Say you are evaluating the markets of two countries in a search for investment growth opportunities. One country’s sovereign debt is 120% of its gross domestic product (GDP), while the other has outstanding sovereign debt that represents only 11% of its GDP.

Saddled with sovereign debt, the first country faces painful fiscal austerity measures, inflationary ones, or both—any of which will no doubt stifle economic growth.

Meanwhile the second nation, with a relatively healthy debt level compared to its GDP, is poised for growth. And in case of another global economic downturn, its fiscal strength could lend this economy a lot more flexibility. After all, governments have greater ability to cut taxes or inject stimulus spending when they begin from healthy debt and spending levels.

Which country represents a more compelling investment option? The choice seems clear. The crippling effects of runaway debt are on display in some of the mightiest countries of the world. These past few years have demonstrated to investors that a strong fiscal position is of paramount importance to a country’s economic vibrancy.

Consider, then, that the figures noted above actually represent the economies of Italy, which carries a crushing sovereign debt load equal to 120% of its GDP, and Kazakhstan, with a modest debt-to-GDP ratio of 11%.1

A Common Misconception

Frontier markets such as Kazakhstan offer the growth opportunities that investors are eagerly seeking in today’s markets. The combined GDP of frontier markets is expected to grow by 4.1% annually over the next three years, well in excess of the 2.5% annual GDP growth rate forecast for the U.S., not to mention the 1.2% rate predicted for Germany and Japan.2

Yet even though the upside potential of frontier markets is clear, many would-be investors are put off by the aura of risk associated with these exotic-sounding and relatively unfamiliar nations. Given the fiscal woes facing so much of the developed world, it would be easy to assume that frontier markets like Kazakhstan are on shaky financial ground too. But it would also be wrong. In fact, while most countries in the developed world are running vast deficits relative to their market economies, the frontier markets stand in stark contrast. Places like Qatar and Nigeria, for example, boast solid fiscal positions that can help offset the other risks their markets might present.

There are, no doubt, many ways in which frontier markets are riskier than developed ones. Political instability, bureaucratic risk, lower levels of infrastructure and the potential for corruption are all legitimate reasons for concern, even though the growth potential in frontier markets is clear.

That is why we believe a broadly diversified approach to investing is crucial when it comes to frontier markets. As an asset class, frontier markets are distinguished not only by low correlations with other major equity asset classes,3 but also by how different these nations are from one another. Other than sharing some basic characteristics and being grouped together by indexers, frontier markets have little in common. They are so diverse that a major development in one frontier economy—say, Nigeria or Argentina— may make no ripple in others, like Estonia or Vietnam. The upshot is that investing across a broad cross section of frontier markets can potentially help dampen the risks of investing in these less developed, less familiar nations.

But based on our analysis, and relative to their counterparts in the developed world, we believe the fiscal positions of frontier market economies are not a worry. In fact, in many cases they can be viewed as a source of strength.

An Advantage Over Developed Nations

Most of the major developed market economies are running large deficits relative to their output, and their levels of debt to GDP have increased rapidly. The last two years have been a fiasco for many European economies, their sovereign debt issues wreaking havoc on global equity markets. Ireland, Portugal, Greece, Italy and Spain are in various stages of economic disarray, and Japan’s debt is now more than 200% the total size of its GDP.4 Even the United States, long seen as the “risk-free” asset, has lost its AAA credit rating from Standard & Poor’s.5

Investors are all too familiar with the fallout. These fiscal pressures have driven the developed economies of the world into a corner from which they have two basic escape options. They will either need to reduce spending and increase revenues, leading to a drag on economic growth, or they will have to inflate their way out, utilizing their central banks to hold interest rates at levels below that of inflation. Both options would have a negative impact on their abilities to grow.

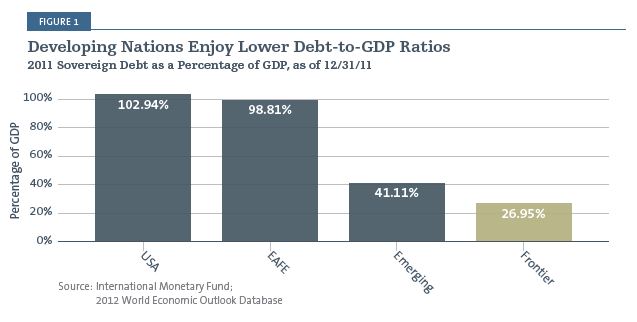

In stark contrast, developing economies that lived through a number of defaults and bailouts in the 1990s have generally run prudent fiscal policies over the last decade, including the worst years of the financial crisis in 2008 and 2009. This may be one of the reasons these economies were able to rebound from the crisis so successfully. Developing nations’ sovereign debt levels are presently far lower than those of developed nations (Figure 1). In fact, many—including Turkey, Kuwait and Estonia—have actually experienced credit upgrades over the last few years.6

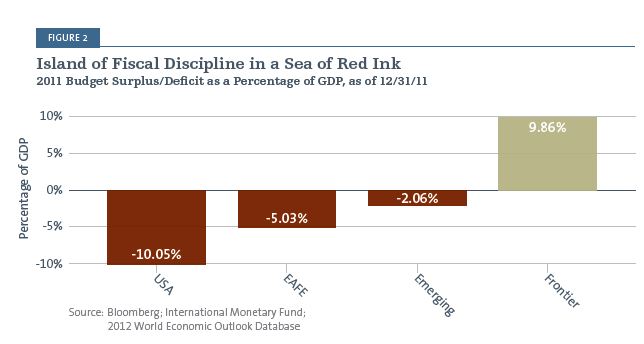

An easy way to get the full picture is by comparing the total national budgets of countries in the frontier, emerging markets and EAFE indexes, along with the U.S., relative to their respective GDPs. Based on 2011 figures, only the frontier countries boast a positive budget surplus as a percentage of their combined GDP, topping the chart at +9.86%. Meanwhile, as a group the developed nations are running substantial budget deficits relative to GDP, with the U.S. carrying a debt load equivalent to more than

10% of its GDP (Figure 2).

Developing countries, including both emerging and frontier markets, can use their healthy fiscal positions as a platform for continued economic growth. All forecasts point to multiple drivers of that future growth—including technological, demographic and economic trends—which may place frontier economies in a position of strength.

In contrast to the developed nations, whose populations are aging, most frontier countries have a younger demographic that points to increasing economic productivity and growth in the years ahead. World Bank data indicates that on average, the median-age in the economies of the Group of Seven, or G-7, is almost 41. In BRIC nations, Brazil, Russia, India and China, the median age is 32. But the median age in frontier market nations is just under 27 years old. And frontier population growth, at a current average of 1.30% annually, is double the 0.65% population growth rate among the BRICs. The G-7 populations are expanding even more slowly, at 0.51%, according to the World Bank database.7

As emerging market nations expand their trading positions around the globe, countries including China, India and Brazil are fueling the growth of frontier countries by expanding trade relationships and entering into strong, symbiotic economic partnerships with them.

The growth potential of frontier markets is easy to understand. They are the emerging markets of tomorrow. But the often heard myth is that they are exceptionally risky. That assumption is understandable. It’s true that political instability, bureaucratic red tape, corruption and less developed infrastructure are all potential hurdles to success in frontier markets. But their fiscal positions? In my opinion, that’s not a worry at all.

You should consider the investment objectives, risks, charges and expenses of the Forward Funds carefully before investing. A prospectus with this and other information may be obtained by calling (800) 999-6809 or by downloading one from www.forwardinvesting.com. It should be read carefully before investing.

RISKS

There are risks involved with investing, including loss of principal. Past performance does not guarantee future results, share prices will fluctuate, and you may have a gain or loss when you redeem shares.

Alternative strategies typically are subject to increased risk and loss of principal. Consequently, investments such as mutual funds which focus on alternative strategies are not suitable for all investors.

Diversification does not assure profit or protect against risk. Derivative instruments involve risks different from those associated with investing directly in securities and may cause, among other things, increased volatility and transaction costs or a fund to lose more than the amount invested.

Foreign securities, especially emerging or frontier markets, will involve additional risks including exchange rate fluctuations, social and political instability, less liquidity, greater volatility and less regulation.

Investing in a non-diversified fund involves the risk of greater price fluctuation than a more diversified portfolio.

Paul Herber is a registered representative of ALPS Distributors, Inc. *Paul Herber has earned the right to use the Chartered Financial Analyst designation. CFA Institute marks are trademarks owned by the CFA Institute.

Forward Funds are distributed by Forward Securities, LLC.

Not FDIC Insured | No Bank Guarantee | May Lose Value

1.International Monetary Fund, 2012 World Economic Outlook Database, as of 12/31/11

2. Ibid.

3. For example, according to Bloomberg as of 11/27/12, the MSCI Frontier Markets Index showed a .352 correlation with the S&P 500 Total Return Index and a .506 correlation with the MSCI EAFE Index.

4. International Monetary Fund, 2012 World Economic Outlook Database, as of 12/31/11

5. Standard & Poor’s, as of 12/31/11

6. Ibid.

7. World Bank database, as of 12/31/11

Definition of terms

AAA is the highest possible rating assigned by the credit rating agency Standard and Poor’s when measuring the credit worthiness of individuals, corporations and countries. It is based upon the history of borrowing and repayment, as well as the availability of assets and extent of liabilities. Austerity measures refer to measures taken by governments to decrease spending in an attempt to reduce budget deficits.

BRIC is an acronym for the emerging economies of Brazil, Russia, India and China combined. Correlation refers to the statistical measure of how two securities move in relation to each other and is computed as the correlation coefficient, with ranges from -1 to +1.

Debt-to-GDP ratio is a measure of a country’s federal debt in relation to its gross domestic product (GDP). By comparing what a country owes to what it produces, the debt-to-GDP ratio indicates the country’s ability to pay back its debt.

Group of Seven (G-7) are seven of the world’s largest developed countries that meet periodically to achieve a cooperative effort on international economic and monetary issues. The member countries are: Canada, France, Germany, Italy, Japan, United Kingdom and United States.

Gross domestic product (GDP) is the total market value of all final goods and services produced in a country in a given year, equal to total consumer, investment and government spending, plus the value of exports, minus the value of imports. The GDP of a country is one of the ways of measuring the size of its economy.

Inflation refers to the rate at which the general level of prices for goods and services is rising, and, subsequently, purchasing power is falling.

Sovereign debt is the total amount owed to the holders of sovereign bonds or bonds issued by a national government.

© 2012 Forward Management, LLC. All rights reserved.

FWD004382

123113