This week we focus very briefly on the sequester and Federal government employment and then revisit a subject that has faded but has the potential to reappear this Spring and Summer (the drought) and conclude with a quick look at housing prices.

Well, as expected (how awful that this is what I’ve come to expect from our elected officials), the can was kicked down the road. What will be interesting is what transpires over the next month or two with more deadlines pending. The media is all over the sequester and the politicians are in full blame game mode with each side pointing out the horrible things we can all expect very shortly. There are others who say, “the impact for the coming year is only .5% to GDP.” That may be insignificant when the economy is healthy but it can be somewhat dire if GDP growth starts to trend the wrong way. Think of our friends across the pond.

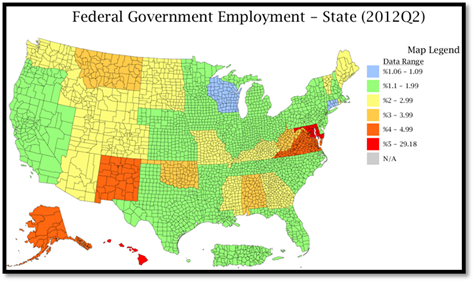

Previously, we’ve looked at reliance on Federal funds and defense expenditures as a percentage of GDP. We think it is worth considering the impact of further employment cuts or furloughs and the impact on tax receipts. The below map gives a sense of Federal Government Employment as a percent of employment within each State. You can’t see DC due to its size but it is bright red (29.18%).

Source: DIVER Analytics; Map Module; Bureau of Labor Statistics

The “good” news is that Federal Government employment as a percent of overall employment is up in only Nevada and the Virgin Islands since the second quarter of 2011. However, when contemplating the impact, we should think about tax receipts impacted by furloughs as well as programs that are cut due to grant reductions and cuts to or elimination of Federal contracts. We suspect this impact will not become obvious for another quarter or two. Who knows, maybe we’ll be surprised and the folks in DC will get down to business and construct a real solution.

Speaking of which, while media lost sight of the muni industries plight regarding tax-exemption and the 28% cap, market participants attending several of the recent conferences have been pretty vocal on the subject. We continue to encourage all market participants to make their voices heard. We refer our readers back to an excellent commentary from our friends at Bernardi Securities, Tax Exempt Municipal Bonds, The Case for an Efficient, Low-Cost, Job-Creating Tax Expenditure. http://www.lumesis.com/pdf/Bernardi-Securities-Inc-White-Paper.pdf.

Drought

Remember the drought folks focused on this past summer? It did get kind of lost in the election season. Well, we’ve been tracking this data since June or so and there is some decent news and some things to take note of as Spring approaches.

Lets start with some good news. The map to the left shows where drought conditions stood as of December 11 and the map to the right depicts how things stand as of February 26. Things have gotten worse in less than 10% of the counties and “only” 720 counties are in a “Severe Drought” or worse according to the National Drought Mitigation Center as of February 26, 2013 compared to 947 on December 11, 2012.

Source: DIVER Analytics; Map Module; National Drought Mitigation Center

Source: DIVER Analytics; Map Module; National Drought Mitigation Center

While things have gotten a bit better in some places, there is still quite a bit of red on this map and, according to some recent reports, a less than snowy winter across the middle part of the country will not help those areas coming out of winter. Let’s hope for some snow and rain for the affected areas. We encourage our readers to pay attention to the impact on those local economies (employment and tax receipts) and the rest of us (crop prices) over the coming months.

Housing

Our last data point this week is around housing. Recently, we have looked at delinquencies and foreclosures. This week, we take a look at housing prices at the county level (this goes a bit deeper than some other sources that focus on the largest metro areas). Looking back over the one year period, 4Q 2012 to 4Q 2011, the good news is prices are stable or increasing in 1,520 counties. That’s about one-half the country. If you were to look at 4Q 2012 v. 4Q 2010 you would see similarly positive news. However, we remind readers that we need to look from where we have come. If we look back to 4Q 2007, 2008 and 2009, housing prices are equal to or greater now than they were then in about one-third of the counties. The impact: assessed values (property tax receipts). Let’s hope the trend of rising prices continues.

And now that to a great piece by John Mauldin, “How Not to Run a Pension”. http://www.mauldineconomics.com/frontlinethoughts/how-not-to-run-a-pension-proofing. If you are interested in obtaining detailed pension data for more than 900 State and City pension plans, please send us a note at [email protected] or call us at 203-276-6500.

This Week’s Function Update and Data :

- In response to requests from our users, we have created a new module that allows for the geographical assignments of issuers to be customized. This new module empowers clients to override the default location assignment of specific issuers within DIVER. Company Administrators can quickly and easily modify locations to a different State, County, City/Town, or School District.

- FEMA Disasters, County, Feb 2013

- Weekly Initial and Continued Jobless Claims, State, 2/16/2012

- Drought Intensity, County, 2/26/2013

- House Price Change and House Price Rank Change, 2011 Q4 - 2012 Q4, State

- Housing Price Index, County & State, 2012 Q4

On the Road : Gregg and Mike will be at the IAA Summit in Arlington, VA. Come visit our booth.

Gregg L. Bienstock

CEO& Co-Founder, Lumesis, Inc.

© Lumesis