Cyprus proved, over the last two weeks, that markets often overlook the small stuff. Very few commentators we follow saw any of it coming and the theories that sprang up in the interim (Cyprus as vassal state to Russia, return to the Cypriot pound, imminent EU break up, twin euros in circulation, utter disaster for the economy, German intransigence and Schrecklichkeit ) were absurd.

Here's what happened and, then, more important, we’ll look at what it means. 1) Cyprus is a divided country and has had a UN force keeping two sides apart for most of the last 50 years. There are roughly 1,000 UN troops maintaining a buffer zone equivalent to 3% of the country, including some of its richest arable land. 2) It joined the EU in 2004 and the euro in 2008. So we have a small country, now playing in the big league, with an overvalued currency and low rates. Cue the next stage: fast catch up, real estate boom and rocket growth in banking.

And dead on cue 3) Cypriot bank assets quickly became over 700% of GDP, compared to 350% for the EU and 90% in the US. Much of the liability growth came from depositors. There were virtually no bond creditors and the equity ratio for its largest bank never fell much below 20:1, compared, say, to US banks at 10:1. Customer deposits were around 80% of liabilities, again compared to around 33% in some of our best US banks. On the asset side, much of the sector was exposed to Greek private loans and sovereign bonds.

So the tie in with the bad part of the EU, plus the razor thin equity buffer, plus the reliance on demand deposits, plus the size of the two main banks, led to a collapse in banking profitability, bad loans and anECBlifeline. At its peak, the largest bank was worth €17bn. You can have it now for €374m. 4) The ECB lifeline, in the form of emergency liquidity, was meant to be temporary. The Cyprus government asked for a more stable solution and got it, in the form of €5.8bn injection, but under conditions imposing losses on all creditors. With the equity tranche already wiped out, that only left the depositors. The agreements that the Cypriot negotiators agreed to was a 7% to 10% levy/haircut/wealth tax on all bank depositors, including small account holders who are usually insured.

Nearly there. The rest happens quickly. 5) Parliament rejects the deal. A new deal focused on just the two banks with the problem, not all banks. Insured depositors get 100c on the euro. Other depositors get large haircuts and an equity kicker (which is pretty worthless). The banks continue with their emergency liquidity. But, capital controls come into place and there are limits on cash withdrawals, check amounts and transfers aboard.

A final twist was that a hitherto anonymous bureaucrat said that the deal may well represent a template for future bank bailouts and that, yes, that included going after depositors. This was fully in line with an European Commission directive from a few months ago which said there must be "better protection [for] tax payers…[we may have to] interfere with creditors' rights…and [that the only protected liabilities were going to be] secured liabilities [and]…deposits…of less than one month." No fair complaining you couldn't find it on the Web site. So his comments were perhaps bad timing but otherwise pretty much on the money. The markets didn't like that one bit and hence the stories on two euros (one in Cyprus, one everywhere else), little guy depositors triggering bank runs and the contagion fear that all weaker banks would get the Troika hammer treatment.

With the picture a little calmer on Good Friday, we think the assessment goes like this.

- Capital controls are not great but they happen all the time and the world's second largest economy uses them with impunity. So why not the 95th? Article 65 of the EU Treaty explicitly allows exceptions to the free movement of capital when members need to undertake "prudential supervision of financial institutions."

- The two-euro story doesn't work. There's no black market for Cypriot euros and a Cypriot euro in Austria will still buy you a bite or two of Wiener Schnitzel. The US has a currency used almost exclusively by about ten other countries. In any of those the dollar is worth exactly…a dollar. Regardless of capital restrictions.

- This is not prelude to currency break up. It is prelude to tougher deals if you need a bank bail out and European banks certainly traded lower over the week. But funding stresses, such as the LOIS EUR, which measures the spread between interbank rates official rates, barely moved and remain well below the one year mean.

- Other stresses in the week included a rally in Bunds and German T-Bills going a bit more negative. But Spanish bonds held value and remain well above what they were at the beginning of the year. The euro fell but rallied. Equities fell around 3% but also recovered.

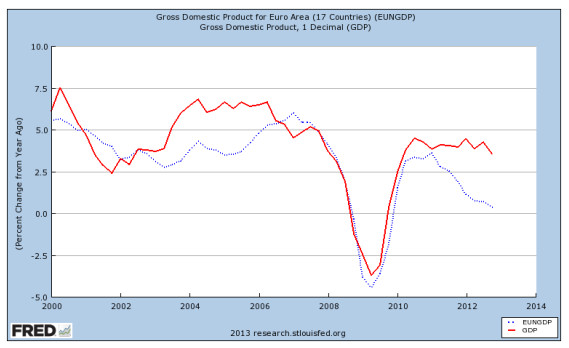

Put all this together, and, yes, we have a miserable outlook for the Cypriot economy. It could decline by as much as 16% and sets back growth for years. It’s part, then, of this bigger picture of really awful nominal growth in Europe. Here's the nominal growth of the EU and the US with the blue line of the EU falling again and again. (HTEconomist Free Exchange )

Source: Federal Reserve Bank of St. Louis, Economic Research

Growth is a huge problem as is attendant demand and unemployment. But perhaps we have slightly more certainty over how banks will be treated and another example, muddled maybe, of how the euro is determined to stay together. And that in turn makes us pretty confident about our European equity holdings, many of which are world class multinationals trading at very reasonable multiples.

FOMC

We stupidly scheduled a vacation when theFOMCmet. These are just such bundles of fun that reading up on them after the event is a real downer. Like watching Valentino Rossi pull a last corner overtake when you already know the result because Speed schedules GP races at ungodly hours after the event is long over. I digress. The Fed committed to unchecked purchases. Their 2013 projections now look like this:

|

Projection Made

|

GDP

|

Unemployment

|

PCE

|

Core PCE

|

| March 2013 | 2.3% to 2.8% | 7.3% to 7.5% | 1.3% to 1.7% | 1.5% to 1.6% |

| December 2012 | 2.3% to 3.0% | 7.4% to 7.7% | 1.3% to 2.0% | 1.6% to 1.9% |

| A year ago | 2.8% to 3.2% | 7.4% to 8.1% | 1.4% to 2.0% | 1.5% to 2.0% |

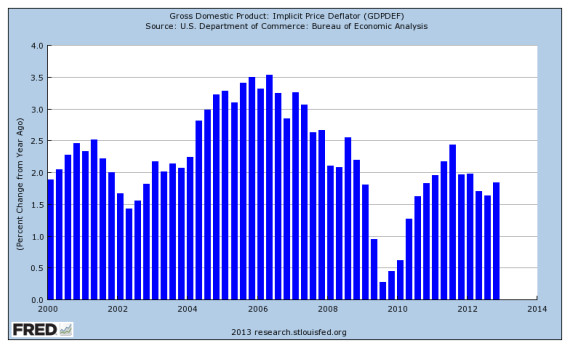

This means that, again, the collective estimates overstate growth, understate inflation and get employment about right. There was of course one dissenter, Esther George of Kansas with the familiar monster-in-the-closet inflation fears. Let's go hunting the snark inflation. Is it here in the GDP price deflator?

Source: Federal Reserve Bank of St. Louis, Economic Research

No.

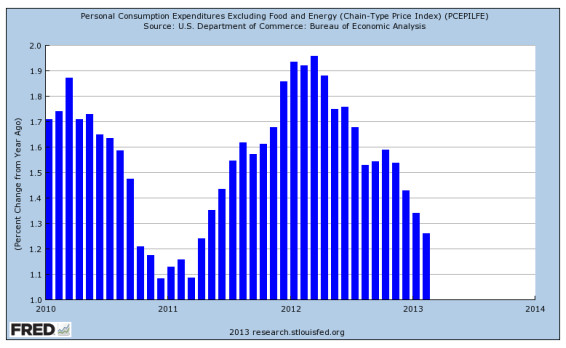

Is it here in the Fed's favorite measure of inflation, PCE core that came out on Friday?

Source: Federal Reserve Bank of St. Louis, Economic Research

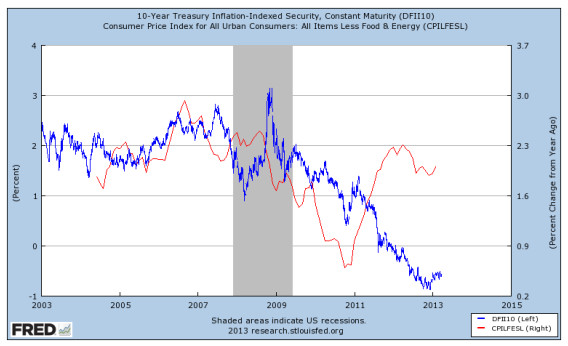

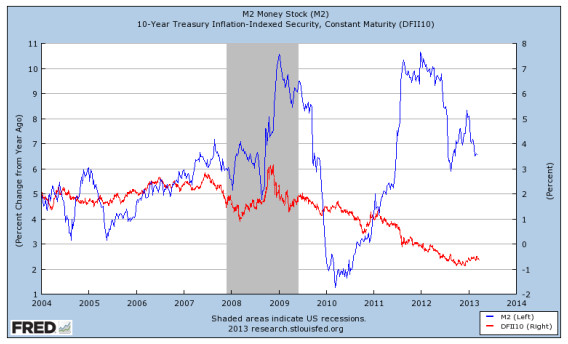

Why, no. Is it in the broad CPI and does the TIPS market care?

Source: Federal Reserve Bank of St. Louis, Economic Research

No and no. So the only explanation must be that the size of the Fed’s balance sheet is an inflationary time bomb and that it must come through to the real economy at some time. Any day now. And therefore the money story is the thing to look at…so here it is:

Source: Federal Reserve Bank of St. Louis, Economic Research

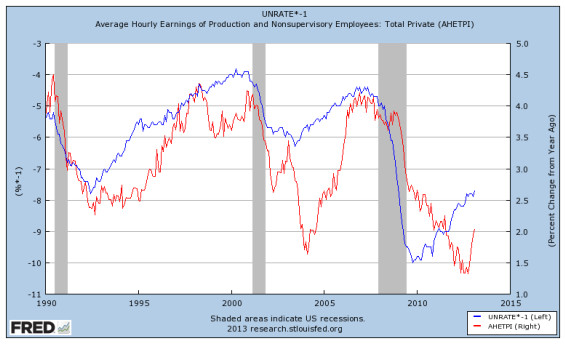

Not there either. Is it coming through in wages and a tight labor market?

Source: Federal Reserve Bank of St. Louis, Economic Research

No. That little tick on the right side of the hourly wages measure is still pretty meager and has a way to go before it disrupts the improvement in the unemployment rate. So it was nice, in the absence of any indicators that price or wages are affecting inflation, to hear Dudley of the New York Fed confirm that he would look for a real “substantial” improvement in the labor market before making any changes and that the Fed is falling short of the inflation target. And this was reinforced by recent hawk Kocherlakota from Minneapolis who stated that while he was all in favor of the 2.5%/6.5% inflation and unemployment target, he actually would like to see more “monetary accommodation” and that they should change the unemployment target to 5.5%. This is the same Kocherlakota who last May expressed concern about inflation at 2% and hypothesized that the then current labor market performance of 8.2% was close to “maximum” levels. It sounds like he stared into the abyss and didn’t like what he saw.

Again, what all this means is that despite gradual progress on the economic front, the Fed will look for more consistent signs of improvement before letting off the current asset repurchase program.

And in the economy?

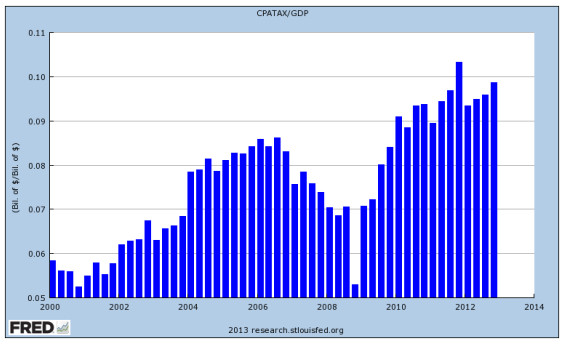

Generally the week had very disappointing consumer confidence numbers (surely the sequester plus delayed reaction to the payroll tax), Richmond Fed Manufacturing, where orders and delivery times fell and the ChicagoPMI, where production, new orders and backlogs all took small hits. The big reports for the week were the revised third estimate GDP numbers for Q4, which came in at 0.4%, up a bit from the original 0.1% but still very weak in the government sector. Without that, GDP would have been around 1.8%. We also saw the first glimpse of corporate profits (they're not in the first and second estimates). Here they are as percent of GDP, their second highest read in twelve years.

Source: Federal Reserve Bank of St. Louis, Economic Research

Some of that is due to lower taxes but a lot is the continuing story of a strong corporate sector that goes some way to justify the run up we have seen in stocks.

The other big number was personal income which rose 0.7% after the 4.0% decline last month which was, in turn, highly distorted by the run up in dividend income in the fourth quarter. It’s not a strong number and spending was probably propped up by another low savings ratio. Also compensation grew at about half the rate of personal income. The latter number was helped by income receipts on assets and rental income.

Bonds

The story for most of the week was a good old fashion flight to quality. The GT10 came in by around 10bps to finish at 1.84%, for a total return of 1.2%. As we’ve said before, these are markets where the coupon can be won or lost in an instant given duration and rate levels. The same story for Bunds which had a similar 1 point gain as investors sought safety. The Fed doves were out in force and the weaker numbers mentioned above let the market drift stronger. The new range for treasuries might well settle into a lower band of 1.75% to 1.85%…at least that’s what the technicals suggest. Throw in some quarter-end positioning, a long weekend, index rebalancing and the market was pretty quiet in other areas. The New Issue Market was quiet too with none of the big corporate names coming with new deals.

Equities

The new money into equities continues. It’s not a rotation. There's no big flood from fixed income money coming. But there has been a roughly $100bn run down in money market mutual funds that may well have found its way into equities. Mind you, that happened last year too and fizzled out by June. The market is holding up well. As we’ve mentioned before, the 1570 level is supported by $111 in earnings. Back when the market was at the same level in 2007, it was $89. So a fourteen multiple feels sound. Also if the S&P 500[1] had just kept up with inflation from 2000, it would be 2056 today, not 25% lower. We’ll certainly keep any eye on multiples.

Bottom Line: Using cash to trade treasuries. Over weight equities but not increasing.

Sources: Bloomberg, Capital Economics, CRT Ader, Economist Free Exchange, Federal Reserve Bank of St. Louis, IMF Fiscal Monitor, Federal Reserve Bank of Kansas, Federal Reserve Bank of New York, Federal Reserve Bank of Philadelphia, Federal Reserve Board, Bureau of Labor Statistics, Bureau of Economic Analysis, US Department of Commerce, US Dept of Housing & Urban Development, ISI, J.P. Morgan Market Intelligence, High Frequency Economics, Pantheon MacroEconomic Advisors, ISM Chicago, TrendMacro, Tim Duy’s Fed Watch, Bank of America, Merril Lynch, Federal Reserve Bank of Minneapolis, ECB Bank Structural Reform, European Commission, “Directive of the European Parliament and of the Council establishing a framework for the recovery and resolution of credit institutions”; United Nations; Sentinel Asset Management, Inc.

[1] Standard & Poor's 500 Index is an unmanaged index of 500 widely held US equity securities chosen for market size, liquidity, and industry group representation. An investment cannot be made directly in an index.

© Sentinel Investments