mindset is very much in risk-on mode at the moment, as documented by the surprisingly calm reaction to the crisis in Cyprus. Mind you, none of this incorporates the risk of an outright war between the two Koreas or an escalation of hostilities between Israel and Iran, just to mention two wild cards. Barring a Black Swan event, though, we are on relatively firm ground for now, but the seeds of the next crisis have already been sown.

© Absolute Return Partners LLP 2013. Registered in England No. OC303480. Authorised and Regulated by the Financial Conduct Authority. Registered Office: 16 Water Lane, Richmond, Surrey, TW9 1TJ, UK.

Important Notice

This material has been prepared by Absolute Return Partners LLP ( ARP). ARP is authorised and regulated by the Financial Conduct Authority in the United Kingdom. It is provided for information purposes, is intended for your use only and does not constitute an invitation or offer to subscribe for or purchase any of the products or services mentioned. The information provided is not intended to provide a sufficient basis on which to make an investment decision. Information and opinions presented in this material have been obtained or derived from sources believed by ARP to be reliable, but ARP makes no representation as to their accuracy or completeness. ARP accepts no liability for any loss arising from the use of this material. The results referred to in this document are not a guide to the future performance of ARP. The value of investments can go down as well as up and the implementation of the approach described does not guarantee positive performance. Any reference to potential asset allocation and potential returns do not represent and should not be interpreted as projections.

Absolute Return Partners

Absolute Return Partners LLP is a London based client-driven, alternative investment boutique. We provide independent asset management and investment advisory services globally to institutional investors.

We are a company with a simple mission – delivering superior risk-adjusted returns to our clients. We believe that we can achieve this through a disciplined risk management approach and an investment process based on our open architecture platform.

Our focus is strictly on absolute returns. We use a diversified range of both traditional and alternative asset classes when creating portfolios for our clients.

We have eliminated all conflicts of interest with our transparent business model and we offer flexible solutions, tailored to match specific needs.

We are authorised and regulated by the Financial Conduct Authority in the UK.

© Absolute Return Partners