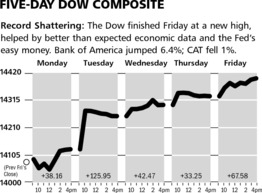

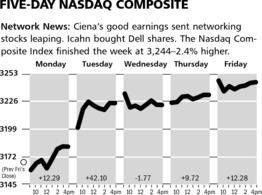

Stocks rose each day last week as the notion of a ho-hum global economy was reassuring to those who fear either a recession or a surge in economic activity.

As the charts above illustrate, the Dow Jones Industrial Average and NASDAQ Composite moved higher by better than two percent for the week ending March 8th.

The Markets & Economy

Well, the overblown fears of sequestration (remember that?) have now been put aside, and the idea of a lumbering onward global economy has resumed as the most likely outlook amongst investors. Last Friday’s employment report for February showed a larger increase in non-farm payrolls and a drop in the official unemployment rate to 7.7%.

Of course, with this report in particular, the details are not nearly as convincing. First, January was revised downwards fairly sharply. Secondly, the statistics noted above exclude 89.3 MILLION Americans who are alive and well but are simply not counted as being “officially” in the work force despite the fact that they are.

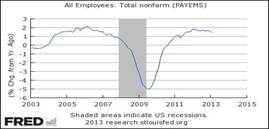

In fact the two graphs furnished below show exactly what I am talking about. The first shows the number of non-farm payroll jobs today versus the past. We have no greater number today than nearly ten years ago, despite population growth and immigration adding to the potential workforce.

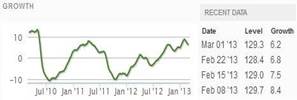

The second graph proves the same point from a different direction. It shows the “participation” rate for the US population. That is the percentage of the overall population who are considered by the government to be in the workforce and thus eligible to be counted as either employed or not employed.

As we have noted many times this percentage is falling like a stone and represents very bad news for society and our government’s finances (people who don’t work don’t pay taxes and consume government transfer payments etc…)

Today’s news that some 47 million Americans are receiving food stamps and some 8 million Americans are on disability is a reflection of this dismal state of affairs.

Thus it is with great amusement that I listen to commentary about how wonderful the last report on jobs was - especially when one considers that it was taking place with the background of zero percent interest rates and governments globally printing money by the trillions in order to keep the global economy from falling below the zero growth line.

The good news for stock market investors is that the Central Banks of the world understand this, even if politicians do not and a citizenry which does not care. Thus you have seen promises from the Federal Reserve, Bank of England, European Central Bank and most aggressively the Bank of Japan which all indicate the printing presses remain wide open and they, as a group, want stock prices (and other asset classes) to rise. In their judgment this is the best way to spark a recovery.

The USA has the added advantage of the boom going on in the energy industry due to new technologies and discoveries. This is very bullish for us and our portfolios are well represented in this decade’s long build out of our energy infrastructure.

What to Expect This Week

It will be a very quiet start to the week. Earnings reports season is over and the only news comes late in the week concerning inflation. This is not exactly a data point which will change market psychology.

The weekly update from the Economic Cycle Research Institute is below. It bounced back after several down weeks, but the people there are sticking by their guns that the US has entered into a recession - we just don’t know it yet. That sounds old by now, but my view remains the same, the global economy is mired in very slow growth. While monetary policy attempts to do what it can to offset the growing austerity on the fiscal side; because government sectors, both here and certainly in Europe, can no longer be afforded in a traditional sense.

.

SYMBOL: BA

SYMBOL: BA

Shares of Boeing have been rallying as orders for the 787 Dreamliners continue to gain momentum. Even though the plane has been grounded since January, more airlines around the world continue to place orders for the aircraft. Just last week Air Berlin ordered another 15 aircrafts, and the battery issues seem to be getting resolved at the Company.

This morning a vice-president stated that the Company is confident that they have a permanent solution to the battery issues that grounded the plane. We do believe this will be a short-term hiccup for the Company, and as they get the 787 Dreamliners back in the air, investors will take notice. Shares of Boeing have been trading higher as the Company is making progress with these issues. The valuation is still very conservative for Boeing, and we expect the price will reach $100 once they get the 787Dreamliners back in the air.

![]() Three-Month Chart

Three-Month Chart

SYMBOL: VOD

SYMBOL: VOD

Shares of Vodafone rallied last week after Verizon stated that they would like to buy Vodafone’s stake in Verizon Wireless. Verizon has been looking to buy back the 45 percent stake that Vodafone currently owns in Verizon Wireless, and we think management on both sides are moving in the right direction. There were some discussions in December about a full merger, and we believe these conversations will lead to a deal in the near future.

We recently upped our stake in Vodafone and expect any deal will lead to much higher prices for shareholders. We expect that a deal will be done by the end of this year, and Verizon will be paying a significant premium for Vodafone’s stake in Verizon Wireless. We believe the shares of Vodafone will reach $35 by the end of this year.

Three-Month Chart

Three-Month Chart

© McIntyre, Freedman & Flynn