Absolute Return Letter: Expect the Unexpected

“The market is not an accommodating machine. It won’t provide high returns just because you need them.”

Peter Bernstein

The seemingly never-ending debate on passive vs. active investment management is beginning to annoy me. The discussion is one-dimensional and, at times, completely derailed. I shall be the first to admit that the long-only industry has not covered itself in glory in recent years. Nor has large parts of the alternative investment management industry for that matter. It is nevertheless the wrong discussion to have. Much more about this later, but let’s begin elsewhere.

I wrote a letter back in October of last year called When Career Risk Reigns (see here). More recently Jeremy Grantham of GMO published a letter called Investing in a Low-Growth World. The two letters address the same painful subject – how do investors get the most out of a low return environment and what returns can they realistically expect?

When I re-read my own letter from last October a couple of weeks ago after having read Jeremy’s take on the subject, I felt as if there were still some important aspects left untouched. I will deal with at least some of those issues in this month’s letter.

The Emperor wears no clothes

Perhaps I can kick it off by making a few comments on the present situation. Grudgingly embracing the new normal – and in this context ‘new normal’ refers to central bank policy - investors have been fooled into believing that economic fundamentals do not matter anymore. Everything can be controlled through intervention, be it monetary or other, or so we have been led to believe.

Perhaps fundamentals don’t matter for now, but sooner or later - probably later - markets will wake up and realise that the emperor wears no clothes. And the volatility hedge that central banks have so conveniently provided will prove utterly futile. It is not so much because economic growth is likely to disappoint. As many studies have found over the years, economic growth per se is of limited relevance to stock market performance. Many find this hard to swallow, yet the empirical evidence is overwhelming.

My long term pessimism is more a function of the debt outlook. Those who believe that we have made good progress in terms of addressing the high financial leverage in our society must be kidding themselves. Without going into detail (as the picture varies somewhat from country to country), it is fair to say that we haven’t really achieved much so far beyond some re-shuffling of debt from the household and financial sectors to the public sector.

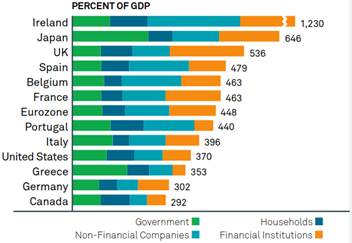

Overall debt levels remain excruciatingly high (chart 1) and I note with some trepidation that Greece is not even close to being the most indebted nation in the world today. In chart 1 debt from all the four main sectors of the economy have been added together. As experience has taught us, it is total debt that matters. Focusing on government debt alone will lead to bad investment decisions.

Chart 1: Gross debt levels in selected countries, 2012

Source: Blackrock, Credit Suisse

Without a healthy level of economic growth there is no way that all this debt can ever be repaid, hence the growing focus on nominal GDP growth, so, in that respect, economic growth still matters.

There is no ‘corporate finance’ solution

I always try to surround myself with bright people. There is no better way to challenge your own ideas than networking with the sharpest knives in the tool box. Recently I discussed the topic of the emperor wearing no clothes with one of the other partners in our partnership. He is not involved day-to-day, yet I consider his regular input extremely valuable in terms of the strategic direction of our firm. Here is what he had to say on the topic:

“There is a long road ahead because of the size of outstanding debts and the fact that nearly everyone is running a primary deficit. It is not possible to generate a growth trajectory which allows an escape from this debt without a proper cleansing / different policy response.

That means the big adjustment is to get used to lower returns and lower growth for the foreseeable future. Nevertheless, governments will try and engineer a way out - with all sorts of attempts at monetizing the debt. But there is no ‘corporate finance’ solution.

This will lead to a lower per 'unit of account' purchasing power for the average citizen, either via higher taxes, inflation, currency depreciation or indeed a combination of all three.

Meanwhile the sheer volume of outstanding financial claims vs. the productive economy will likely see further rolling bubbles and higher real economy volatility. Avoiding the [fallout from the] bubbles will be a key strategic objective.

The only way to make real money will be by improving returns gained on the passive alternative, e.g. excess returns from outperformance, improving an asset, reducing costs, managing tax efficiently. The return from falling discount rates is well and truly over.

Therefore maintaining current purchasing power without materially losing capital will make you a big winner - in time to pick up the new bull wave when it arrives - which it eventually will.”

A common thread that runs through my partner’s observations, my October 2012 letter and Jeremy’s latest letter is the topic of low economic growth and to what degree we should expect low growth to lead to low returns?

This is a critical question, not only given the current environment of mildly negative real rates but also because more and more central banks around the world appear to be switching their focus towards nominal growth. As I see it, negative real rates are an integral part of such a policy change. It is therefore not unreasonable to expect real rates to remain flat to negative for years to come. At Absolute Return Partners we actually expect a widening of the spread, as we project inflation to rise faster than bond yields over the next few years.

The impact on returns from negative real rates

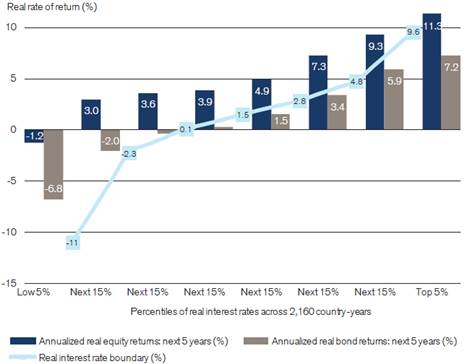

Intuitively you would expect a strong positive relationship between real rates and subsequent real returns on bonds and equities, but is there any evidence to support that thesis? To find the answer I turned to Credit Suisse’s Global Investment Returns Yearbook 2013.

The answer to that question is an emphatic YES, but the path to it is a wee bit complicated so allow me to explain. The authors of the study began by calculating real interest rates every year during the 1900-2012 period on each of the 20 countries in the study. Following that, real equity and real bond returns were calculated for the subsequent 5 years, leading to a total of 2,160 observations (20 countries times 108 overlapping 5-year periods between 1900 and 2012). Those observations were then ranked from lowest to highest real rates and 8 bands were established (lowest 5%, next 15%, etc. – see the x-axis in chart 2).

Chart 2: Real returns vs. real interest rates, 1900-2012

Source: Credit Suisse Global Investment Returns Yearbook 2013

Some important observations can be made on the basis of chart 2. For example, when real rates have been negative in the past (i.e. when the light blue line is below the x-axis), real bond returns and real equity returns have been either low or negative over the following 5 years. The opposite is the case when real rates have been strongly positive. In other words, what we expected intuitively turns out to be true.

A couple of observations to supplement this analysis: Although interest rates are near all-time lows in many countries, real rates are not. Most countries currently fall into the third or fourth band (when counting from the left), suggesting that real bond returns should be near zero over the next 5 years, whereas real equity returns should annualise 3-4%. The other, and perhaps more pertinent, observation is that most episodes of negative real rates have occurred during periods of high inflation. The present one is occurring during a low inflation period and during a period where asset prices are being heavily manipulated through central bank intervention. One may thus have to be careful in terms of how the data is interpreted.

Chart 2 is essentially another way of measuring the equity risk premium, which measures the excess return - over and above the risk-free rate of return - equity investors have earned over time for taking equity market risk. I prefer this measure of the equity risk premium to the more traditional (static) approach, as the equity risk premium is far from stable. For example, during much of the last decade, it was negative, leading to equity investors being punished for taking equity market risk (chart 3). The dynamic approach used by the authors of the Credit Suisse Yearbook addresses this problem by distinguishing between different real rate regimes.

Chart 3: U.S. equity risk premium, 1935-2012

Source: Barclays Equity Gilt Study 2013.

Note: Measures 10-year annualised excess return of equities relative to bonds.

The correlation conundrum resolved

Another dynamic which equity investors are well advised to consider is how equities and bonds interact. Over time the correlation between the two has shifted back and forth with the investment community ‘agreeing to disagree’ as to the underlying causes. A recent analysis provided by Guggenheim Investments has cast new light on the relationship between equity and bond prices, and the results are quite intriguing.

What the smart guys at Guggenheim have found is that the last half century (1962-2012) can be divided into three distinctly different regimes:

- when U.S. 10-year bond yields trade below 4%;

- when U.S. 10-year bond yields trade between 4% and 6%; and

- when U.S. 10-year bond yields exceed 6%.

During the first regime the correlation between equity and bond returns has been consistently positive. When the yield has exceeded 6%, the correlation has been negative. When the yield has traded in the range of 4% to 6% no clear picture has emerged (chart 4).

Chart 4: Equity-Bond correlations in different yield environments (1962-2012)

Source: Guggenheim Investments

Based on the Guggenheim analysis, with the U.S. 10-year bond currently yielding just below 2%, one should expect a further drop in bond yields to have a negative impact on equity prices. Likewise, should bond yields begin to rise modestly from current levels to, say, 2.5% or even 3%, equity prices should actually strengthen. I believe that may take one or two equity bears by surprise!

A new take on active versus passive

Let’s change gear and focus on the trend away from active management towards ETFs and other passive investment vehicles, a trend which by and large has been driven by poor performance amongst active managers. I am not at all convinced that now is the appropriate time to go passive, though. Years (well, decades) of experience has taught me that the more buoyant the markets are, the more difficult it is to outperform the index; however, during more challenging times, an active manager has the odds stacked much more in his favour.

Let’s assume for a second that, for most OECD nations, real rates will hover in the range of zero to -2% over the next few years, and let’s also assume that the equity risk premium will average around 4%. That should give investors the prospects of a real return of 2-4% per annum on their equity investments (5-7% nominal returns annualised given our inflation expectations). Now, that is a hurdle which the average active manager has a fair chance of exceeding.

Despite this logic, the trend towards passive is relentless. Being little more than a cottage industry in 2000 with less than $100 billion under management, ETFs today manage over $1.5 trillion between them and there are no signs of any slowdown in growth (chart 5).

There is more to the story than poor performance, though. I went on a business trip to Copenhagen only a couple of weeks ago. Whilst there I met with several pension fund managers who gave me insight into what is on their minds at moment. The expense ratio was pretty much all they talked about (well, I exaggerate only modestly). Why this obsession?

It turned out that the Danish pension funds have just been subjected to a study measuring performance and expense ratios (amongst other things), and the study showed that, with few exceptions, those pension funds with the highest expense ratios have delivered the poorest returns over recent years. As one CIO said to me, in a rational discussion between two investment professionals it is easy to agree that it is the return after fees that one should focus on. However, when the supervisory board (which consists mostly of non-professionals) convenes, the discussion very quickly turns to expense ratios in absolute terms. It is much easier for a lay person to grasp and, in a low return environment, it is a relatively easy case to argue even if it is fundamentally flawed.

Chart 5: Growth in ETFs, 2000-2012

Source: iShares, Blackrock

Herding is a powerful factor in all aspects of life but particularly so in the field of investments. Just like herding drives stock prices up and down, it is also the fundamental force behind trends like the move from active to passive. There are few things in life that are worse for an investor than sitting at a dinner party amongst friends to find out that their returns have far exceeded his. At the most basic level, herding is a survival mechanism. It expresses itself in numerous ways. In our industry we often refer to it as career risk.

So, whilst perfectly understandable, is the decision to go passive the correct one? There is a whole raft of issues which most passive investors have chosen to ignore. Who says, for example, that a market cap weighted index such as the S&P500 is the right benchmark choice? A simple equally weighted benchmark would do better in most years. What about survivorship bias in the index world? Do not think for one minute that it is only an issue in the world of active management. And what about performance in absolute terms? Is it really good enough that you perform as poorly as your peer group? I thought not.

I could go on and on but shall spare you the pain. Before I rest my case, though, I would like to share with you a recent article from the FT called ‘ A new take on the active vs passive debate’ (see here). The article makes the interesting point that you cannot assume that just because the average fund may underperform, the average investor will also underperform. The logic is straightforward. The industry standard when calculating performance is to assign an equal weight to all funds. This may in some instances lead to highly skewed results. The following is a quote from the article, written by Merryn Somerset Webb:

“Take the [UK] equity income sector for example. At the beginning of 2012 there were 92 funds in it. But Neil Woodford, via just three Invesco Perpetual funds, was responsible for running 40 per cent of all the money invested in it; his funds together were bigger than 84 of the remaining 89 funds combined. Yet if you simply added up the performance of the funds and divided by 92, as any conventional analysis would, his funds would account for only 3.3 per cent of the sector performance.”

A simple example to illustrate the problem: Assume we have a mutual fund sector with only 2 funds in it. One accounts for 90% of assets under management and is up 10% year-to-date; the other one which accounts for only 10% of assets under management is down 10% year-to-date. A conventional analysis of the sector will show the performance to be flat year-to-date whereas an asset weighted approach will show the return to +8%.

As funds under active management tend to flow from the poorer performers towards the stronger ones, it is fair to assume that the average investor has performed considerably better than the industry statistics suggest. There is actually evidence to back up this claim. According to a recent study which the FT article refers to:

“…over the past five years, in almost all cases the average [UK] investor is doing better than the average fund.”

Conclusions

So, to sum it all up, those who argue furiously for a passive approach in a low return environment are at risk of getting it horribly wrong longer term. Costs do make a difference when returns are low, hence the appeal of a passive, low-cost approach in the first place. However, if active managers respond rationally to the passive onslaught, their fees will be slashed, making the cost argument largely redundant. At the same time, more money being managed passively means less efficient markets and less competition for good ideas which, all other things being equal, should result in active managers finding it easier to outperform their passive peers.

Eventually, active long-only managers will have lowered their fees sufficiently that cost will no longer be a significant issue in terms of choosing between passive and active management and investors will direct their attention elsewhere. The distinction between alpha and beta providers will become more prominent, and investors will be prepared to pay the higher fees only to investment managers who can document the ability to deliver alpha over time (and not many can do that). Charging performance fees on a strategy that is driven primarily by market returns (beta) will become a thing of the past.

Investors will also increasingly be prepared to pay for asymmetric returns as opposed to symmetric returns. For those not familiar with this terminology, asymmetric returns are what hedge funds are supposed to be all about, even if many of them have not lived up to the hype. An asymmetric return profile suggests that the manager captures significantly more of the upside delivered by the markets than he participates on the downside when markets turn sour.

Asymmetric returns are extremely attractive to an underfunded pension sector which cannot afford large draw-downs; however, it is a difficult skill to master. As investors become more and more sophisticated and they educate themselves further about alternative investment management techniques, this is a skill set which they will be prepared to pay high fees for.

Niels C. Jensen

4 March 2013

© Absolute Return Partners LLP 2013. Registered in England No. OC303480. Authorised and Regulated by the Financial Services Authority. Registered Office: 16 Water Lane, Richmond, Surrey, TW9 1TJ, UK.

Important Notice

This material has been prepared by Absolute Return Partners LLP ( ARP). ARP is authorised and regulated by the Financial Services Authority. It is provided for information purposes, is intended for your use only and does not constitute an invitation or offer to subscribe for or purchase any of the products or services mentioned. The information provided is not intended to provide a sufficient basis on which to make an investment decision. Information and opinions presented in this material have been obtained or derived from sources believed by ARP to be reliable, but ARP makes no representation as to their accuracy or completeness. ARP accepts no liability for any loss arising from the use of this material. The results referred to in this document are not a guide to the future performance of ARP. The value of investments can go down as well as up and the implementation of the approach described does not guarantee positive performance. Any reference to potential asset allocation and potential returns do not represent and should not be interpreted as projections.

Absolute Return Partners

Absolute Return Partners LLP is a London based client-driven, alternative investment boutique. We provide independent asset management and investment advisory services globally to institutional investors.

We are a company with a simple mission – delivering superior risk-adjusted returns to our clients. We believe that we can achieve this through a disciplined risk management approach and an investment process based on our open architecture platform.

Our focus is strictly on absolute returns. We use a diversified range of both traditional and alternative asset classes when creating portfolios for our clients.

We have eliminated all conflicts of interest with our transparent business model and we offer flexible solutions, tailored to match specific needs.

We are authorised and regulated by the Financial Services Authority.

Visit www.arpinvestments.com to learn more about us.

Absolute Return Letter contributors:

|

Niels C. Jensen |

Tel +44 20 8939 2901 |

|

|

Nick Rees |

Tel +44 20 8939 2903 |

|

|

Tricia Ward |

Tel +44 20 8939 2906 |

© Absolute Return Partners