The conventional approach will continue to fail

The increases in the portfolio’s net asset value continue easily to beat the hardly exacting returns from the index. The fund has gained 10.4% gross for the year to date (to 22 March), vs. a 3.0% rise for the MSCI Emerging Index. This outperformance (replicated over rolling 1- and 3-year periods) has been achieved by choosing investments irrespective of index country or sector weightings or where they are listed, so long as they derive the majority of income and profits from developing countries. Whilst it would be hubris to forecast that this strategy will continue to be successful, it is certainly preferable to the conventional index- weighted approach, or one which confuses high economic growth with superior stock market returns.

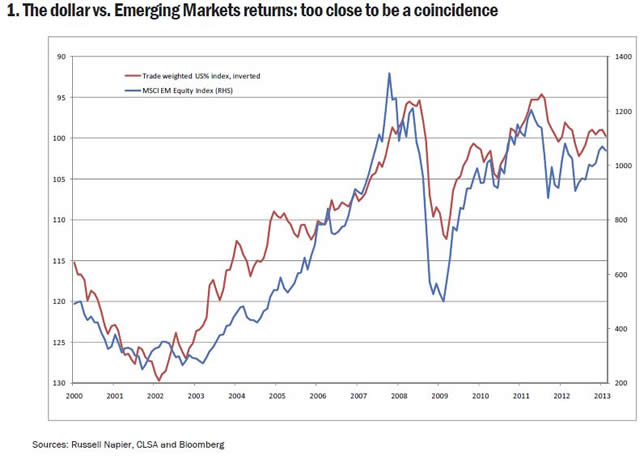

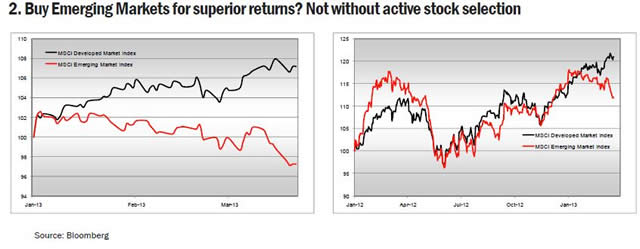

Investors continue to find it perplexing that emerging markets, which since the turn of the century have become mainstream for institutional allocations, are not producing the expected higher returns (see charts on p.4). Year-to–date the gain has been a mere 3% (in sterling terms), even as the developed markets returned 13%. One reason is currencies. As shown also on p.4, the index has an inverse relationship to the level of the trade weighted dollar. When this is weak, they tend to perform better; when strong, the converse applies. Whilst there are myriad causes, the important point is that this long-term relationship shows no sign of breaking, and there are few grounds to expect the dollar to tumble from the current fourth quartile of its 20-year trading range.

Then there is the construction of the indices; those in emerging markets are dominated by financials, property and commodities (which, because of foreign exuberance about the prospects in EM and institutional quasi-indexation, tend to be expensive). Thus the indices do not reflect the rapid increase in economic activity in consumption or services. Another reason for the disparity is that the direction of equity markets in developing nations, despite their generally higher economic growth and lower debt- to-GDP ratios, remains very dependent on events within the advanced countries. This is not due to better politicians in one than the other - even American presidents can have only a minimal positive impact on economic activity. (Conversely, politicians such as Presidents Chavez or Kim Jong-un can have a disproportionate negative impact.) Rather, it is because, out of necessity, central banks in the developed countries have wholly embraced the same trio of policies to improve their current and capital accounts: money printing, low interest rates and exchange rate manipulation.

The first two of these policies are not as readily available to most developing nations, yet are creating major distortions in asset prices within them. Currency manipulation too is often unavailable, because of currency pegs and other exchange rate policies. Moreover, the near collapse of the banking systems in developed countries has brought about a wholesale reduction in credit to developing countries, whilst their loose money conditions have resulted in hints of excess inflation, forcing governments such as in Brazil, India or Singapore to raise rates and tighten. In 2013, it is likely that EM returns will again be less than those of developed markets - if a conventional approach is followed.

Companies in slow-growth, developed countries are often better at sweating their assets, i.e. at producing superior growth in earnings per share. In 2012, according to JP Morgan, EM companies had earnings per share growth of 3.7%; US companies 4.3%. Many EM companies also lack capital discipline or a focus on maintaining profit margins. Again for last year, the average emerging market saw an increase in equity in issue of over 5%. In developed countries the amount actually contracted. A focus on margins has tended to dominate boardrooms in developed countries; those in the EMs focus more on grabbing market share, even if loss-making, in the expectation that once a leading position has been achieved, so better margins will result (similar to the fallacious Japanese approach of the 1980s).

Historically, valuations in most markets, developed and emerging, are high on traditional measures, from Cyclically Adjusted PEs (CAPE), Tobin’s Q (replacement cost) or consensus growth in earnings. Yet they are likely to remain high and even rise further, provided the advanced nations do not change their current central bank policies much. These policies entail no real attempts to control budget deficits (i.e. austerity), and are pro inflation, low interest rates and continued borrowing via quantitative easing as required. So long as all these continue to be probable, so the surprising pattern of spluttering economic activity globally, yet good stock markets, continues. Even so, it would be wildly irresponsible to chase the higher-end valuations: Mexico on 28x PE, Philippines, Indonesia and Thailand on 36x, 27x and 25x respectively; or those with external debt-to-GDP ratios at Cyprus -like proportions, such as Hungary (155%), Poland (71%) or Turkey (only 41% but a 7.5% current account deficit and a looming corporate debt repayment problem).

Widespread poor value means country and stock selection become ever more important and, year-to-date, the fund has navigated this problem well. Equity markets look set for another ‘surprisingly’ good year, but with those in the EMs yet again behind those of developed countries. However, capturing their superior economic growth by finding companies with higher earnings growth is not especially difficult provided investors are prepared to ignore country and index weightings, and to buy the cheapest exposure, whether listed in EM or developed countries.

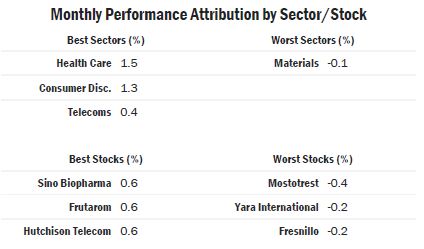

In the first two months of the year the portfolio’s 10.8% gross rise easily exceeded the 7.1% of the index; for the rolling year, the returns were 12.0% vs. 5.6%. February saw strong results from holdings in numerous different sectors. The three Chinese pharmaceutical companies acquired at the turn of the year (and the portfolio’s first foray back into China since 2009) - Lee’s, Sino Biopharma and China Pharmaceutical - all performed well as the government announced better healthcare provisions. Other strong performers were widely spread geographically: Frutarom, the Israeli-listed global flavours and essences group; in Hong Kong, both HutchTel (mobile telephony), which also produced strong results after the reporting period, and the international luggage company Samsonite; Giant Manufacturing, the high-end global bicycle maker, based in Taiwan but increasingly dependent on its Chinese factories. SHFL Entertainment, the US-based maker of electronic card readers and other equipment for the global gambling industry, also enjoyed a good recovery on a better outlook for demand, especially from emerging markets.

No sector owned suffered any meaningful fall, with the “worst” being materials (agriculture-related and gold/silver mining companies). The two major gainers were health care and consumer discretionary stocks (13% and 17% of the portfolio respectively). Both enjoy relatively low valuations and stable earnings and, as in developed markets, are enjoying a gradual re-rating.

New holdings have included Malaysia’s infrastructure group, Padini, and Mexico’s Genomma Lab, a specialist producer and distributor of over-the-counter drugs. The weighting in precious metals was increased through the purchase of Canada’s First Majestic Silver. This is a good example of a company listed in a developed market but with all its assets in EM countries; its principal mines are in Mexico, with other prospects across Latin America. Several holdings were reduced after good gains: Samsonite and Shangri-La (the hotel group) in Hong Kong, and SATS in Singapore. Others were topped up with the proceeds, such as Sembcorp Marine.

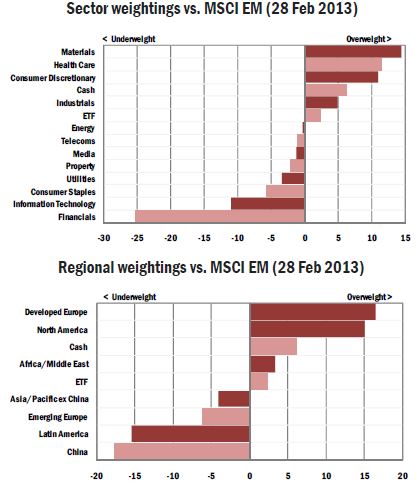

The portfolio continues to run minimal to nil exposure to financials and property, sectors which so dominate the indices. This is simply because valuations are poor and the outlook for earnings growth muted. Similarly, with the exceptions of precious metals and agricultural-related companies, there is no exposure to other commodities save gas exploration and production. Expected growth in earnings per share in 2013 is forecast in excess of 18%, yet the average multiple is 300 basis points lower than the index. The portfolio’s structure may be unconventional versus both other funds and the index, but in terms of balance sheet strength or growth at a realistic price, it is superior. The target is less to beat the uninspiring MSCI Emerging Market Index, but the World Index too.

Bedlam Asset Management plc is authorised and regulated by the Financial Services Authority (212757). Bedlam Funds plc is regulated by the Central Bank of Ireland pursuant to the European Communities (Undertakings for Collective Investment in Transferable Securities) Regulations, 2003 as amended by the European Communities (Undertakings for Collective Investment in Transferable Securities) (Amendment) Regulations, 2003 (the "UCITs Regulations") and is a recognised collective investment scheme for the purposes of section 264 of the United Kingdom Financial Services and Markets Act, 2000. Shares in Bedlam Funds plc may only be sold on the terms of, and pursuant to, its most recent prospectus. This document is not investment advice or a recommendation to purchase, hold or sell a security. Past performance is not a reliable indicator of future results.

© Bedlam Asset Management