Imagine you are in a boat about the size of a car. The waves coming at you are equivalent to a twelve story building. Your boat is leaking badly and you're about to head into the Roaring Forties, some of the most ill-tempered seas in the world. What do you do? Well, Donald Crowhurst faced this in 1968 in an attempt to be the first to sail solo round the world. The stark choices were to continue, and meet almost certain disaster, or turn around and face bankruptcy. Then a third option came to him. Stay still, wait for other racers to pass him by, slip into their wake and return home the short way. Survive with a simple deception. No harm done. It turned out very badly and if you want to know the ending, watch a tremendous documentary called Deep Water. But for today, the “staying where you are and waiting it out option” is what is happening in Europe. What looks like a fairly settled policy is fast becoming a very dangerous situation. The outlook for the world’s second largest economic block is pretty awful.

On we stumble

TheECBis a curious animal. Its only mandate is price stability and to do it with very few tools. QE? Nope. Asset purchase? Not really. Buyers of sovereign debt in the primary market? Definitely not. Foreign exchange intervention? No. Reserve management? No.

This week the bank kept interest rates unchanged even as unemployment hit the 19m mark. Mario Draghi warned that in a bank-based economy, i.e. where capital markets play little part in the financing of enterprises and nearly all expansion and growth must be financed with loans, the transmission mechanism was still very weak. In simple terms, this means that credit does not flow and that banks’ poor asset quality and risk aversion prevents liquidity flowing to where it’s needed most. So we have a situation where i) inflation is at or below the forecast rate ii) the flow of money is seized and iii) theOMTsare a solution that, as yet, no one wants to engage . So what we face is very limited ECB support to the wider economy in Europe.

Some commentators suggest the ECB has failed. In fact, it has done a lot given the very limited arsenal at its disposal. Draghi managed to talk away the risk of a break up last summer and the all important spread differential of Italian and Spanish debt to Bunds has held up. But we’re now entering a phase where the low rates simply forecast low growth, low demand and inertia. Not any broad confidence in growth. The ECB is not to blame. It has all the tools of a Swiss penknife in a world which needs backhoes. Meanwhile the real economy stats look pretty sad: 4Q GDP in the eurozone fell 0.6%, and nearly every component fell in unison. Exports were down 0.9% and consumption fell again. It has not registered positive growth since mid 2011. The French economy is feeling the pinch. Government is pulling back, the relatively strong euro hurts French exports, and its decade long history of increasing labor costs at twice the rate of Germany means that large parts of the economy are very uncompetitive. The overall risk, of course, is that if France begins to hurt, the core cohesion of the EU will come under increasing duress.

There are few hints that the road of “growth through austerity” will change in Europe. But there are more voices calling out. Last week the boss of Fiat said “I understand austerity, but we can lose weight until we die.” Or, another way, just staying put and trying to sit it out is highly dangerous. By any normal standard, Europe should be pursuing easier monetary conditions immediately and governments should be on a course of gradual fiscal growth. The fact that it is not happening means more woe.

The Fed by contrast…

Two more speeches last week from the Fed heavyweights (so that’s Bernanke and Yellen) which reinforced that any tussle between Camp One of “ease up soon, we don’t know what effects Fed policy is doing to financial markets” and Camp Two of “we know exactly what we want monetary policy to do and we won't ease up until we get there” is one sided. Camp Two is winning. Bernanke was up first where he answered the question of why rates are low. The answer was flatly that inflation is low and is expected to remain so, the recovery weak and that term premiums, or the extra return expected from holding long-term bonds, were low because of the safe haven demand for safe assets. He does not think that any assets are mispriced to any real level and that, anyway, the Fed has better oversight, supervision and understanding of the financial sector than they did. This is probably very true as last week’s stress tests on 18 of the large bank holding companies showed that under even severe conditions, Tier 1 capital would fall from around 11% to 8% or about what they were four years ago. In other words, there should not be any major financial fall out from the banks. Famous last words perhaps, but it does mean that there's unlikely to be any monetary easing caused by worries from asset prices.

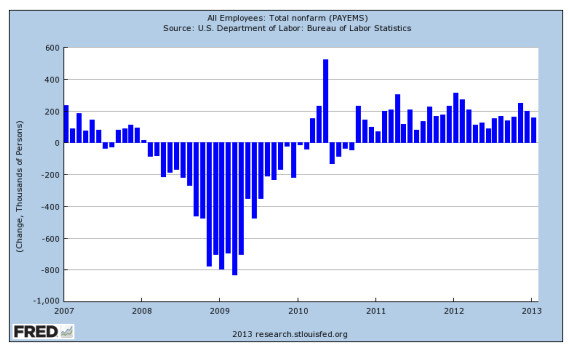

Over at Janet Yellen’s speech we got some strong indications of what would change Fed policy. For a start, there's unlikely to be any change until we see a substantial improvement in unemployment. That means not just the 6.5% level, but things like hirings and total employment. Are we any where near? Well no, not even with the strong 236,000 increase in new jobs last week and a nice reduction in the unemployment rate to 7.7%. Here's the trend in new jobs. We’ve seen strong +230,000 numbers before in this recovery and they haven’t held.

Source: Federal Reserve Bank of St. Louis, Economic Research

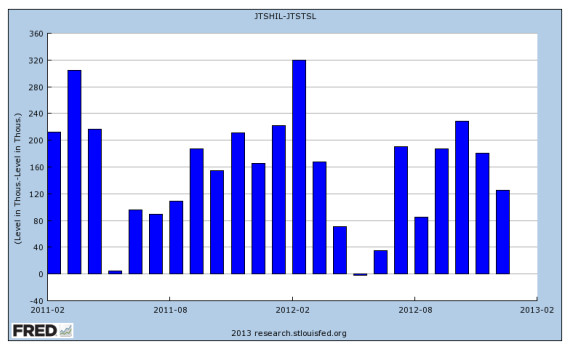

Here's the hires-less-separations, which hit lows of -800,000 in 2008 and 2009 and should be closer to 350,000 in a robust labor market.

Source: Federal Reserve Bank of St. Louis, Economic Research

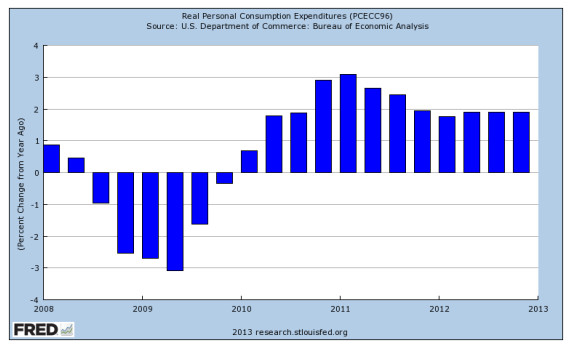

And here's all personal consumption expenditures which are not in any danger of hitting the Fed’s 2% target yet alone the newly revised one of 2.5%.

Source: Federal Reserve Bank of St. Louis, Economic Research

The recent personal income report held little to suggest any upward momentum to employment and growth. Disposable income fell 4%, interest payments as a total of compensation fell again (all part of household delivering) andDPIper capita, one of our favorite indicators of how much is being earned, fell YOY to $32,483. It hasn’t changed since 2006.

A final point in the speech was what the Fed may do with the $3.1tr in assets on the balance sheet, of which 88% are treasuries andMBSand 74% are securities of over five years’ maturity. We’ve thought for a while that the answer may be “nothing” and that the book may just roll off. In this case, the Fed can always use the overhang as a powerful tool to curb inflation because it could push the securities out quickly to raise rates if needed. This idea is getting more currency and could remove the risk of market destabilization. It would be a neat trick if we could get all the benefits of lower rates from asset purchases without concerns of a major put back. It would not be the first time this Fed has used untried policy to help the demand economy every way it can.

Bonds

Last week the market sold off around a point as it first saw betterISMnumbers. The non-manufacturing index hitting a twelve-month high and both indices showed good gains in orders and employment. The strong employment gains on Friday were enough for 10-year treasuries to stay above 2%. But there was noise in the numbers to suggest (as above) that QE will remain. The labor force contracted by 130,000, participation dipped (it’s now half a point lower than a year ago) and even at the 200,000 of new jobs, we don’t hit the Evans-rule of 6.5% for well over a year. We continue to look at parts of the credit market where the “story”, or management, products and margins, are drivers of return, not just rates, duration and spreads. This is leading us into non-index names, which feels like a very good strategy in light of how hard some index constituent bonds might be hit in any ETF sell-off.

Equities

We made it. Records on the leading indexes. Although not in real terms and with some very painful corrections along the way. We don’t buy the “rotation” story and anyway “weight of money” arguments for stock gains are well worn and vacuous. Fund flows are simply less important these days. Hedge funds, institutional, corporate and retail demand have been growing, largely at the expense of funds. One good sign of confidence has been more announcements of share buy-backs. These aren’t always good for a few reasons. One, companies tend to buy less than they announce, two they nearly always buy near the top and three they can waste a lot of money doing it (one reason why they should run the purchases through the P&L account but that’s a diatribe for another day). But we have had a near 20 year record month for buy-backs in February and the market likes that. So do we.

Bottom Line : We remain overweight equities and have been for a while. On any pull-back we would add more. We are keeping a strong watch on valuations. Anything more than a forward multiple of 15 on the market would concern us.

Sources: Bloomberg, Capital Economics, CRT Ader, Economist Free Exchange, Federal Reserve Bank of St. Louis, IMF Fiscal Monitor, Federal Reserve Bank of Kansas, Federal Reserve Bank of New York, Federal Reserve Bank of Philadelphia, Federal Reserve Board, Bureau of Labor Statistics, Bureau of Economic Analysis, US Department of Commerce, US Census Bureau, US Dept of Housing & Urban Development, ISI, J.P. Morgan Market Intelligence, High Frequency Economics, Pantheon MacroEconomic Advisors, ISM Chicago, Sentinel Asset Management, Inc.

© Sentinel Investments