The Success of Central Bank Policy Is Not Measured By The Revenue It Generates

- The success of central bank policy is not measured by the revenue it generates

- Cyprus is a small country that could cast a long shadow

- The U.S. dollar's fortune is changing

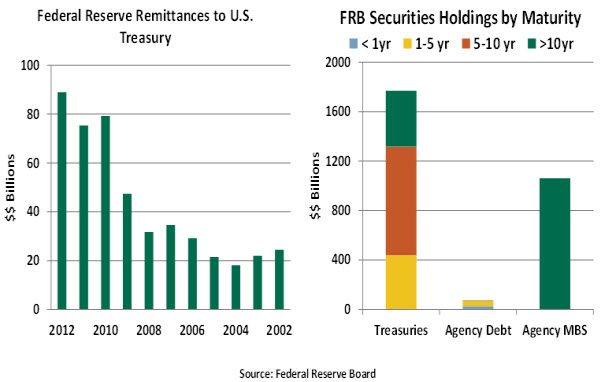

What’s the most profitable bank in the United States? The answer may surprise you: it’s the Federal Reserve Bank. The Fed’s excess of revenue over costs last year was more than $90 billion; theaggregateprofitability of U.S. banks in 2012 was only $141 billion. Of course, the Fed has the advantage of being able to create costless liabilities and growing its balance sheet without capital constraints.

It looks like the Fed’s bounty will continue to grow, at least for a while. The Federal Open Market Committee (FOMC) decided this week that its bond purchasing program would proceed unabated. The meeting included consideration of the costs and benefits of quantitative easing (QE), but the points raised apparently did not deter the group from pressing ahead. (By contrast, the Bank of England once again voted down a proposal to extend its own QE program.)

Central bank portfolios have not been constructed with the intention of making a lot of money. The goal of QE is to bring economic activity to a higher level and allow for meaningful reductions in unemployment. If and when this effort bears fruit, though, central banks will have some difficult decisions to make about what to do with all the bonds they own.

In the United States, the Fed remits its annual excess to the U.S. Treasury. Last year’s contribution didn’t make a significant dent in the fiscal deficit, but it was welcome nonetheless.

QE programs focus on long-term securities in an effort to keep long-term interest rates down. If successful, improving economic conditions will eventually lead those interest rates to rise. In this case, central banks will see the value of their holdings depreciate.

As investors are well aware, the prices of long-term securities are quite sensitive to changes in market interest rates. Rough calculations suggest that the Fed’s holdings have an average maturity of around seven years; a 1% increase in seven-year yields therefore results in roughly a 7% decline in the value of their holdings. On $2 trillion of long-term bonds, this would represent an unrealized loss of $140 billion.

Importantly, these losses would only be recognized if the Federal Reserve sold its securities. Fed officials have been very careful to note that their exit strategy would likely involve holding many of these assets to maturity, partly to sustain monetary accommodation for some time after the economy begins to improve.

But it may be difficult to balance the desire to avoid loss-taking and the need to drain reserves from the financial system at an appropriate pace. The Federal Reserve will try to manage long-term rates carefully during its exit strategy, but it holds only about 16% of the overall market of Treasury debt and Agency mortgage-backed securities. Having a precise influence over the prices of the other 84% will be a great challenge.

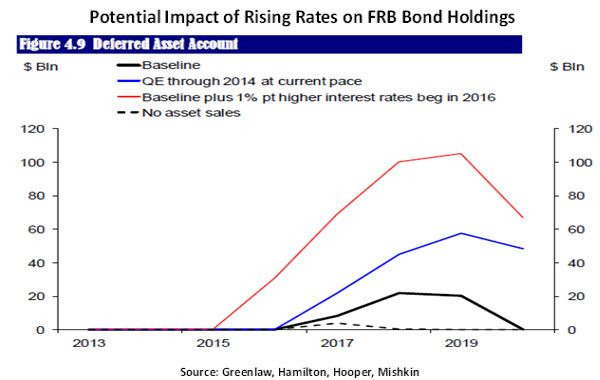

A group of economists led by former Fed Governor Frederic Mishkin recently published a paper that looked athow the Fed’s net revenue might evolve as economic conditions normalize. Using reasonable assumptions, they arrived at the conclusion that the Fed’s net revenue would fall below zero in late 2016. In this event, the Fed would create a “deferred asset” on its balance sheet which could become sizeable for a few years before receding.

To be certain, the Fed would certainly be able to continue funding its operations during this interval. (Its annual expenses amount to about $5.8 billion.) So funding from the Treasury would not be required, but the optics of the situation – no matter how well-foreshadowed – would certainly provide fuel to the critics of Fed policy.

Should this set of circumstances prevail, it will be important for everyone to remember the ultimate objective of monetary policy. If quantitative easing is successful, stronger economic growth will represent the real return on a central bank’s portfolio. And the improvement in tax revenues that would accrue to the Treasury should make the loss of Federal Reserve remittance a minor matter.

The minutes of this week’s FOMC meeting should eventually reveal details of the cost-benefit evaluation surrounding quantitative easing. For the reasons cited above, I hope that the prospective performance of the Fed’s bond portfolio was not a major consideration.

Policy Responses to Cyprus: No Confidence

The world’s attention this past week focused on the travails of Cyprus. The country has been in terrible financial trouble for some time, so the arrival of a moment of truth is not surprising. What has been surprising is the miscalculation of policy-makers as they try to stabilize the situation.

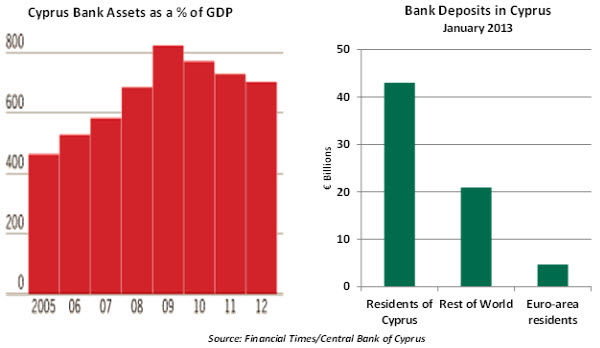

Cyprus, a eurozone member since 2008, accounts for less than 1% of eurozone gross domestic product (GDP). The root cause of its present imbroglio is the country’s banks, which suffered deep losses from holding Greek bonds. The Cypriot government came to the aid of two of the largest banks to prevent the collapse of the financial system.

The situation certainly underscores the need for a pan-eurozone bank supervisor that could have highlighted these financial weaknesses at an earlier stage, when they could have been handled in a more orderly and potentially inexpensive fashion.

The banks in Cyprus have survived on emergency funding from the European Central Bank (ECB). The ECB stated that its support will not continue past March 25 unless Cyprus strikes a deal with the “troika” (the ECB, the International Monetary Fund and the European Union) to bring its debt under some control. The current offer from the troika is contingent on the country raising about €6 billion toward its own rescue.

To generate the necessary funds, Cypriot leaders and EU officials hastily designed a tax on bank deposits that would hit large and small savers alike. This roiled not only the Cypriots, but also the many foreigners who have money on deposit with local banks.

Cyprus’ rather generous residency rules, friendly tax policies, and (some would say) lax monitoring of questionable financial activity has brought substantial funding into the country. By taxing large deposits heavily, policy-makers may have seen the opportunity to address two problems at once. But the likelihood that these monies, however shady, will depart in coming months could raise the ultimate cost of resolution.

For small savers, members of the EU have been encouraged to follow a standard outline for deposit insurance, which fully protects accounts up to €100,000. (This coverage is provided by each individual country, not the eurozone as a whole.) The initial deposit tax, endorsed by officials from Cyprus and the EU, goes against the spirit of this guidance. This is an unsettling change of direction that shakes the foundation of the banking system.

Without trust, there is no liquidity, and without liquidity banks and countries fail. If that was the outcome the troika sought to avoid, it chose an odd way to go about it. And the situation reverberates far beyond Nicosia. Depositors in other countries who are or may become dependent on aid from the troika can’t help but be unsettled by the prospect that their funds are not safe.

When confronted with a similar situation in 2008, U.S. regulators opted to go in the opposite direction. Deposits were guaranteed by the FDIC regardless of size, a step that helped settle the financial system. After the crisis passed, the insurance system was restructured to assess premiums against all bank liabilities and thereby correct any misaligned incentives.

The initial deposit tax proposal was quickly defeated in the Cyprus parliament, leaving both sides scrambling for alternatives. As of this writing, it is unclear which direction Cyprus will take. Overtures to Russia, whose citizens have significant holdings on the island, have not yet generated the needed support. (And it is unclear that the troika would feel comfortable with this arrangement in any event.) There are no other reservoirs deep enough to generate the needed funds, so Cyprus may return to the deposit tax, potentially confining it to deposits exceeding €100,000. Some have suggested converting these deposits to equity, which is called a “bail-in” by financial policy-makers.

The worst-case scenario is an expulsion of Cyprus from the eurozone. The ECB’s governing council could withdraw support before the end of March. The question would then become whether Cyprus can be ring-fenced, financially and psychologically.

Whether Cyprus falls or not, the message that other European depositors may be at risk is exactly the wrong one to send at such a delicate time. The ECB has pledged to do “whatever it takes” to stabilize financial conditions on the continent; it may soon be called upon to deliver on that grand promise.

Are Happy Days Here Again for the Dollar?

The U.S. dollar’s future trend is the subject of conversations in company board rooms, currency trading desks, policy settings. Following is our take on the outlook for the U.S. dollar.

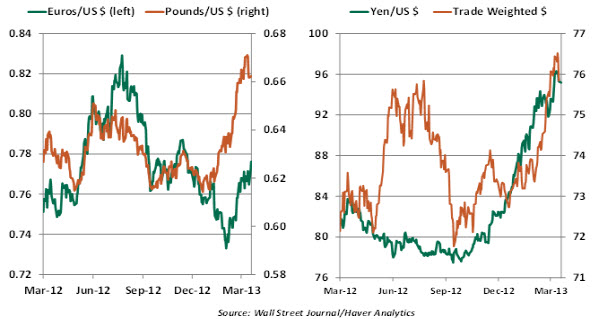

To set the stage, the charts below show the dollar’s recent movements. Year-to-date, the dollar has risen 3.4%, 5.6%, and 5.1% vis-à-vis the euro, Japanese yen and sterling, respectively. It has moved up 4.4% in terms of the trade-weighted measure. The economic and financial sector weakness in the eurozone and United Kingdom explain part of the recent improvement, while the yen’s depreciation is tied to expectations of aggressive Japanese monetary easing.

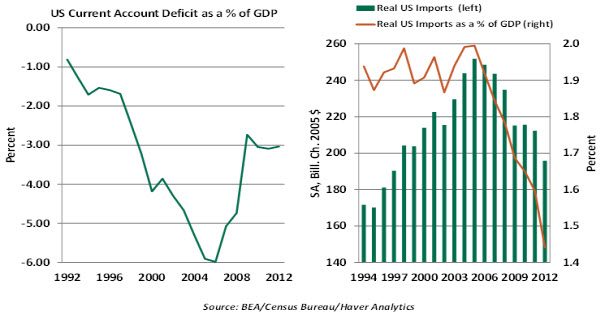

Over the medium term, the economic underpinnings of the U.S. dollar suggest a bullish outlook. The U.S. current account balance as a percent of GDP was roughly steady at around 3% during 2010 – 2012, despite an acceleration in economic activity. It is also noteworthy that real petroleum imports stand at the lowest mark in more than a decade. A better balance of trade reduces the downward pressure on the U.S. currency.

Further, the recent spate of bullish U.S. economic indicators – payrolls, housing, retail sales – bodes positively for the U.S. economy. Essentially, the relative strength of the U.S. economy is a source of confidence for investors, which should spur capital flows and demand for the dollar.

In the very near term, the Fed’s quantitative easing program will weigh on currency markets. The future trajectory of the dollar is not one straight line pointing north. It will include short-term ups and downs, but the odds favor a strong trend for the greenback given the relative economic position of the United States in a global setting.

The opinions expressed herein are those of the author and do not necessarily represent the views of The Northern Trust Company. The Northern Trust Company does not warrant the accuracy or completeness of information contained herein, such information is subject to change and is not intended to influence your investment decisions.

© Northern Trust

![]()

![]()

![]()

![]()