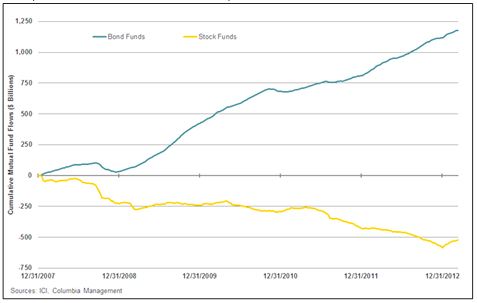

Given the strong flows into the bond market over the past few years, many pundits have pondered the beginning of the “Great Rotation” when bond investors begin to move money into the equity market. Investors fear that this shift could cause losses in bond funds as investors flee. Indeed since the start of the Great Recession in 2008, investors have plowed into bond funds as an alternative to equity volatility.

While many critics deny the potential for such a shift, we think it is important to review what it would take for such a shift to happen. We see a few plausible things that could cause this shift:

- Bond Valuations

- Recent Equity Returns

- Prospects for Growth

We have been observing that yields are “historically low” for quite some time. This has yet to be a deterrent of flows into fixed income in recent history. However, fixed volatility has been tame in recent years. If rates begin to drift higher causing price losses on interest-rate sensitive bonds, investors could begin to get spooked and begin to move money out.

Exhibit 1 (data collected from ICI, December 2012)

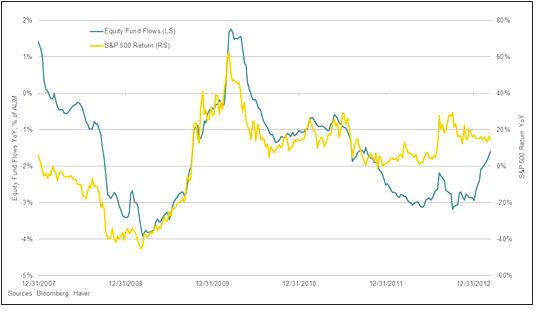

Secondly, equity investors have had a tendency to look in the rear view mirror when it comes to investing in stock funds. In fact, rising equity prices have tended to elicit greater flows into equity funds in recent years (Exhibit 2).

If equity markets continue to rise, this could give some investors the confidence to invest further into the sector, perhaps funding their purchases by selling bonds.

Exhibit 2

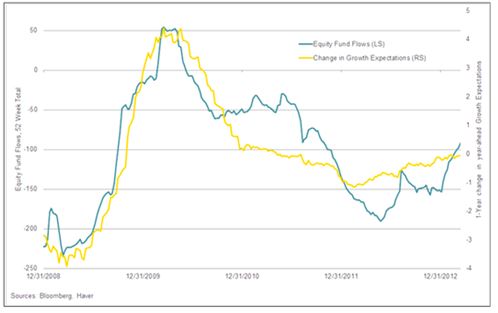

Lastly, equity flows have been closely correlated with growth expectations. It stands to reason that if investors expect better times ahead for the economy, then it may be an attractive time to invest in equities. The data do support this theory (Exhibit 3), and this could be a significant factor should investors begin to upgrade their growth expectations from their currently depressed level.

Each of these factors plays a role in determining how much money may leave bond funds and how quickly it may do so. More broadly, it highlights a key risk in bond investing today. Bond prices are high and yields are low, leaving little margin for error if conditions deteriorate. Therefore, it is more important than ever to avoid the potholes that may exist in the bond market. A portfolio rotation like this could be a potential pothole for bonds. Another risk could emanate from investors changing their expectations about the Fed, which has spent more time lately discussing the possibility of tapering their asset purchases (although they haven’t told us when!). Risk-related potholes could also come from fiscal policy in the U.S., where we still have not seen the full impact of tax hikes and sequestration. Internationally, Cyprus has also reminded us that all may not be well in the eurozone, an area with a tendency to spark bouts of market risk aversion.

Exhibit 3

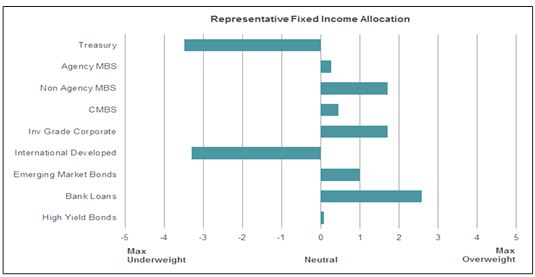

While we continue to believe risk management is paramount in this environment, we also recognize that the fundamental outlook remains well anchored. The U.S. economy has been outperforming expectations of late, buoyed by an improving labor market and a rebound in housing. Many emerging market nations in Asia and Latin America are also poised to post stronger growth this year than last year in our view. Therefore, we believe that fixed income opportunities remain, but investors should be picky and focus on fundamentals. In this environment, we like corporate debt exposure with a skew towards senior secured bank loans. We also like emerging market debt in countries with improving fundamental profiles. Nevertheless, we believe investors should take a more cautious view on areas that have potentially asymmetric downside potential. These include bonds with long durations or excessive foreign currency risk.

Exhibit 4

While the Great Rotation may still be a long way from happening, it simply highlights one of the many risks to bond investing in this environment. While the fundamental outlook remains solid for many sectors, the prices fully reflect that. In our view, a successful fixed income strategy in this environment is one that is diversified, flexible, and driven by bottoms-up research in order to avoid the potholes that the market may present in the future.

Disclosure

The views expressed are as of 4/1/13, may change as market or other conditions change, and may differ from views expressed by other Columbia Management Investment Advisers, LLC (CMIA) associates or affiliates. Actual investments or investment decisions made by CMIA and its affiliates, whether for its own account or on behalf of clients, will not necessarily reflect the views expressed. This information is not intended to provide investment advice and does not account for individual investor circumstances. Investment decisions should always be made based on an investor's specific financial needs, objectives, goals, time horizon, and risk tolerance. Asset classes described may not be suitable for all investors. Past performance does not guarantee future results and no forecast should be considered a guarantee either. Since economic and market conditions change frequently, there can be no assurance that the trends described here will continue or that the forecasts are accurate.

It is not possible to invest directly in an index.

The Standard & Poor's (S&P) 500 Index tracks the performance of 500 widely held, large-capitalization U.S. stocks.

This material may contain certain statements that may be deemed forward-looking. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those discussed. There is no guarantee that investment objectives will be achieved or that any particular investment will be profitable.

Investment products are not federally or FDIC-insured, are not deposits or obligations of, or guaranteed by any financial institution, and involve investment risks including possible loss of principal and fluctuation in value.

Securities products offered through Columbia Management Investment Distributors, Inc., member FINRA. Advisory services provided by Columbia Management Investment Advisers, LLC.

© 2013 Columbia Management Investment Advisers, LLC. All rights reserved. 154808