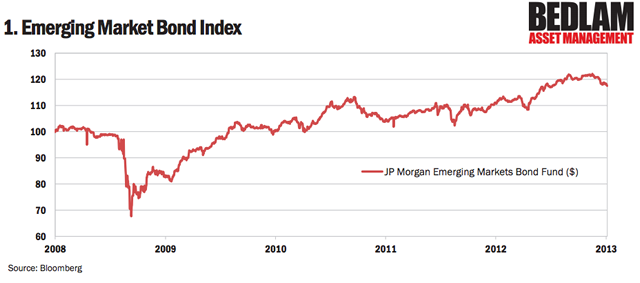

Although the year is barely a month old there are already signs that the long-awaited rotation out of the perceived safety of bonds and into inflation-proofed equities may have begun. Given the dismally low yields on offer it seems likely that, at the very least, it is the beginning of the end of the bond market bubble. Some of the biggest bubbles in the bond market, and thus most at risk from a sell-off, are in high yield and emerging market debt. In the search for yield there has been an explosion in money allocated to emerging market debt, pushing bond yields down to record lows, often ignoring weakening fundamentals. Taking as a proxy the JP Morgan Emerging Market Bond Fund (which looks to track the index), emerging market bonds have lost -2.1% in dollar terms so far this year (see chart 1). Over the same, admittedly short, period emerging market equities have fallen - 1.2% in dollar terms, compared with a gain of 6.4% in the S&P 500, 2.5% in the Nikkei and 1.1% for European equities. A continued underperformance of emerging market equities versus developed markets may well be one of the many surprises this year, as the bond market discovers that their financial strength is not quite as healthy as first thought. This would also have negative implications for commodities.

The scale of the inflow into emerging market debt in recent years has been colossal. Russell Napier, strategist at CLSA Ltd, estimates that emerging market bond funds have grown from $34b in 2003, to currently over $300b. Historically, foreigners have focused their investments in the dollar denominated debt of developing countries, due to the fear of economic indiscipline and inflation. Not so now. The Financial Times recently reported that from less than $150b in March 2009, foreign holdings of local currency emerging market debt reached over $500b by the end of last year. Despite these large capital inflows the growth in the foreign reserves of emerging markets has fallen, from 20% two years ago to currently zero. The implication is that their balance of payments position (current account plus capital account) is fast deteriorating. If a country targets its exchange rate to maintain export competitiveness and their balance of payments moves into deficit, then they will have to sell their foreign reserves to buy and support their currency.

China is a classic example of how a combination of smaller trade surpluses, capital outflow and a targeted exchange rate can lead to stagnant foreign reserves. At the end of June 2011 China’s foreign reserves totalled $3.3 trillion, a rise of 27% against the previous year. This growth has collapsed to zero, with foreign reserves virtually unchanged at $3.3 trillion as at the end of last year. These large inflows of hot money from bond investors are now being fully offset by dwindling current account surpluses (as they import more and export less) and capital outflow. Across the developing world many of the previously large current account surpluses have now shrunk or gone into deficit, as cheap and easy access to credit has fuelled consumption and a surge in imports. Meanwhile a rise in domestic asset prices has resulted in capital outflow, as local money seeks more attractive overseas investment opportunities. There could easily be a sharp exodus from these open-ended bond funds as they wake up to high valuations and deteriorating fundamentals. Exacerbated by the illiquid nature of emerging market debt, this would lead to both a jump in interest rates and a declining currency.

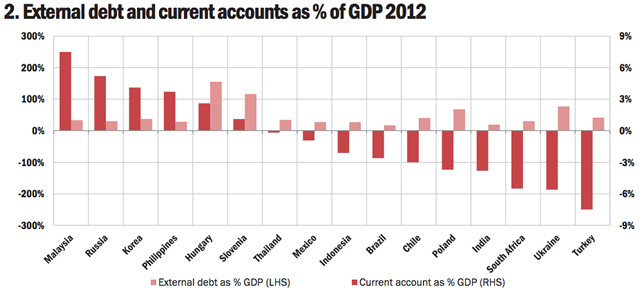

The biggest risk lies with those countries that have a high foreign debt-to-GDP ratio and a large current account deficit. This is a potentially toxic combination if the current account deficit has been reliant on hot money, such as bond investors, for funding. If these investors decide to sell, weakening the currency, then the country’s foreign debt becomes more expensive to service. Historically external debt-to-GDP levels above 35% have led to a significant rise in a country’s credit risk.

In this respect some of the biggest risks exist in Eastern European countries such as Hungary, Croatia, Ukraine and Poland, with external debt to GDP of 155%, 97%, 77% and 68% (see chart 2). Turkey also has major structural problems. External debt to GDP is 41% and the current account deficit, at 7.5% of GDP, is heavily reliant on hot money. Despite this, the Turkish 10- year domestic government bond yield trades at 6.6%, down from 10% in 2010. Meanwhile a potential funding pressure looms. Turkish companies have $130b of corporate debt to roll-over in 2013, out-stripping Turkey’s $100b in foreign reserves. Oblivious to Turkey’s worsening financial situation the equity market trades on a cyclically adjusted PE of 17x.

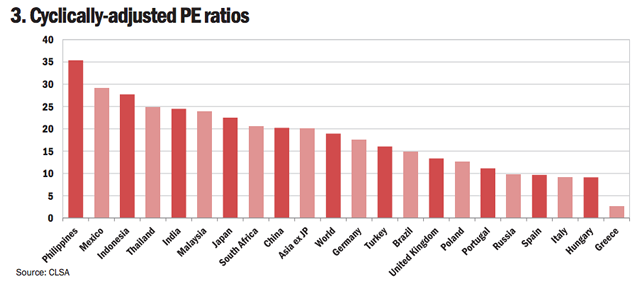

Equity investors are also at risk from excessively high valuations that have been boosted by unsustainably low interest rates. Historically, the best equity returns have been made from buying cheap, well managed businesses that offer a decent dividend yield. Investors now need to be much more selective. Some of the high PE ratings now on offer provide little room for earnings disappointment, with the most extreme being Mexico, Chile and much of South East Asia (see chart 3). Mexico is now trading on a price-to-earnings ratio of 28x, with the Philippines, Indonesia and Thailand on 36x, 27x and 25x respectively. The lofty Indonesian equity valuations come at a time when their current account deficit widened to 3.6% of GDP in the fourth quarter of 2012. It is becoming increasingly reliant on short term inflows. The most recent data shows that over 40% of the deficit was funded by short term money such as bond investors.

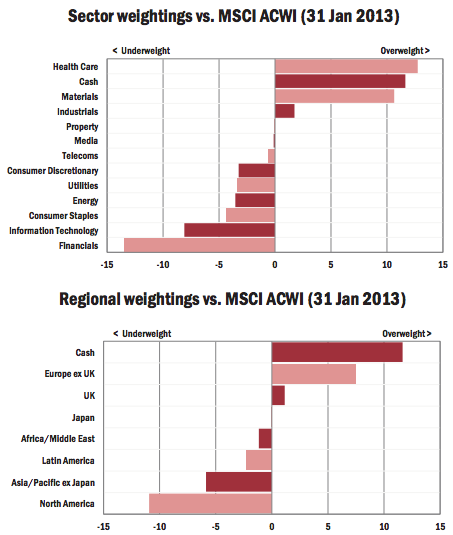

Fortunately emerging markets is a deep enough asset class to still provide ample investment opportunities. The Global strategy’s 13% weighting to emerging markets is focussed in Singapore and North Asia. It consists of a handful of cheap, well run companies that are increasing market share and have structural factors that will drive an expansion in operating margins over the next 2-3 years. The fund is also finding cheap exposure to emerging markets through companies listed in developed markets. Thus based on where companies generate their profits the fund is 35% exposed to emerging markets.

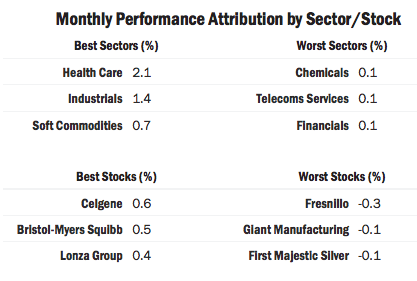

Gains for the fund were marginally ahead of the index, boosted both by the continued rally in equities and stock selection. In the fund, health care, the biggest sector at 18%, performed best on the back of strong news flow. The industrial and agricultural holdings also did well as money moved out of sectors viewed as “safe” bond proxies, such as utilities and staples, into cheaper and more cyclical companies. Lonza (chemicals) and Mosaic (fertilisers) jumped 9% and 8% respectively. Two other notable trends, which are likely to continue, were the underperformance of emerging market equities versus developed markets and the rally in Japanese equities. By listing, the fund’s weighting to emerging markets is 13%, compared with the 18% recommended by the index. The 10% in Japan is virtually all in non-bank financials and property.

The share price of Celgene popped 26% as management announced a revenue target of $12-13b for 2017, from $6b in 2013 . This was based on an upbeat assessment of future approvals across its pipeline of cancer and arthritis drugs. Medtronic, which produces medical devices, gained over 13% after management predicted better long term sales growth. Amongst the pharmaceuticals, Bristol Myers and Pfizer had strong gains. Both companies released good 2012 numbers and will benefit from the approval of their jointly developed stroke prevention drug, Eliquis. Elsewhere the industrial holdings rallied, on expectations that global growth will accelerate rather than on any company specific news flow. Holdings in the materials sector were also firm. Lonza (a supplier to the pharmaceutical companies) rallied in anticipation of good 2012 results, while the agricultural chemical companies, Yara and Israel Chemical, rose in line with higher fertilizer prices.

One of the few detractors from performance was bicycle producer Giant Manufacturing. The stock lost over 5% as year-end sales fell short of expectations; the fourth quarter is seasonally weak for the group. In the future, earnings growth should accelerate as production facilities in China are now fully on stream and will ramp up.

There were two sales and two new purchases. The Cambodian casino operator, Nagacorp, jumped 16%, resulting in a 60% gain since purchase; the stock was sold at target price. Australian Agricultural was sold as extreme weather is a threat to their livestock and investment plans look unrealistic. Sumitomo Real Estate was purchased for its exposure to the improving Tokyo condominium market. December condominium viewings are the highest for several years, with the government looking to extend mortgage interest relief. Mitsubishi Estate, the fund’s other property holding, mainly deals with the Tokyo office market. A sector review of precious metal miners resulted in the purchase of First Majestic. It is a low cost silver producer ($9/oz versus silver price of $31) with all of its assets located in mining-friendly Mexico. We expect production to more than double over the next three years.

© Bedlam Asset Management