What America does with its money.

The quality of the Fed’s Flow of Funds data is about as comprehensive a balance sheet assessment of corporate and private America as you could wish for. It’s also great for looking at trends rather than the hot spots over which the market frets. Here are some of the findings:

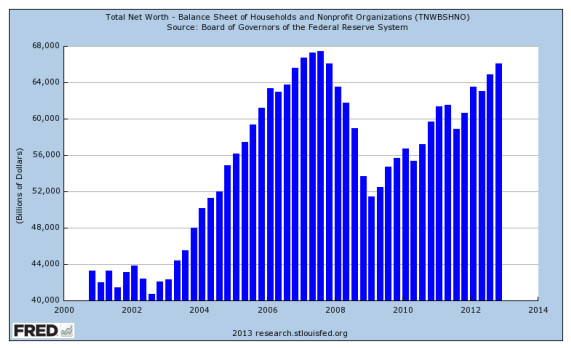

1. Household net worth: is on the mend at some $13 trillion above the lows of 2008 and up $5.4 trillion over 2012. Most of the increase is in financial assets and equities. Yes, equity in real estate rose about $1.5 trillion or 22% in the last two years but well over a third of the gain is from a run down in mortgage debt rather than an increase in house prices. Here's the overall net worth picture:

Source: Federal Reserve Bank of St. Louis, Economic Research

It’s a solid report and stands behind the gradual increase in confidence we have seen in other measures. But net worth increases from securities and savings do not have the consumer spending multiplier of real estate value increases. For one, the rise in prices from securities is not attachable in the way that aHELOCcan work. It helps, but the days (1997-2007) whenPCEgrew at 1.5x the GDP rate and contributed some 80% of growth are well behind us. So, for now put this down to ongoing balance sheet repair.

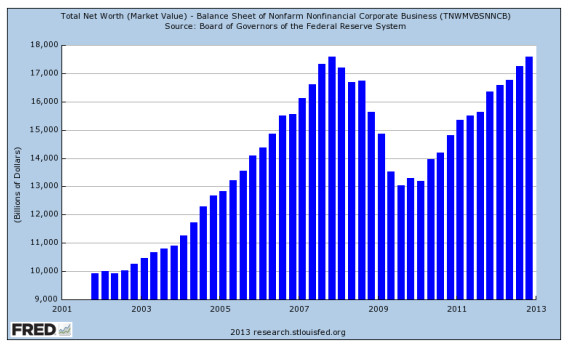

2. Same story with the corporate sector: Companies have built up their capital expenditures and financial assets and reduced their liabilities.

Source: Federal Reserve Bank of St. Louis, Economic Research

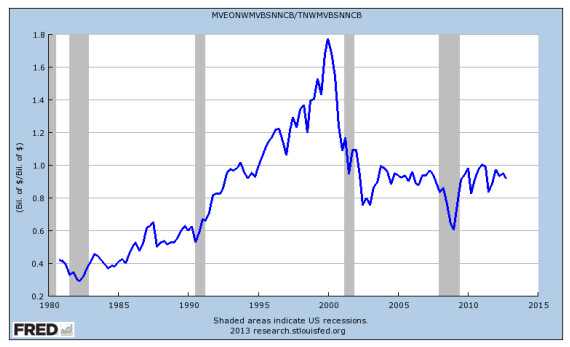

The Fed’s report showed that the market value of equities of $16.2 trillion was equal to 0.92 times the net worth of companies at $17.5 trillion. This is just another way to express Tobin’s Q, which measure a firm’s market value to replacement cost of assets. In the long run, they should roughly equal each other for a ratio of 1.0. The long term average since 1900 is 0.65 but in the last 15 years has ranged from 0.6 to 1.8. Here it is now:

Source: Federal Reserve Bank of St. Louis, Economic Research

The market value number can bounce around a lot but at this stage, we’d simply say that valuations appear reasonable and that companies continue to draw in borrowings and net indebtedness and are thus a source of net savings.

3. Stock market as a negative source of funds: which picks up a secular theme that was only briefly interrupted by the recession. In 2012, companies had net issuance of (-$207bn) about the same as 2011 and compared to the $580bn of issuance in 2008 and 2009…all of which came from the financial sector. Since 2006, net issuance has shrunk in five out of the seven years for a total of (-$680bn). It’s nothing to be too worried about except that lower shares outstanding improve the EPS line without any non-leveraged improvement to the bottom line. The longer term question is, what is the point of a stock market except as a source of permanent funds? Those funds have been shrinking, albeit while market values increased, and would probably have been better used as dividends.

4. And the headline drop from a year or so ago: when commentators were all a-twitter that 60% of Treasury issuance was being bought by “monetary authorities,” i.e. the Fed, and that would surely, no, must lead to a rate increase once price support diminished. That number is now less than 5% and demand from the household sector for US debt has soared to $600bn in a year. And the foreign buyers that we couldn’t possibly live without? Turns out we can. They bought 46% (net) Treasury debt two years ago against 30% now.

US: no push but some pull through

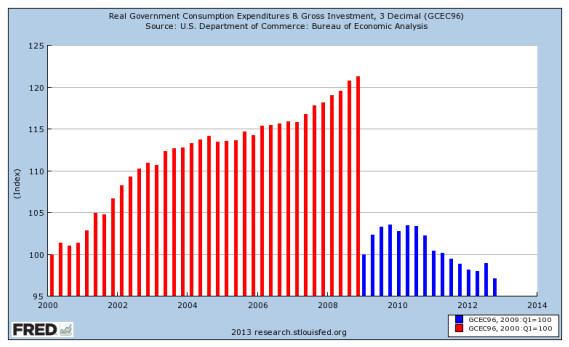

The four fiscal threats are winding their way through the system. These were i) increase in taxes for January 1st, ii) sequester, iii) continuing resolution, and iv) debt ceiling. We’re still awaiting the effect of the first two on the economy. So far things have been muted but they may not remain so. Starting with the fiscal drag, this is what growth in government spending looks like in the post recession period compared to the first eight years of the decade.

Source: Federal Reserve Bank of St. Louis, Economic Research

That blue line is the slower rate of all government expenditures which has happened pretty much relentlessly since 2010. The red line is the 20% increase in government spending in the…well you know. This month’s budget statement can be broken into the following (the numbers are for five months into the fiscal year starting October):

| Item (bn) | 2012 | 2013 | Change |

|---|---|---|---|

| Deficit | $581 | $494 | (-15%) |

| Receipts | $893 | $1,010 | +13% |

| Outlays | ($1,474) | ($1,504) | +2% |

| Borrowing | $601 | $555 | (-8%) |

| Income Tax Receipts | $425 | $500 | +17% |

| Big 51 | $1,118 | $1,146 | +2.5% |

| Rest of Budget | $357 | $356 | 0% |

| Receipts on Social Security | $322 | $344 | +7% |

| Outlays on Social Security | $330 | $353 | +7% |

| “Shortfall” | ($8) | ($9) | 0% |

| Net Interest | ($101) | ($100) | 0% |

| Interest/GDP | 1.6% | 1.5% | - |

| Deficit/GDP | 9.1% | 7.5% | - |

Source: US Department of the Treasury, Monthly Treasury Statement, February 2013

1.Big 5 budget items are Defense, Social Security, Medicare, Medicaid and Interest. Together they make up 76% of the Federal budget

Now, the fiscal year is not over and there are seasonalities which make the straight line extrapolation a little simplistic. But the core story is that fiscal consolidation is going on and at quite a pace. The deficit is falling rapidly. It’s certainly helped by double-digit growth in revenues which supports the truism that the cleanest and quickest way to improve the deficit is to get people back to work. The so-called entitlement programs are growing but so too are the hypothecated taxes, especially the social retirement tax. At the rate of the current shortfall, and assuming modest growth in the $2.6tr Social Security trust fund, Social Security will drop scheduled benefits down to payable benefits in about 22 years. We do not currently see a scenario where Social Security stops paying!

The deficit meanwhile continues to shrink. The latestCBOestimate is for a deficit of 5.3% for this year and leveling out at around 3% for the next 10 years. Whatever problem we’re trying to solve, discretionary non-entitlement programs isn’t one of them. And the entitlement programs really revolve around an aging population and medical costs. But they’re certainly not big enough to crowd out the private sector.

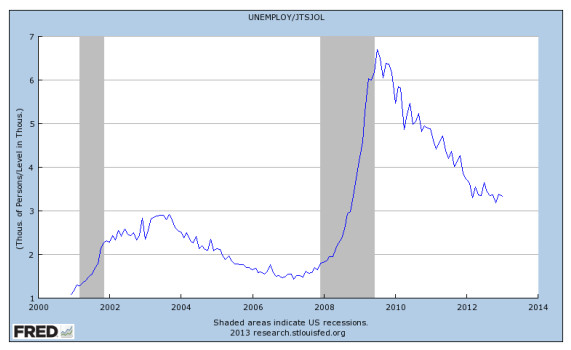

On the jobs side, we saw theJOLTSreport which should be a lot stronger given the employment gains. There does not seem to be enough in the way of job openings. The latest number show around 3.6m up from lows of 2.4m but the relevant number is openings per person unemployed and it looks like this:

Source: Federal Reserve Bank of St. Louis, Economic Research

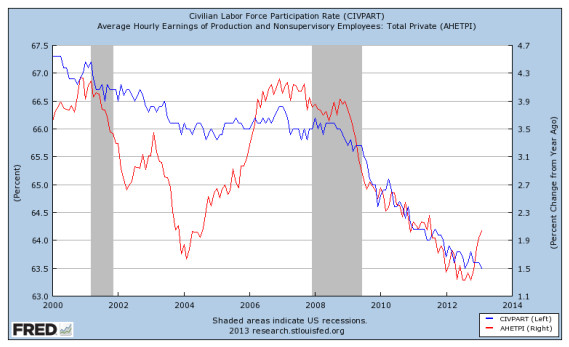

So that’s way above what we would expect. Here the normal cue is “aha…see it’s structural unemployment” and there're some points to that argument. TheNFIBcame out last week and, again, 34% of companies reported few or no qualified applicants for job openings. Similarly, the participation rate is coming down steadily (here the blue line) while earnings (red line) hooked up in the last report.

Source: Federal Reserve Bank of St. Louis, Economic Research

But against this, we should acknowledge that the small companies in the NFIB survey always report difficulties in hiring and even at the worst unemployment rate levels in 2009, well over a quarter reported difficulty in finding applicants. On the earnings side, we would rather see a few months of higher earnings increases before claiming a tightening labor supply. The latest number may be no more than employers willing to provide overtime and more pay rather than hire. So it’s way too soon to think of the labor market as constrained or in some way structurally changed from prior years.

Bonds

We had 3/10/30 auctions last week. The 3-years are rarely eventful. The 10-year had been traded weakly in the first half of the week, disturbed, probably, by the strongishNFPs. Going into the auction the 10-year was trading weakly in therepomarket which tells us that there was a big short ahead of the auction. But the auction was successful and the 10-year yield ended up some 5bp lower by week’s end. The 30-year auction was a little weaker with a lower bid/cover ratio and the indirect bidders taking 42% compared to a norm of 34%. By the end of the week there was very little net move in bonds.

Overall, the tone seems to be firming. We have digested the supply. Mortgages remain under pressure…we think it’s mainly hedge fund selling. High yield continues to outperformIGs YTD by about 180bp. Put that down to equity strength.

Equities

All roads lead to a 1600 level. The consolidation around the 1560 level is very welcome. The market has two forces at work: those who want a pull back and those who don’t want to fight the tape. One adage works for us right now: don’t short a bull market. Consensus estimates are for a $110 EPS coming into earnings season. The valuation strikes us as very reasonable.

Bottom Line: On any small set back we will up our equity exposure.

Bottom, bottom line: Two members of Sentinel’s extended family passed away last week. Our deepest sympathies go to the families.

Sources: Bloomberg, Capital Economics, CRT Ader, Economist Free Exchange, Federal Reserve Bank of St. Louis, IMF Fiscal Monitor, Federal Reserve Bank of Kansas, Federal Reserve Bank of New York, Federal Reserve Bank of Philadelphia, Federal Reserve Board, Bureau of Labor Statistics, Bureau of Economic Analysis, Congressional Budget Office, US Dept of the Treasury, ISI, J.P. Morgan Market Intelligence, High Frequency Economics, Pantheon MacroEconomic Advisors, TrendMacro, Tim Duy’s Fed Watch, Bank of America, Merrill Lynch, National Federation of Independent Business, Sentinel Asset Management, Inc.

© Sentinel Investments