- Labor policy needs to help, not hinder employment

- The U.S. employment report surprised on the upside

- Watch the shadows behind China’s official credit measures

Among the few universally held views in economics is that good jobs with good incomes are a good thing. Employment drives wages, which drive spending, which drives profits, which in turn drives more employment. This virtuous cycle drives economies upward at a nice pace.

Those working are able to maintain their skills with on-the-job experience and training. Those working are paying taxes and paying into social benefit programs, instead of drawing upon them. And those working are in a better position to save and invest, activities which support economic growth.

Yet while governments worldwide agree that improving employment conditions is desirable, there is much less consensus on how to achieve the task. Labor policies that are intended to help workers’ fortunes often have counterproductive side effects. At a time when many countries are seeking better labor market outcomes, it seems essential to understand the impact that government strategy has on hiring.

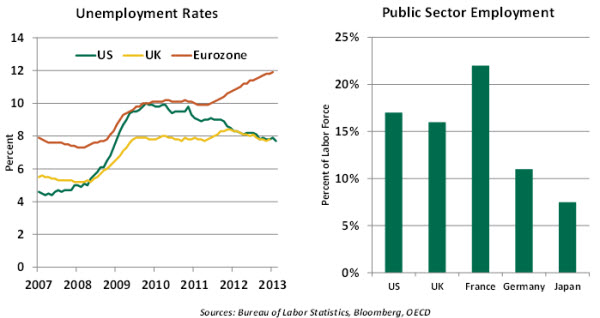

Unemployment across major world markets is uniformly higher than it was six years ago. Recession leads employers to reduce staff in an effort to preserve profitability. This is often a difficult and expensive process, and employers are consequently very careful about reversing it. In good times, employees are human resources; in bad times, they are costs.

Direct government hiring is the most basic example of policy to promote employment. In the aftermath of the Great Recession, however, world governments followed the example of the private sector. Efforts to reduce debt accumulation have led to job reductions across a variety of national agencies. This has proven to be a special hardship for countries with high levels of public sector employment, and leaves displaced workers to seek new opportunities in the private sector.

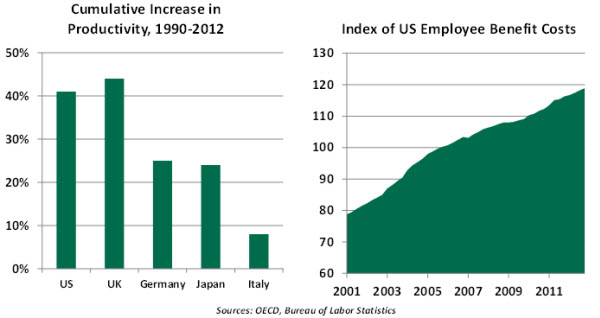

Employees are most attractive when their productivity is high, which is to say that the ratio of output to wages is greatest. Productivity can be bolstered either by improving the skills of employees or by improving the tools or technology they have to work with.

Governments have often invested in re-training employees and in business infrastructure. Many have suggested that investment in re-invention should be highest during periods where economic transition has been most substantial.

Unfortunately, the right policy action can be trumped by other agendas. The international rush to austerity has limited funding for maintenance of physical and human capital. Policy makers must remember that some line items in a national budget are investments, and not costs.

Further, firms facing changing times prefer flexibility in managing their staffs so that they are always appropriately sized and allocated. In all countries, though, there exist certain labor market “rigidities” that can serve as headwinds for personnel managers. These include guidelines on the length of a workweek, seniority preferences, severance requirements, and outright employment protection rules.

Designed to shield workers from the sometimes harsh realities of the labor markets, these measures can nonetheless inhibit the demand for labor. They can serve to diminish productivity, and prevent firms and countries from adapting to changing circumstances. Countries with more significant rigidities generally have lower productivity growth.

In the United States, the most important labor rigidities are minimum wages and health care costs. Classical economics suggests that job creation should be better in systems where wages are allowed to seek their own level. Yet many countries have minimum wage laws, using them to ensure income levels that are sufficient for working families.

The amount of “drag” on employment created by minimum wages depends critically on where they are set and how fast they grow. In the United States, the minimum wage has increased from $2.90 to $7.25 per hour over the past 40 years. That represents an annual increase of about 2.3%, only about half the yearly increase in the Consumer Price Index over that interval. Under these circumstances, the weight of studies suggests that minimum wages do not significantly impair hiring.

Unlike their foreign competitors, American employers also bear the responsibility of providing health care costs for their employees. With those costs rising rapidly, this duty has become a strain on both bottom lines and management attention. And it diminishes the attraction of adding to staff.

The challenges of reforming the U.S. health care system are too numerous and complicated to cover in this space. Progress on this front, however, could clear the field a bit for employers contemplating expansions to headcount.

Labor policy has always been challenged to balance efficiency and fairness. Yet as we strive for better employment, self-made structural impediments deserve extra scrutiny. Sometimes, moderating the burden faced by employers can ultimately work to the benefit of employees.

February Employment Report – Don’t Get Overly Excited

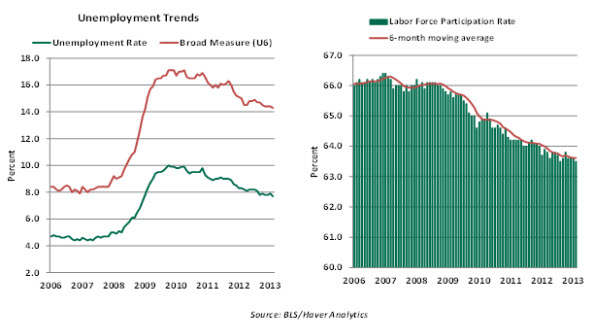

The February U.S. labor market headline numbers – a 7.7% jobless rate and 236,000 new jobs—are unquestionably upbeat. But there are reasons not to get carried away by optimism.

The decline in the unemployment rate to 7.7% in February, a new cycle low, from 7.9% in January has resulted in a 0.6% drop of the jobless rate during the last six months. However, the labor force participation rate has yet to post a meaningful increase and, in fact, declined slightly to 63.5% in February. The good news is that over that last six months the participation rate has held steady compared with the large declines seen earlier in the entire recovery. But until discouraged workers begin returning to the labor force in meaningful numbers, we cannot consider the job market fully healthy.

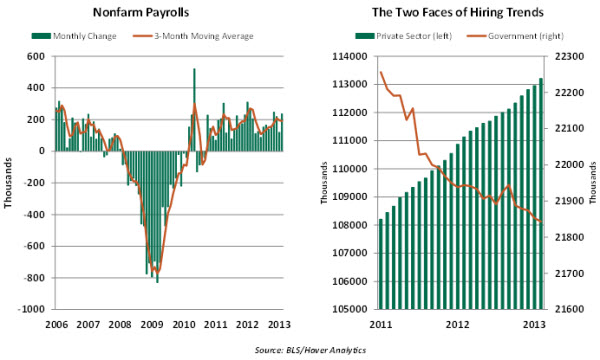

Payroll numbers from the establishment survey underscore that hiring momentum has moved up to a new level. The February increase in payrolls reflects gains in private sector employment (+246,000) and a continued downsizing of government payrolls (-10,000).

The overall workweek stretched 0.1 hour to 34.5 hours in February, while the factory workweek also moved up 0.2 hour to 40.9 hours, a cycle high. Hourly earnings rose 4 cents to $23.82, putting the year-to-year gain at 2.1%. The hourly earnings trend has held above 2.0% for three straight months. The improvement in employment and earnings bode positively for consumer spending in the months ahead.

Yet the projected reduction in government employment caused by the recently-enacted Federal spending “sequester” looms on the horizon. The Congressional Budget Office estimates job losses on the order of 700,000 during fiscal year 2013, ending in September; we may see a significant reduction in hiring over the next three months. This large unknown casts a long shadow on recent bullish economic data such as payroll numbers, jobless claims, auto sales, and purchasing managers’ surveys.

It will be interesting to read the Fed’s statements about the labor market after its March 20 meeting. The latest employment numbers are inching gradually toward the fuzzy criteria of “substantial” improvement, the trigger for moderation in quantitative easing. President Charles Evans of the Chicago Fed places a consistent gain of 200,000 payroll jobs as a suitable indicator, while President Eric Rosengren of the Boston Fed prefers a 7.25% jobless rate, and Vice Chair Janet Yellen is tracking the hiring rate and quit rate. Perhaps more concrete guidelines will be available soon.

For now, the Fed is on hold in the near term until labor market data send an unmistakable message of strength. Although we are making good progress, we are not there yet.

China: Watching Shadows Behind Official Credit Numbers

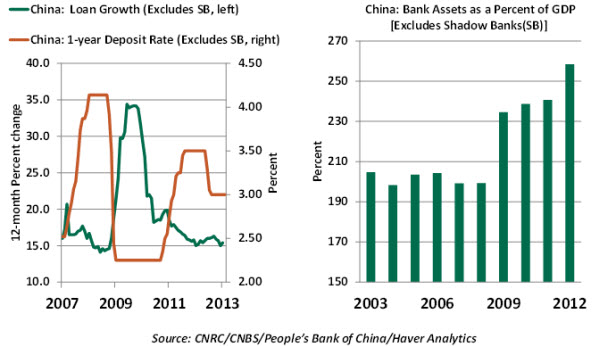

Credit growth in China has moderated in the last three years according to official reports (see chart), after a torrid pace in 2009. But this is an incomplete picture of recent lending trends in the Chinese economy. There is a worrisome surge of credit from the shadow banking sector unfolding behind the veil of official credit data. Private sector estimates place the size of the shadow banking sector anywhere between $2 trillion and $4 trillion, which is about one-fourth to one-half of China’s GDP.

The shadow banking sector is made up primarily of large non-bank institutions, with affluent clientele, acting as trust companies. They offer attractive returns derived from lending to risky customers, off-balance sheet lending by regular banks, and other variations.

A large part of China’s shadow banking sector operates under a legal umbrella subject to only loose regulatory oversight. Wealth management products (WMPs), short-term deposit-like instruments offering very high yields, account for a large part of the shadow banking system’s growth and are off-balance sheet. These high returns lure investors who would otherwise earn only the official deposit rate (see chart), which is small compared with the earnings WMPs promise.

Essentially, customers who purchase WMPs view them as safe deposits but are unaware that they fund, for example, property developers in an overheated real estate market and other risky ventures. Small and medium sized businesses and local governments also receive funds raised through WMPs.

The opacity of WMPs and the mismatch between short-term deposits and long-term liabilities are the shadow banking sector’s fundamental flaws. The creditworthiness of the investments funded by WMPs remains hazy. In addition, there is a practice of using new deposits to repay old deposits and thus conceal failed investments.

Regulators are cognizant of these risks and are making an effort to improve disclosure along with placing restrictions on lending to local governments. But measures of this kind are still on the drawing broad as of this writing.

So, how to distinguish between a “bad” credit boom and “good” credit boom? An International Monetary Fund measure compares private credit growth with that of real gross domestic product to assess whether credit conditions are hazardous. Unfortunately, complete credit data are not available for China. A good proxy is the ratio of bank assets as a percent of GDP (see chart), which in China’s case has registered a sharp increase even without the unprecedented growth in the shadow banking sector.

One school of thought suggests that the shadow banking sector represents the broadening sophistication of Chinese finance, and requires monitoring (as opposed to restriction) at the present time. If regulators clamp down hard on the shady practices of the shadow banking sector, the sector could implode, which not be helpful to economic performance. Despite these views, the rapid growth in credit originating from the shadow banking sector is an explosive financial development that calls for close watching.

The opinions expressed herein are those of the author and do not necessarily represent the views of The Northern Trust Company. The Northern Trust Company does not warrant the accuracy or completeness of information contained herein, such information is subject to change and is not intended to influence your investment decisions.

© Northern Trust