- There are more sellers than buyers in the world economy

- The recent Italian election may usher in renewed instability

- US bank lending is finally expanding, but not everyone is happy about it

Our family is not taking a spring trip this year. That announcement was greeted with howls of protest from my children, who seem to think that March travel to warmer climates is a basic human right. But I reminded them that our finances had already been taxed by various school trips, team trips, and the need for new carpeting. The latter was brought on by callous disregard for our rule against eating chocolate pudding in the family room.

It’s certainly challenging to some sensibilities when budget constraints become more binding. Prosperity can make everything seem affordable, and recession can make everything seem expendable. Over the past four years, corporations have cut costs aggressively and governments around the world are engaged in austerity programs of varying degrees.

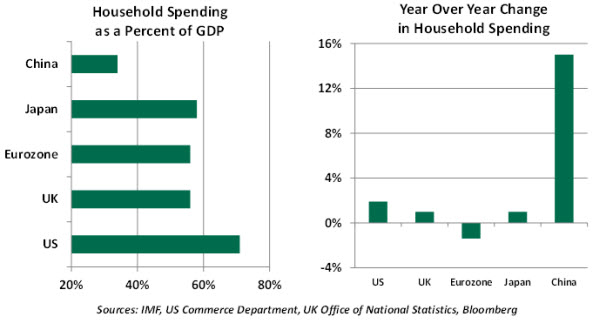

But renewed frugality among households is perhaps the most significant trend of the times. With one notable exception, consumers around the globe have been tightening their belts, and there seems to be no end to their thrift. Given the role that personal spending plays in the world economy, this represents a real constraint to growth.

Household spending accounts for more than half of gross domestic product (GDP) among the G-7 countries, with a peak of more than 70% in the United States. For many years, America was thought to be the consumer of last resort in the world, allowing other countries to grow substantially through exports. Today, that strategy is not as attractive.

In many major markets, a series of factors has constrained personal consumption.

High levels of joblessness. Unemployment and underemployment are still steeply elevated. This directly limits the spending power of those out of work and indirectly limits the spending power of those working by placing downward pressure on wages.

More restrictive credit conditions. Many financial institutions are still working out from under bad loans soured by the Great Recession. In some cases, work to reinforce liquidity and capital is unfinished. Creditworthiness isn’t what it used to be, and additional regulation governing consumer credit is also a hindrance.

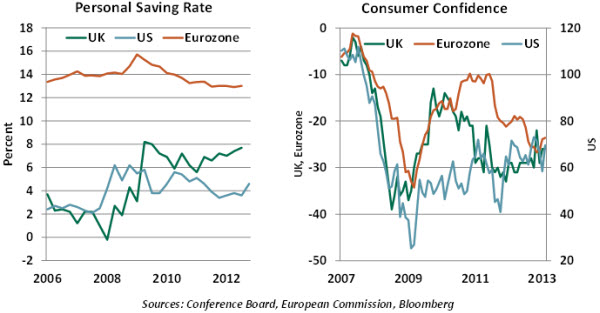

Rebuilding saving. The retreat of real estate values and significant market corrections diminished household net worth and hampered the finances of public and private pension systems. Job interruptions have prompted a further depletion of savings. With the postwar generation approaching retirement, we might expect a renewed emphasis on saving, a trend which appears to be underway in the United States and the UK.

Uncertainty. With the outlook for economic activity and policy very much unclear, confidence levels are still well off their pre-recession peaks. Worried consumers typically spend much less freely.

Restrictive Fiscal Policy. In an effort to close budget gaps, Western countries have increased taxes and cut outlays. Both tend to reduce household spending power; in the United States, the restoration of the payroll tax to its normal level made January a very unpleasant month for many major retailers.

It is certainly hard to generalize about consumers across countries, since tastes and habits vary considerably. But it seems fair to conclude that household spending in America, Europe, and Japan may proceed on a shallow trajectory. Producers in those areas will count on exporting as the path to growth… but who will be in a position to buy?

In seeking to answer this question, many are looking to China. Consumption in that country is a very small fraction of GDP, but it is growing rapidly as China’s middle class expands and becomes more prosperous. Yet China will be seeking to take advantage of its own domestic demand to buffer a drop in its exports, so it’s not clear that Chinese consumers will be able to take up the slack for lost demand elsewhere in the world.

The clearest and cleanest way to restore consumption growth is by renewing job creation. This will foster improved income growth and ease budget constraints. Policy in all regions should remain keenly focused on this objective.

It’s sometimes said you should be careful what you wish for. If my kids continue their carping about a spring “staycation,” I might announce that we’re going to take a long family car trip. Audio and video devices would be forbidden, in favor of parental lectures on the evils of drinking, dating, and eating chocolate pudding in the family room. Compared to that, a boring week in the house might not seem so bad.

Italian Voters Turn Away from Austerity

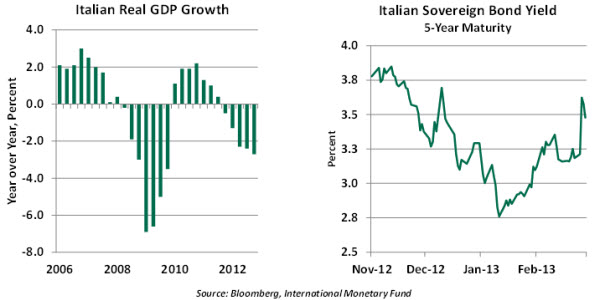

The results of last weekend’s parliamentary election have brought political confusion back to Italy, with a quarter of voters supporting an anti-eurozone populist movement and no party able to control the upper house. With the economy mired in recession and fiscal reforms desperately needed to return the economy to growth, a weak or short-lived government bodes ill for the outlook.

In the voting for the lower house, the center-left Democratic Party (PD) alliance did not perform as well as expected (29.5% of the vote) but did manage to emerge with the largest bloc, automatically giving it a majority of the seats. Surprisingly, former Prime Minister Silvio Berlusconi’s People of Freedom (PdL) alliance did far better than expected (29.2%), coming within a whisker of beating the PD. Even more surprising was the stunning 25% of the vote claimed by the populist protest Five-Star Movement (M5S), led by comedian Beppe Grillo.

The political stalemate comes about because the upper house (Senate) is deeply divided. The Italian Senate has almost as much power as the lower house, making control of both houses critical if a government is to make any real legislative progress. The centrist group of former Prime Minister Mario Monti won only about 10% of the vote and only 18 seats in the Senate, leaving him unable to play the role of kingmaker.

A return to political confusion matters deeply for Italy because the economy is mired in its worst recession in 20 years. Real GDP fell 0.9% in the fourth quarter of last year, the sixth consecutive quarter of decline. The unemployment rate exceeds 11%, and youth unemployment is even higher. Labor market and structural reforms are desperately needed in order to boost competitiveness – particularly with Italy falling even further behind the likes of Spain in that process.

Although the headline fiscal deficit is running below 3% of GDP, years of public finance neglect under Berlusconi have left Italy with a public debt burden at 127% of GDP, surpassed only by Greece in the eurozone.

On the plus side, the sheer size of Italy’s debt means that funding costs would have to spike for an extended period of time before the average cost of the overall debt burden became unsustainable. Italy has already met about 20% of its issuance target for 2013.

However, a revisit of the market stresses of late 2011 would quickly make it difficult for Italy to meet the remaining 80% of needs for 2013. A bond auction held shortly after the election found yields at their highest level since last fall.

Italian voters are clearly fed up with talk of reform and austerity. Berlusconi (ever willing to say whatever it takes to win votes) campaigned on a platform of tax cuts and no more reform. M5S leader Beppe Grillo went even further and called for a referendum on Italy’s eurozone membership. Some two-thirds of Italian voters thus rejected the tentative reform steps undertaken by the Monti administration. Strong support for Five-Star is indicative of a crisis of legitimacy across Europe, with voters in many countries rejecting established political parties. Efforts to impose reform and austerity on uncompetitive economies are firmly identified with Germany, making such reforms even harder to impose.

The traditional Italian parties will try to avoid a new election as long as possible in the hopes that Five-Star will lose some of its momentum. However, the markets will be looking for a fast solution to the stalemate. Once it becomes apparent that a PD-led minority government, or a grand coalition of the PD-PdL, will mean a weak and ineffective government, pressure for fresh elections under a new system will increase.

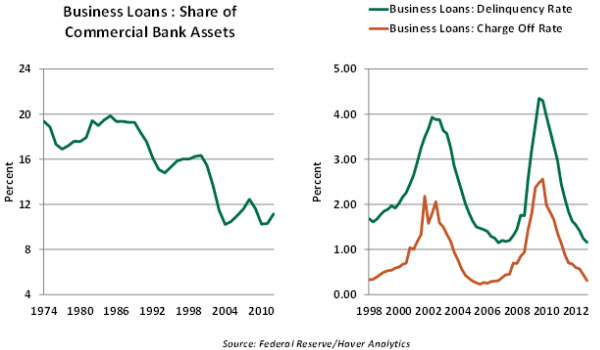

Recent Trend in Bank Loans to Business – Does It Raise a Red Flag?

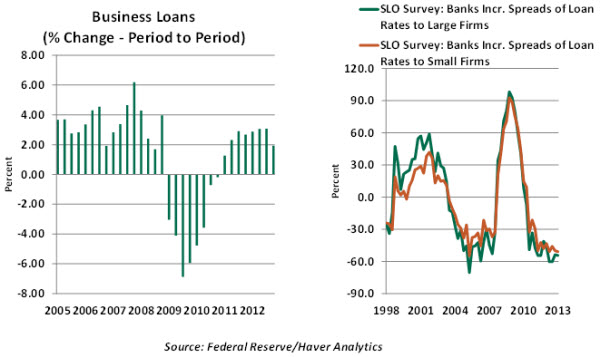

Banks are back in the business of lending to households and firms after shrinking their loan books for nearly three years following the collapse of Lehman Brothers in 2008. Loan extensions to businesses show stronger growth compared with that of households and have made headlines in the financial press of late. A recentWall Street Journalarticle reported noticeable growth in bank lending to businesses at significantly low spreads and reminded readers of attendant risks. We have been tracking these data closely and our findings suggest that there is nothing to be too concerned about.

Loans to businesses have increased $262 billion to roughly $1.5 trillion during the two years ended 2012 after declining $426 billion during the Great Recession and thereafter. But bankers report that the spreads they earn from these loans are paltry. The historically low interest rate environment has spurred firms to raise funds in the bond market and contributed to trimming spreads on bank loans.

Low spreads are interpreted as aggressive bank lending to increase market share. However, the share of business loans in the balance sheet of banks indicates that there is little reason to be alarmed by their advancing trend. Business loans made up about 12% of commercial bank assets in the fourth quarter of 2012, up from a low of about 10% at the onset of the recession. Also, from a historical perspective, the current share of business loans does not stand out.

The quality of loans that banks hold is another important facet to consider. The delinquency rates of business loans in the final months of 2012 declined to a level seen well before the crisis commenced. The main conclusion is that traditional indicators of the quality of businesses loans are not sending warning signals yet.

Before we declare that bankers have not thrown caution to the wind, it is critical to recognize that loans that sour during weak economic conditions most often originate during the upswing of business activity. This history will certainly have to be respected. But banks have taken criticism for not making enough loans, and now seem to be getting called to task for making too many. It’s hard to find a middle ground.

The opinions expressed herein are those of the author and do not necessarily represent the views of The Northern Trust Company. The Northern Trust Company does not warrant the accuracy or completeness of information contained herein, such information is subject to change and is not intended to influence your investment decisions.

© Northern Trust