Executive Summary

- While large-cap indices get all the headlines, mid and small caps have continued to excel.

- Frontier markets have picked up the slack as major emerging markets stumble.

- Global risks persist, though U.S. fundamentals appear solid.

- The move toward U.S. energy independence should soon result in a trade surplus, boosting GDP.

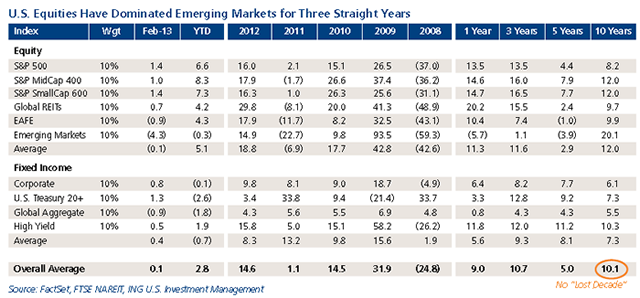

The U.S. equity market is on a roll, still cheering investors after a multiyear bull market. While the media loudly anticipates the records about to fall in prominent benchmarks like the DJIA and the S&P 500, less-heralded indexes like the S&P MidCap 400 and S&P SmallCap 600 breached their post-2008 highs two years ago. But we have to give the patriarchs their due; they have picked up the pace of late despite the seemingly heavy burdens of the fiscal cliff and the sequester riding on their backs.

But what happened to the thoroughbred emerging markets? Emerging markets were supposed to be the unblemished, low-debt engines of global growth. Meanwhile, after a robust start to 2013 the U.S. is building on its trifecta — three straight years of equity market dominance over the emerging markets. The much-vaunted BRIC (Brazil, Russia, India and China) countries are behaving like their namesake, posting negative returns over the past 52 weeks.

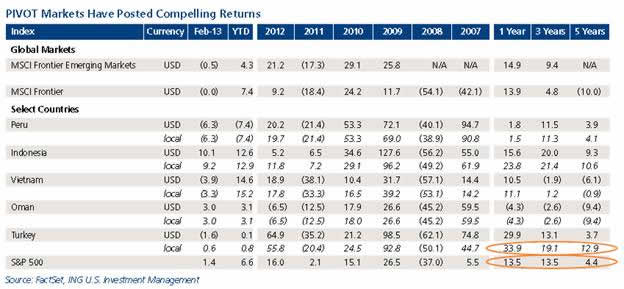

It may be a day of reckoning for these countries: Either modernize your economy and open it up to the free market, or risk being left behind. It’s not that investors do not appreciate emerging markets, but they will only wait so long for the emergence cycle to finish. For example, how much longer can China afford to deny its citizens the freedom to compete fairly against the government in the marketplace? Investors are global in focus — and limited in patience — and have shown signs of a “PIVOT” toward the frontier markets.

PIVOT is a Global Perspectives acronym representing Peru, Indonesia, Vietnam, Oman and Turkey — a broad and diverse group of newly emerging countries that have unique risk and return characteristics. Investors who are focused primarily on slow-growth developed countries need to adjust their orientations toward the markets that will be driving the expansion of the world’s economic pie.

- Peru may be having a down year in its equity markets, but the country’s 6.1% GDP growth rate in 2012 and its position as the world’s third-largest copper producer will continue to highlight investment prospects in Latin America.

- Indonesia is one of the only countries to experience a sovereign debt upgrade in 2012. The fourth-most populous nation in the world suffered a slight slowdown in economic activity last year, as its exports of coal and oil to China and India slowed. However, GDP growth still clocked in at a solid 6.2%, and expectations are for 6%-plus growth again in in 2013.

- Vietnam has experienced some high-growth growing pains of late. But with Chinese manufacturers taking notice of Vietnam’s young, tech-savvy population and its comparatively low labor costs, the country will continue to offer opportunity galore.

- Oman, contrary to public perception, is not simply an oil play. Its non-oil-related GDP is growing by double digits, and its debt-to-GDP ratio is the lowest on record. Meanwhile, Oman signed a free-trade agreement with the U.S. in 2009 that will expand its future growth potential

- Turkey is a model of European economic growth, standing in sharp contrast to the likes of Greece and Portugal. Strong growth rates in recent years have made Turkey the largest economy in Eastern Europe and helped its equity market outperform all other emerging markets in 2012, with a 56% total return in local terms. Moreover, these trends suggest Turkey is a market with legs.

Global Risks

Global risks abound. Europe is in its third year of recession out of the last five, and Italy is a deer in the headlights following the inconclusive result to its latest elections. China has had to extend the loan terms to its cities due to massive overinvestment; meanwhile, policymakers appear to have grown panicky about the country’s property bubble, recently slapping a poorly considered 20% tax on housing capital gains. Nevertheless, it still makes sense for investors to explore beyond U.S. borders, even beyond emerging markets; a PIVOT to the frontier may be the right way to go.

Market Fundamentals

Regardless of location, geography or stage of economic development, we recommend an in-depth exploration of any market’s underlying fundamentals prior to investment. Accordingly, we turn our attention to the ABCDs of market fundamentals.

Advancing earnings growth. Corporate earnings growth — the primary fundamental of the market — has surprised on the upside. With 98% of the S&P 500 having reported fourth quarter 2012 results, year-over- year earnings growth is a solid 3.9%, as companies — especially in the financial sector — have managed to push earnings ever higher despite the economic headwinds. Should it hold, as it almost certainly will, the fourth quarter’s expansion would represent a turnaround from the third quarter’s negative print. Earnings tend to trend; though it is unusual to reverse course like this, it is not without precedent. We will closely monitor the earnings front.

Broadening manufacturing. Manufacturing has once again stood strong and is clearly in expansionary range with the latest ISM reading of 54.2%. The U.S. energy boom continues to fuel a subtle but growing trend

of manufacturing “on-shoring” to the U.S.

Consumer as the game changer. Overwhelmingly positive housing data — including a healthy 7% year-over-year increase in housing prices as reported by Case-Shiller — is buoying consumer sentiment and contributing to the so called wealth effect that Americans feel from rising property and stock values. Housing, however, is considered a greater contributor to the wealth effect, as it is less volatile.

Developing markets. Growth is undeniably stronger in Latin America, Africa and Southeast Asia, where economies are not weighed down by older populations and high debt burdens. With economic growth in the developed world likely to remain constrained by these factors, investors are advised to look far and wide for diversification and growth opportunities.

Tectonic Shifts

Global trade is looking like a vastly underestimated catalyst for future economic growth, based on international trends as well as those in the U.S., which might be on track to post its first trade surplus since 1975. We forecast that within the next two to three years, trade will be additive to GDP.

A little primer on how gross domestic product (GDP) is calculated is probably in order.

GDP = C + I + G + (X – M), where

C = consumption

I = investment

G = government

X = exports

M = imports

The exports minus imports part of the equation represents the trade deficit or surplus, and there are several developments currently in place that are supporting the latter. The U.S. path toward energy independence, for example, provides a double benefit toward a trade surplus. Not only do we have ample oil and gas to export, production trends suggest our need to import energy will be all but eliminated in the near future.

Broad Global Diversification

The more you hear about a particular risk, the less likely its market impact will be of significant magnitude. Notwithstanding the obvious shortcomings of the sequester, we believe it is market positive, as it means that the private economy gets a reprieve from the obligation to supply $85 billion of capital to an inefficient government sector. Meanwhile, broad trends around the world that we call tectonic shifts — including global trade, energy, frontier markets and technology — are conspiring to provide upside surprises to the private economy and corporate earnings growth in particular.

If you find yourself looking for assets that you wished you owned, it might be time to heed our advice to be broadly globally diversified at all times. While you are at it, consider a PIVOT to the frontier markets as well.

This commentary has been prepared by ING U.S. Investment Management for informational purposes. Nothing contained herein should be construed as (i) an offer to sell or solicitation of an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. Any opinions expressed herein reflect our judgment and are subject to change. Certain of the statements contained herein are statements of future expectations and other forward-looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) increasing levels of loan defaults (5) changes in laws and regulations and (6) changes in the policies of governments and/or regulatory authorities.

The opinions, views and information expressed in this commentary regarding holdings are subject to change without notice. The information provided regarding holdings is not a recommendation to buy or sell any security. Fund holdings are fluid and are subject to daily change based on market conditions and other factors.

Past performance is no guarantee of future results.

© 2013 ING Investments Distributor, LLC • 230 Park Avenue, New York, NY 10169

CID 5921