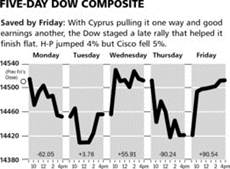

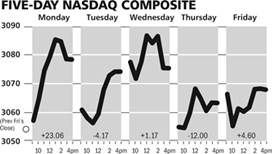

Stocks were flat last week as investors were mesmerized by the goings on in Cypress and the European Union.

When all was said and done, there was no movement in either the Dow Jones Industrial Average or the NASDAQ Composite as the charts above illustrate.

The Markets & Economy

The Federal Reserve Board met last week and the message was the same. Things are slowly getting better, but the economy has a long way to go and hence there is no change in policy now or in the foreseeable future. Of course, in this world of upside down thinking that is exactly the message that Wall Street wants to hear. This means that the zero interest-rate policy as well as the quantitative easing policy, which are financing the government’s annual trillion dollar deficits, will continue.

The implication of this, of course, is that the green light remains on for financial engineering such as the Dell buyout, or higher dividends to continue to boost stock prices and make it the winning asset class at present.

Even the news from Cyprus, which borders on the morose, could not cause more than a glimmer of pain for investors. This despite the fact that bank deposits to the tune of billions of Euro’s had been usurped and that the Cypriot economy is now entering the land of the dead. Expectations now call for that nation-state to see its economy collapse in the years ahead (sounds like Greece after their restructuring).

Given the capital controls and the inability to get your money out of the country, it is hard to see how Cyprus staying in the Euro zone could be worth it. Obviously, having a Euro in Cyprus is not the same as having one in the rest of the EMU. Thus in essence in all fundamental ways, this country is no longer a member of a single zone currency.

Don’t worry though because it won’t be long before the media’s attention turns to Slovenia, which for some reason is also broke and a member of the European Monetary Union. What a mess.

In any event the markets this morning are cheering this outcome as it pushes down the road the day when the EMU is split apart. The social consequences are awful for the people of Cyprus, but the markets are not concerned with such things.

Closer to home, the notion that our economy is on a self-contained recovery is once again gaining steam. Every spring for the past four years the data seems to give this impression only to see subsequent months roll back that notion. Clearly, the USA is doing better than most. Our energy position is improving rapidly, and housing is no longer a drag.

However, that just means we are going to see growth while most other nations (including our trading partners) are teetering on renewed recession. Accordingly, the backdrop for stocks remains paradoxically excellent as the Fed wants stock prices higher, and alternative asset classes provide little competition. While a retreat from these levels is always a decent shot, the reality is the market is poised to finish the first quarter with very strong gains. This has historically implied a very good year is in store.

What to Expect This Week

This is a holiday shortened trading week with the stock markets closed this coming Friday in observance of Good Friday. There will be a GDP report this Thursday, but I really don’t expect much volatility unless the Cyprus deal announced over the weekend somehow blows up. Given that the European markets have an even lighter schedule coming up due to Easter next Sunday, I don’t think that is likely.

This week’s ECRI Economic Cycle Research Institute Update

Our next update will be two weeks from this morning by which time we will have the employment data for March to hash over.

![]()

SYMBOL: BIIB

Biogen Idec won approval by the European Union for the use of Tecfidera, formerly known as BG-12, in Europe. We have talked extensively about this drug, and it has been the main driver for the outperformance of the stock over the past three years. This is the first major hurdle for the drug, and a decision from the FDA is expected on March 28th.

This drug is a major breakthrough in the treatment of multiple sclerosis. This is the first drug that will hit the market that allows patients an easy-to-take pill, and all of the data has shown positive effects. There are 2.1 million people worldwide that are affected by this disease. It should definitely be a blockbuster drug, and Wall Street expects sales will reach $3.25 billion annually by 2017.

Shares of Biogen have been one of the top performing stocks in the S&P 500 for the last three years, and we expect the trend will continue. The Company received several upgrades over the past week from Wall Street firms, and we believe an FDA approval later this week will help to move the stock higher. We still believe the shares will reach $200 by year-end, although that prediction might be too conservative.

![]() Three-Month Chart

Three-Month Chart

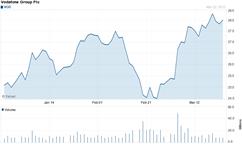

![]() VODAFONE

VODAFONE

SYMBOL: VOD

Rumors of Verizon buying Vodafone’s stake in Verizon Wireless surfaced again this morning. According to the story in the Telegraph, Verizon is more likely to buy just the Verizon Wireless assets - not the entire company. Insiders believe that Vodafone’s management would like to make a “clean break” from the business in America, and the valuation of wireless assets has never been higher. A deal could happen as soon as this summer, and shareholders of Vodafone will be the big winner. We believe a deal for the Verizon Wireless assets will lead to a $40 share price for Vodafone shareholders.

![]() Vodafone Three Month Chart

Vodafone Three Month Chart

© McIntyre, Freedman & Flynn