Markets were looking for a reason to correct. Risk assets had outpaced themselves since mid November and in the first seven weeks the S&P[1] had outperformed the US Treasury 10-year note by 12% and the 30-year bond by 15%. There was no major event to the week. Just fatigue rollover and a mildly negative spin on theFOMCminutes. The markets will lumber through the sequester and face the next test on the debt ceiling and first quarter results. Below the surface, the outlook is mildly optimistic. Why the qualifier? Because everything, in Europe, US and Japan, must be set in the context of the asset deflation and deleveraging going on and that will go on for some years. In all this, the US is best placed to continue to outperform but it will remain subdued by any past measure.

Let's take as our start of the modern economic era Tawney's definition of the Reformation as the "rise of capitalism." So 500 years. Plot this on a calendar of January to February. Our first meaningful record of any national accounts came in 1665, so late April, from William Petty in the form of an income, expenditure and physical assets count. Adam Smith came along in mid-July and global value added measures came with Michael Mulhall in early September. The first measure of GNP came in October (Meade and Stone). Post-war data improved steadily in mid-October and everything we use as historical precedent dates pretty much from then on. Sure, there's some strong inferred data and extrapolation from the Depression era from October 1st to October 8th and we can use those. But heavy real time data only started to improve around December 10th and in some cases, like integratedECdata, it starts around December 20th. The Great Recession started December 26th and the latest round of QE started around 10.00pm on December 31st.

Apologies to Carl Sagan for all this. But the point is that we're flying sight-impaired on much of the economic issues we face today. Our national economic databases, everything in the FRED series, would likely fit onto an iPhone. We just don't have that much information. And that's why we have little consensus on what we face and what to do about it. So economists and politicians rage. The economic torpor sludges on.

We were reminded of this last year when theIMFcame out with a very big "whoops" on fiscal multipliers saying that they were around 1.7 not 0.5. And this meant that a fiscal austerity cut of €1.00 would not contract the economy by €0.5 but €1.7. And again last week when a 500 page report thumped on our desk from the European Commission that made some startling points: i) that fiscal consolidation killed aggregate demand when it was meant to inspire confidence ii) that a new divide of falling output and massive unemployment has risen within the EU iii) that larger welfare states have tended to higher employment rates iv) that of 23m unemployed, 10m are long-term unemployed (which in the EU is defined as one year, not the US definition of 27 weeks) and one in five of those have never had a job v) that raising minimum wages improves the fiscal outlook and v) automatic stabilizers, which are merely counter cyclical expenses, worked.

Stay with me. We're nearly done. Another report tracing the banking crisis also made some counter intuitive conclusions: i) that risk averse economies are more prone to crisis, because savers want safe and liquid assets which means banks can't take on longer term assets and spreads decline ii) labor market flexibility increases the probability and severity of a crisis because workers over produce and then cut production more quickly iii) high uncertainty leads to crises and the higher savings, lower loan supply and financial sector fragility cycle starts anew.

So what? Well, this stirs up the economic debate quite a bit, even if we brush this off with "well, that's Europe; the US is different…and in a good way." It suggests strongly that our policy and debates hold no adamantine rules. And that the slow income growth, high savings, slow output and high unemployment have no easy solution of "spend more or cut more but for goodness sake, decide which." With apologies to Donald Byrd who died two weeks ago, it is a slow drag.

FOMC

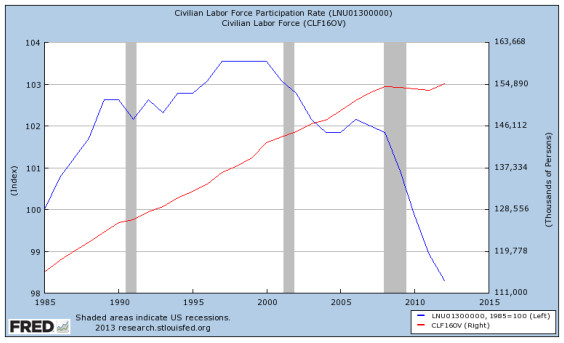

We had a run of Fed regional presidents speak recently and it's no surprise that the last two sets of minutes implied a healthy divide. For the voting members, the hawks are mostly Esther George of Kansas who is worried about rising farm land, bond prices and high yield loans. She barely mentions unemployment. Janet Yellen, the Vice Chair, and one to watch for if Bernanke decides to step down next year, is all about employment growth and low participation…here you can see the 2000 peak and quick decline:

Source: Federal Reserve Bank of St. Louis, Economic Research

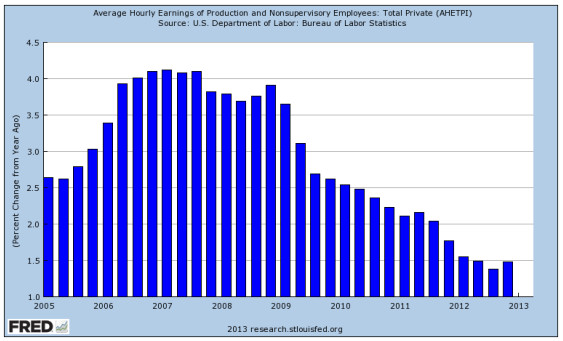

As well as the growth in earnings which has pushed along at levels way below inflation, see here:

Source: Federal Reserve Bank of St. Louis, Economic Research

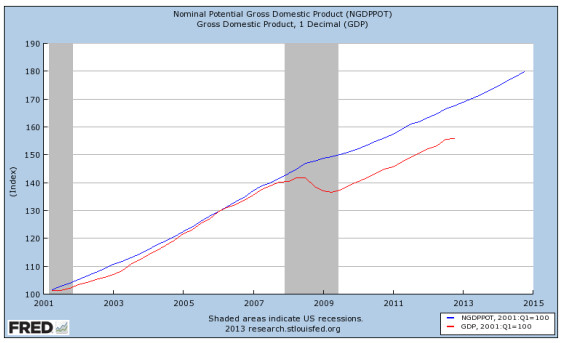

And finally the imprecise but still relevant output gap which can't seem to trend up to its potential, see here:

Source: Federal Reserve Bank of St. Louis, Economic Research

Ever read IKEA instructions? They start in Swedish, translate to Chinese and then to English. With English not being anyone's first language. Fed minutes have about the same level of readability. There's always some rune reading going on when interpreting Fed minutes, especially when it comes to defining "few…some…many." We don't think it matters too much because Bernanke is firmly in charge and probably has all the permanent members with him. The dissenters can use speeches to make different points but rarely carry the day for policy changes. There's no uncertainty about the zero rate. That stays until they reach the 2.5/6.5 (rates for inflation and unemployment) threshold.

What is less certain is how long they maintain the $85bn asset purchase program and if they vary the mix and rate. That seems entirely appropriate because we would concede that the Fed balance sheet is getting a little weird: $3.2 trillion, of which $1.7tr is in government debt, which is about 15% of all public debt, and of that, $1.3tr in maturities over five years or about 26% of the total. Some members express concern and may want to "vary" or "taper" the pace of purchases as economic conditions change.

What might those be? Well, Bullard of the St. Louis Fed, gave some indications when he said they would look at total employment, hours worked,JOLTSdata and, we would guess, participation, inflation expectations and asset prices. This means to us that if the economy is good, they will pull back on asset purchases. But we're not there yet. Also buried in the minutes was a clue about the unwind. Again, several members said they would want to hold the securities for a "longer period." Our guess is that means until maturity. So on balance we had not great economic reports, added to a commitment to hold the current assets plus a possible change in buying if things get better. That seems a good enough mix even if the communication is a little opaque. The market initially fell a quarter point but rallied back by half a point over the next day which seems the right response.

Europe

The broad story remains that financial markets, spreads and banking are in a stable to mend phase but the real economy is in a bind. So Spanish spreads against Bunds have narrowed from 626bp last summer to 360bps, Italy from 520bp to 292bp and even Greece from 2900bps to 950bps. But the GDP figures for Q4 came in at -0.6% and most positive numbers, like better budget deficits, lower inflation, improved current accounts, are just as indicative of weakness as strength. Europe is thus working from a very low base and will take a while to return to positive rates of expansion.

There are a few options and questions: i) will Germany use some of its borrowing room to set up some expansion ahead of the November elections (maybe) ii) will theECBgive more guidance on monetary policy (probably) or iii) adopt programs for banks to lend (probably not) and iv) in light of recent euro strength, will they try to talk or intervene the currency down (just talking it down from €1.36 to €1.31 has been quite an achievement, so yes )? We think on the whole, Europe will have a slow mend and buying into equities is about buying into global growth and some exports.

US

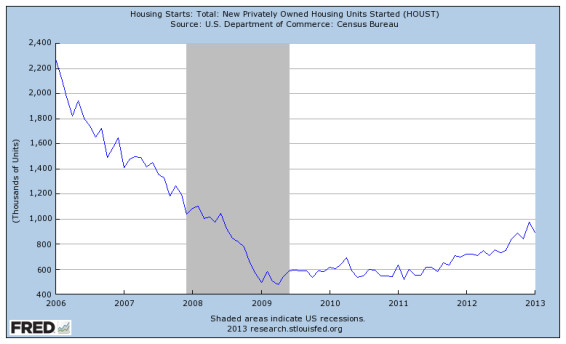

Highlights of the week were a slight drop in housing starts but a revision up to the prior two months. Housing starts are 24% above those of a year ago, but as the following graph shows that's quite a way off the peak.

Source: Federal Reserve Bank of St. Louis, Economic Research

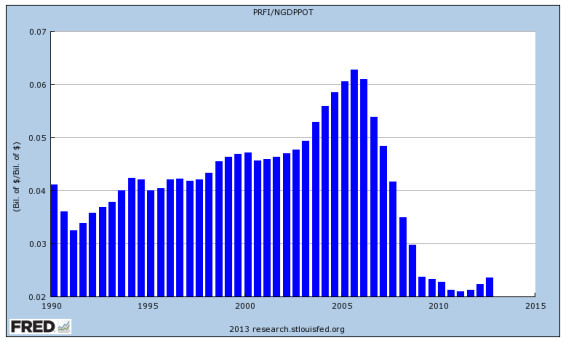

Housing is more of a wealth effect and consumer boost story. If people feel confident about jobs, they're willing to form households and follow through with all the expenditures. Housing by itself is not a big driver of growth. Here's private residential fixed investment as percent of nominal GDP. It's a big drop from the peaks and likely to stay that way.

Source: Federal Reserve Bank of St. Louis, Economic Research

We saw the same upward revision story in industrial production with the three month on three month increase now at 1.9% and the new orders index from theISMand Empire Survey showing some solid increases. Inflation at the producer and consumer levels came in soft and below expectations. The core, ex-food and energy, had a slight rise but that was after two months of very slow growth. No inflation here.

Bonds

We don't see a lot of opportunity at these rates levels. The return spread of the S&P over the broad bond aggregates YTD is now about 5.82%. It was as high as 8.33%. The closer it moves to 5%, the more we're ready to take our cash holdings down and start buying more into equities.

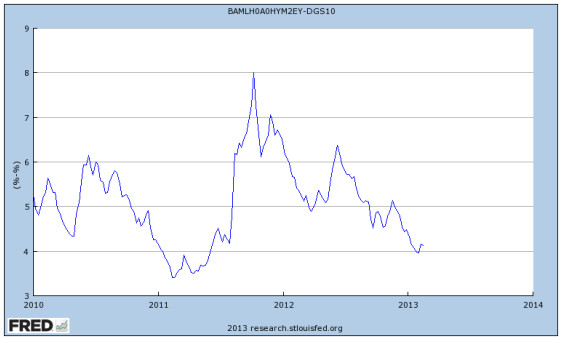

The high yield spreads came in fast in the last half of 2012. Here's the yield less the yield on the 10-year note.

Source: Federal Reserve Bank of St. Louis, Economic Research

While there's still a healthy bid on new issues, we have seen some softening in the after markets. The opportunity in bonds is about "stories" meaning idiosyncratic risks of management, products, cover and margins. That's why we're buying away from the indices when we can.

Equities

Equities have had a strong run and especially small company stocks. Here's the ratio small company performance to the S&P. Every time the line slopes up, small cap outperforms:

Source: Federal Reserve Bank of St. Louis, Economic Research

Hopefully some of the new money hype is rolling over. A "weight of money" argument for stocks is one of the flimsiest reasons for a market rise and rarely has legs to it. It's up there with "there are more buyers than sellers." We thought the market needed a reason to sell off a bit and the FOMC minutes were the catalyst. Earnings growth this year may come in at around 10% but real operating earnings before share buy backs distort the story and will be about half that. And the real, not per share earnings, are what counts for GDP. For now, though, the risk assets have strong sentiment behind them.

Bottom Line: Increasing the equity exposure on any correction.

[1] Standard & Poor's 500 Index is an unmanaged index of 500 widely held US equity securities chosen for market size, liquidity, and industry group representation. An investment cannot be made directly in an index.

Sources: "Employment and Social Developments in Europe 2012", EC Publications; Contours of the World Economy 1-2030, Angus Maddison; Jonathan Portes, www.notthetreasuryview.blogspot.com; "Booms and Systemic Banking Crises", Frederic Boissay, Fabrice Collard, and Frank Smets; Frances Coppola Comment; Bloomberg; Capital Economics; CRT Ader; Economist Free Exchange; Federal Reserve Bank of St. Louis; IMF Fiscal Monitor; Federal Reserve Bank of Kansas; Federal Reserve Bank of New York; Federal Reserve Bank of Philadelphia; Federal Reserve Board; Bureau of Labor Statistics; Bureau of Economic Analysis; US Department of Commerce; US Census Bureau; US Dept of Housing & Urban Development; ISI; J.P. Morgan Market Intelligence; TrendMacro; University of Michigan; High Frequency Economics; Pantheon MacroEconomic Advisors; Sentinel Asset Management. Inc.

© Sentinel Investments