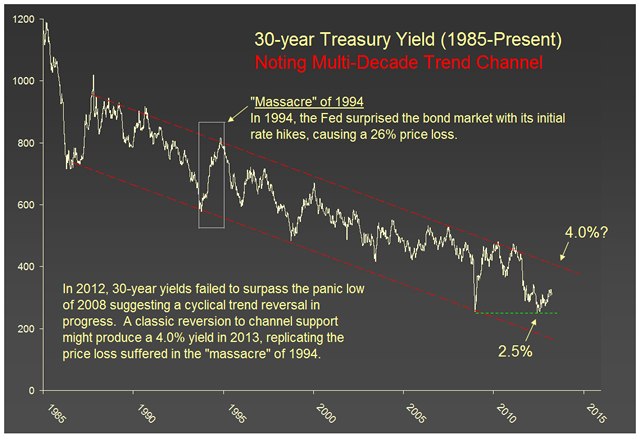

At last year’s Contrary Opinion Forum in Vermont, Michael Aronstein of Marketfield Asset Management outlined the case for brisk economic recovery as one of the most contrary of all possible opinions. With this thesis in mind, I recently examined the behavior of 30-year Treasury bonds, comparing today’s environment with that of 1994. See attached chart.

In 1994, the bond market was surprised by the Fed’s initial rate hikes, causing the 30-year Treasury yield to spike from 5.8% to 8.2% over a 13-month period. The price damage to those who bought near the top was about 26%. An analogous modern day rout might carry yields from 2.5% to 4.0% by July 2013. Remember, today’s low interest rate environment has increased the price sensitivity of long-term bonds. A yield swing of 150 basis points in 2013 is equivalent to a swing of 240 basis points in 1994.

Some might think that, in an age of “financial repression,” bonds are immune from normal cyclical moves. This could not be further from the truth, at least on the long end of the maturity spectrum. The post-crash environment has already witnessed a whopping 35% price reduction in the long bond – from December 2008 to April 2010 – while short-term interest rates were stuck near 0%. It should be obvious that the bond market presents a wide range of risk and return, even under a deliberate policy of artificially low interest rates.

So, why study the “massacre” of 1994? Because it pays to contemplate older analogies, especially those connected with the Fed-funds-rate cycle. And why emphasize price changes over yield changes? Because market price captures all that is known, or believed, about a security at a given time. Price swings cause the pain and euphoria that influence human behavior.

A classic reversion to channel support is not a farfetched scenario now that the Fed has articulated a 6.5% threshold on headline unemployment. Further declines in the household-survey rate might catalyze further bond-market losses, despite what the Fed says it will do.

© Charter Trust Company