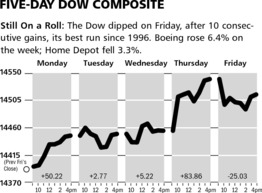

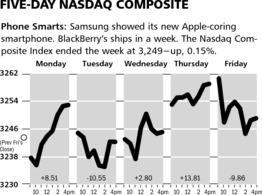

Stocks had a very quiet week with volumes reaching levels that one associates with holiday trading.

As the charts above illustrate, there was little movement in stock prices as the Dow Jones Industrial Average gained .8%,

while the NASDAQ Composite was virtually unchanged for the week.

The Markets & Economy

Last week’s slow action was followed over the weekend by a very poor idea of how to deal with the island nation of Cyprus and its outsized banking system. Cyprus, believe it or not, is a member of the European Monetary Union and thus its banking system (which lent largely to Greece and the Cypriot government) comes under the European Central Bank. The problem though is that this island over recent years has served as a magnet for some “hot” and perhaps illegal deposits from countries such as Russia, which has a $60 billion dollar exposure to the banking system of Cyprus.

This, of course, should never have been allowed to happen because the island’s banks are now broke. To make matter worse its banking system has neither shareholders nor bondholders sufficient to handle the problem. The solution then proposed by Germany and the European Union was to simply confiscate a proportion of depositors money.

This proposal has not been approved by the Cypriot minority government as of yet, and has provided evidence once again of the inevitability of the collapse of the monetary union. This scheme of confiscation runs afoul of the deposit guarantee (by the government of course) on bank balances up to 100,000 Euros. Thus this guarantee is worthless. It calls into question any such assurances there are for bank accounts in Spain, Portugal, Greece & Italy just to name a few countries with undercapitalized banks.

The European Monetary Union is an idea that should never have seen the light of day and must come to an end. It will. Recent elections in Italy where anti-EMU parties received 55% of the vote tell you the direction the wind is blowing. This latest plan for Cyprus will strengthen that trend.

Ironically, this has the side effect of making the US dollar look much more appealing, and its status as the world’s reserve currency will be unchallenged once again. As you know from my previous writings, as long as the USA retains its ability to, without limit, issue fiat currency then our day of reckoning is put off well into the future. The USA continues to be not only the best of a bad lot, but really is the only game in town for the trillions of dollars of assets seeking a home in the global marketplace.

The dollar is up on this news and our Treasury market is also higher. At the same time our economy, while growing very slowly, is showing resilience which again places us ahead of the pack. Accordingly, investment flows will continue to favor our markets.

What to Expect This Week

We have a two day Federal Reserve meeting which culminates in a press briefing on Wednesday afternoon with Chairman Bernanke. Prior to the Cyprus fiasco the chief item to flush out was the Fed’s view on our growth prospects and whether it would impact its policy of buying assets to the tune of 85 billion dollars per month.

Given the uncertainties introduced by Cyprus and the reality that our domestic growth rate of 2% or so remains vulnerable, it now seems likely that Bernanke will not attempt to further ruffle the markets. The Cyprus fiasco may be short lived, but the fear it has installed into global investors will remain for some time.

In addition, the economy will get some updates on housing and other surveys this week, but they will not cause a stir compared to the matters discussed above.

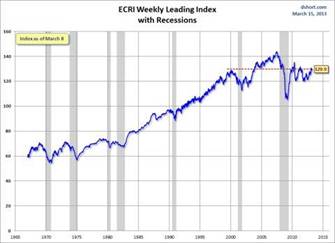

The weekly update from the Economic Cycle Research Institute showed a gain in their indicators, but overall there has been little movement one way or another for the past couple of months. While they think the USA is in recession, the evidence does not support that view. Neither does it support the view that the FED would change policy based upon the data we have seen. In other words, after the fallout from Cyprus is discounted, the markets should resume the pattern of the past several years - higher.

![]() VODAFONE

VODAFONE

SYMBOL: VOD

Shares of Vodafone continue to rally on reports that Verizon is looking to buy back its stake in Verizon Wireless. This has been rumored for years, although it seems like the companies are coming much closer to an agreement. Instead of just buying the 45% stake that Vodafone currently owns in Verizon Wireless, it is looking more likely that Verizon would purchase the entire company due to tax implications.

This is the first time that the companies have had serious discussions about a merger, and we believe Vodafone shareholders will be the big winner in any deal. We expect that shareholders will receive a significant premium to the current price, and see a deal happening by the end of this year. We see limited downside to the shares at these levels and expect any Vodafone buy out would lead to a $40 share price.

![]() Vodafone Three-Month Chart

Vodafone Three-Month Chart

SYMBOL: AKAM

The co-founder and new CEO of Akamai, Thomson Leighton, purchased another million dollars worth of stock this past week, bringing his non-option holdings to 3.8 million shares. This is his second recent purchase, and also follows the previous CEO’s purchase of more than million dollars last month. Over the past 30 days the two executives have bought $3.8 million worth of stock. We are always encouraged by insider buying, and the size of these purchases is significant. We expect the news from the Company to continue to improve over the next several quarters, and look for the share price to rise to $50 by the end of this year.

![]() Three-Month Chart

Three-Month Chart

© McIntyre, Freedman & Flynn