ING Fixed Income Perspectives February 2013

Bond Market Outlook

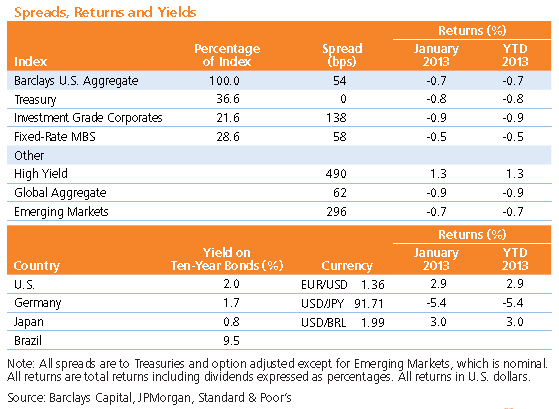

Global Interest Rates: Yields have largely corrected toward fair value, but we still prefer credit risk to interest rate risk; we are underweight duration in the U.S.

Global Currencies: We remain bearish on the U.S. dollar, yen and pound sterling, though our outlook on the euro has improved.

Corporates: Spreads are fairly valued, but we have taken a more neutral stance given weakening fundamentals and increasing event risk.

High Yield: Spreads continue to offer attractive compensation for default risk, though we have tempered our long-term view given low all-in yields and limited upside.

Mortgages: The Fed continues its commitment to agency MBS purchases, providing strong technical support for mortgages.

Emerging Markets: We favor local-currency sovereigns, as EM currencies are poised to strengthen; we prefer high yield within both sovereigns and corporates.

Macro Overview

- Despite its diminutive size, February has been a whirlwind. Eat and drink too much on Fat Tuesday, be reminded of our corporeal nature on Ash Wednesday, receive a sappy Hallmark card on Thursday, and cap it all off with a memorial for a bunch of ex-presidents on Monday. Unfortunately, the next several weeks don’t appear to offer any relief from this calendar whiplash.

- U.S. politicians have a March 1 date with unfinished fiscal business, and our expectation is that brinksmanship will remain the prevailing strategy. Even if a last-minute deal ultimately proves elusive, however, the impact of the sequester — equal in scale to about one month of the Fed’s expansionary bond-buying programs — will not cause excessive long-term fiscal drag. March 8, meanwhile, will see the latest release of nonfarm payrolls data, which have become the primary indicator by which we divine the intentions of the Fed. Though the labor market should continue to show signs of improvement, the Fed’s current policy of low target rates and aggressive quantitative easing will remain intact until the unemployment level finds its way down to 7%.

- While Europe is not expected to contribute significantly to global growth this year, the tide has turned from complete economic meltdown to mere stagnation — to the benefit of market sentiment. The euro has appreciated 12% from August’s lows and is now approaching levels that could challenge the competitiveness of some countries’ exports; ECB chief Draghi does not consider the currency risk to be an immediate concern, however. Italian political risk, on the other hand, has intensified as the market-unfriendly Italian conservative coalition led by former PM Berlusconi continues to pick up momentum in advance of the country’s late-February elections.

- Another noteworthy event on the horizon is the appointment of a fresh Bank of Japan governor. The new chief will inherit Prime Minister Abe’s promises of bold action to jumpstart an economy that has stagnated for years. The BOJ’s approach to addressing these promises will have significant implications on the direction of the yen, which has already weakened considerably in 2013, as Japan looks to a weaker currency to help bolster its export base and counteract the forces of deflation.

Sector Overviews

Global Interest Rates

- Yields have largely corrected toward fair value. The January selloff in the U.S. did breech prior support levels and appears to have established a new range of 1.8–2.1 on the ten-year Treasury. The direction of U.S. interest rates going forward will depend on macro fundamentals like payroll data. Strategically, global growth and inflation will be sufficient to erode value at current levels, which should continue to pressure rates higher over time. As such, our bias continues to be underweight duration in the U.S.

- Even amid modest global growth and a relatively stable Europe, we maintain a negative bias toward specific euro zone nations such as France and Spain given unsustainable debt dynamics and sluggish economic growth. We still favor Italy on a relative-value basis versus Germany but are cautious in light of heightened political risks. We believe U.K. Gilts make an attractive alternative to German bunds.

Global Currencies

- Given the structural weakness in the U.S. dollar, we continue to favor higher-yielding currencies like the Indian rupee that can tolerate modest global commodity inflationary pressures. In addition, we may also look to currencies such as the Mexican and Philippine pesos, as flows into emerging markets continue and Chinese growth spreads to surrounding countries.

- We are bearish on the U.S. dollar, yen and pound sterling, though we have grown more constructive on the euro given the less-dire outlook for Europe. We also hold in low regard the Canadian and Australian dollars given weaker global demand.

Investment Grade Corporates

- Strong private sector demand, stabilization in Europe and a more positive growth outlook for emerging markets are supportive of investment grade spreads. Fundamentals have begun to deteriorate, however; fourth quarter sales and earnings growth generally exceeded expectations, but year-over-year growth rates continued to decelerate and event risk is a legitimate threat.

- The technical environment remains supportive, as investors continue to search for high-quality spread assets. Heavy new-issue supply, however, has weighed on the market in recent months and inhibited spread tightening. Spreads appear fairly valued; however, with earnings and sales growth only mildly positive and event risk increasing, a more neutral stance is warranted.

High Yield Corporates

- High yield spreads continue to offer attractive compensation for default risk, though low all-in yields and near-record-high dollar prices limit upside from current levels — particularly given the callable structure of most of these securities — and have tempered our longer-term view.

- Solid balance sheets limit the risk of a near-term spike in defaults, though credit momentum has begun to wane as evidenced by increased mergers and acquisitions/leveraged-buyout activity. The primary near-term risk to the asset class is the macro environment, as Europe remains in recession and the United States has only partially addressed its fiscal challenges.

Mortgages

- The Fed continues its commitment to purchase roughly $60–80 billion of agency MBS per month — which equates to 50% of gross monthly issuance — for the foreseeable future, providing strong technical support for mortgages. However, as agency RMBS continue to trade at a premium, borrower prepayments and directional swings in rates remain salient factors in the performance of mortgages. Adjustments to HARP and other accommodative government policies are inducing faster prepayments; combatting these factors are rising fees levied by the Federal Housing Administration and government-sponsored enterprises, originator capacity constraints and borrower burnout.

- In non-agency RMBS, increased demand for housing and continued improvement in housing prices bode well in the longer term. While significantly tighter on a year-over-year basis, relatively wide credit spreads continue to attract yield-hungry investors.

- In CMBS, the refinancing boom continues, fueled mostly by the low-rate environment; the largest new-issuance pipeline since the credit crisis is slated to clear in 2013. Demand is currently strong and appears sufficient to keep the asset class well-bid in the near term.

Emerging Markets

- Sovereign net issuance is expected to be relatively low in 2013; spreads in both hard- and local-currency debt are attractive and should continue to grind tighter. However, we currently favor local-currency sovereigns over hard-currency, as EM currencies are poised to strengthen. Intervention risk — for example, the risk the Bank of Japan actively weakens the yen — is a concern, particularly as positioning in local currency has become heavy and flows robust.

- Profitability and leverage for emerging market corporates have ticked up, but fundamentals remain stable. The technical backdrop is not as supportive, as the market has had difficulty absorbing record new-issue supply. We prefer high yield over investment grade within both sovereigns and corporates.

ING U.S. Investment Management’s fixed income strategies cover a broad range of maturities, sectors and instruments, giving investors wide latitude to create a new portfolio structure or complement an existing one. We offer investment strategies across the yield curve and credit spectrum, as well as in specialized disciplines that focus on individual market sectors. We build portfolios one bond at a time, with a critical review of each security by experienced fixed income managers. As of December 31, 2012, ING U.S. Investment Management managed $127 billion in fixed income strategies in the United States.

This commentary has been prepared by ING U.S. Investment Management for informational purposes. Nothing contained herein should be construed as (i) an offer to sell or solicitation of an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. Any opinions expressed herein reflect our judgment and are subject to change. Certain of the statements contained herein are statements of future expectations and other forward-looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) increasing levels of loan defaults, (5) changes in laws and regulations and (6) changes in the policies of governments and/or regulatory authorities.

Past performance is no guarantee of future results.

© 2013 ING Investments Distributor, LLC • 230 Park Avenue, New York, NY 10169

CID 5825