Central Banks Are Factoring Financial Stability into Their Decision Making

- Central banks are factoring financial stability into their decision making

- The FOMC is taking a critical look at its asset purchase strategy

- Don’t look now, but the sequester is coming

Central banks around the world have a variety of mandates. Most are required to maintain some mix of price stability and solid levels of growth or employment. These are no small feats, and it is often a struggle to balance objectives. This was evident in the most recent Monetary Policy Council meeting at the Bank of England, where Governor Mervyn King was on the short side of a 6-3 vote against quantitative easing.

To make matters even more difficult, a relatively new objective is becoming more prominent for international monetary authorities. Whether formally stated or informally pursued, the quest for financial stability is having an increasing bearing on central bank strategy. And it is complicating the conduct and communication of monetary policy.

In the immediate wake of the 2008 financial crisis, few would dispute that financial stability was a worthy aim. The reversion of asset price excesses in global markets severely damaged the balance sheets of many individuals and financial institutions, creating a deep global recession. More than four years later, economies around the world are still struggling mightily to regain normalcy.

In the US, the Federal Reserve has received criticism from some corners for creating conditions that contributed to the crisis. Short-term interest rates were held very low for a very long time early in the last decade, which facilitated a buildup of leverage that proved unsustainable.

Believing that financial markets were reasonably contained and self-regulating, the Fed and other supervisors took a less-than-active role in policing them. When the fall came, it became apparent the feedback loop between asset prices, banks, and the economy had been underestimated. The memory of these miscalculations is still fresh, and central banks are loathe to repeat past errors.

Post mortems on the crisis identified the need for systemic regulation. To that end, the Dodd- Frank Act created a Financial Stability Oversight Council with representatives from all regulators. The Federal Reserve was given additional authority for “macroprudential” oversight. The reunification of the UK Financial Service Authority (FSA) and the Bank of England was announced in 2010, and financial stability was made an official element of their collective charter. Groups within central banks began monitoring markets more closely for signs of excess and sought to better map interconnectedness in the financial system.

At first, there was little excess to be found. The risk aversion that set in after the crisis caused asset prices to correct sharply, removing the air from the bubbles that had formed. But the extreme conservatism was not helpful to economic prospects. And so among the stated goals of quantitative easing was to bring interest rates and uncertainty down to a point where investors would rebalance their holdings in a somewhat more aggressive direction. It has been hoped that a modest renewal of risk appetite would better promote economic expansion.

In this regard, central bank action has been a great success. Market volatility is at a low level, and risk assets have performed very, very well.

Yet the difficulty of this strategy is that it is impossible to steer risk appetite precisely. Markets are often characterized by bullish and bearish swings, driven more by animal spirits than cold calculus. The more aggressively a central bank pursues quantitative easing, the greater the risk that investors could become overly aggressive as well. And when the easing program inevitably stops, there is potential for a disorderly reversal.

In this sense, the objectives of promoting growth and sustaining financial stability could run counter to one another. We see this reflected in heightened discussion of policy risks in central bank deliberations and public comments. A critique of the most recent Federal Reserve debate on this front follows this segment.

The introduction of financial stability as an additional mandate for central banks will be difficult to factor into monetary policy. There are no clear measures of stability that could be used in the same manner as inflation or unemployment targets. Cliché though it sounds, markets are stable…until they aren’t. It’s terribly difficult to know whether actions today are laying the groundwork for dysfunction that could occur many years in the future.

And while central banks have signaled an increased willingness to address nascent asset price excesses with supervisory restraint, history does not suggest that they will be very successful. Warnings about extremes in the mortgage markets during the last decade were routinely muffled by industry participants and their adherents in Congress.

So the job of central banks and those who follow them has a new dimension that complicates things. While it’s worthy to consider the potential impact on financial stability, it’s terribly hard to balance this element against the more tangible and immediate goals of price stability and full employment. There is simply no map for the terrain that we are now traversing.

Latest from the FOMC: Evolution of Asset Purchase Strategy

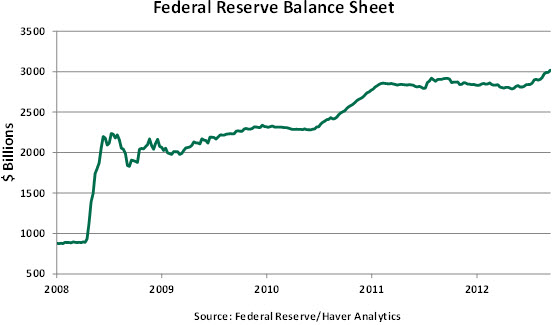

The minutes of the January 29-30 Federal Open Market Committee (FOMC) meeting revealed a range of opinions regarding quantitative easing. The existence of different views about suitable monetary policy actions should not be surprising, given the extended lackluster recovery of the economy and the size of the Fed’s balance sheet. The Fed’s balance sheet stands at more than $3 trillion with the potential to touch $4 trillion if the current asset purchase plan proceeds without reductions.

The minutes of the January meeting noted that “ several ” participants held the view that the size of monthly purchases ($85 billion) should be varied depending on the economic outlook or the Fed’s assessment of the costs and benefits of asset purchases. These observations suggest that the FOMC is trying to fine-tune its purchase program to be consistent with economic developments and net costs of its action.

The discussion also contained a modification of the current understanding of forward guidance pertaining to asset purchases. A “ number ” of participants indicated that the ongoing assessment of costs and benefits of the large asset purchase program could lead to a tapering in the size of asset purchases or a termination before a “substantial” improvement in the labor market had occurred. Financial markets interpreted this modification about the timing and size of asset purchases as the Fed leaning slightly to the hawkish side.

The doves on the FOMC noted that a premature termination of financial accommodation could disrupt economic growth. (This has been cited by some as a policy error in Japan.) They stressed the importance of maintaining an accommodative stance and retaining assets on the Fed’s balance sheet even as the economy strengthens to ensure sustained expansion.

Fed Governor Jeremy Stein voted with the majority at the January meeting,but in a speech earlier this monthhe expressed concern about whether policy was causing excesses to develop in financial markets. The minutes reveal that a discussion along the lines of Governor Stein’s recent speech was part of the January meeting. The Fed’s staff was asked to perform additional research on these aspects for discussion at the March 19-20 FOMC meeting. This session will be followed by a press conference, which should make for very interesting viewing.

Summing up, the Fed offered more color on its current thinking about the asset purchase program but there is no reason to infer that a change of pace is coming anytime very soon. The FOMC has not altered its current view of the economy, and employment conditions are still a long way from ideal. But the notion that quantitative easing might continue without bounds is being challenged, and a tapering of the program before the end of this year cannot be ruled out.

Automatic Federal Government Spending Cuts – A Preview

Markets are closely watching the March 1 deadline when the federal government spending cuts of $85 billion in fiscal year 2013 will take effect as per the Budget Control Act. This impending event is often referred to as the “sequester,” and it is the first installment of a $1.2 trillion reduction in government spending to be put in place over a period of nine years. With time for compromise running short, analysts are busy anticipating how the sequester will affect the economy.

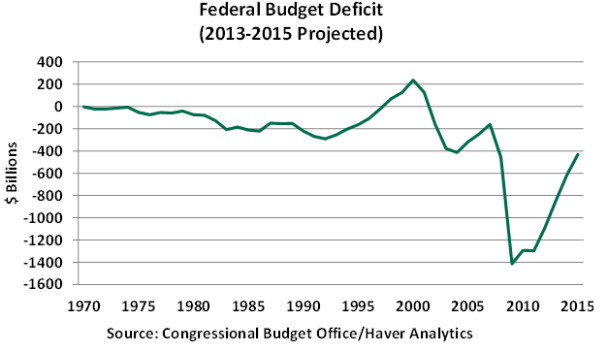

Some have hailed the sequester as a credible budget reduction program. And that it is; assuming the entire gamut of spending cuts occurs, the Congressional Budget Office (CBO) estimates that the federal deficit would shrink to $845 billion and $616 billion in fiscal years 2013 and 2014, respectively, from $1.09 trillion in 2012. If these estimates are accurate, the economic ramifications are largely positive. Pressure on interest rates will be reduced as the federal government’s participation in credit markets declines.

Yet a decline in federal government spending directly reduces real growth and potential offsets follow with a lag. There is no firm consensus about the size of fiscal multipliers, which drive the size of economic gains that ensue when government reduces its involvement in the economy. Assuming a fiscal spending multiplier at the mid-point of the CBO’s stated range, our current estimate of real GDP growth will be reduced 0.5% on a Q4/Q4 basis in 2013 if all provisions of the sequester take effect.

Drilling down to the details of the likely cuts in government spending reveals the micro aspects. A 50% reduction in discretionary defense outlays is baked into the provisions of current law, implying that defense operations will suffer a sizable setback. Reduced funding for schools would translate to fewer teachers and cutbacks in a wide range of programs. Federal government expenditures related to food inspection, air traffic control, and law enforcement would be pared back. Cuts to border and port security could affect the volume and timing of trade flows. So we are all likely in for some level of inconvenience.

Social Security and Medicare programs are not subject to a change, while there will be a 2.0% reduction in payment to Medicare providers. Essentially, nearly all federal agencies must scale back outlays of the next seven months of fiscal year 2013.

On the political front, discussions are underway indicating that Congress could modify existing law. Currently, Congress has adjourned for a recess and has a very short period to bring about alterations to current law before March 1. Therefore, the odds are high as of this writing that the automatic federal government spending cuts will take place on March 1.

In addition to the sequester, Congress faces a series of other deadlines in the next few weeks. The current Continuing Resolution enabling funding operations of the Federal government expires on March 27. Failure to renew this authority could result in a temporary shutdown of the federal government. Yet as Congress begins deliberations on the details of a new Continuing Resolution, there is room to soften the blow of the sequester.

Congress must pass the Federal budget for the next fiscal year by April 15 to prevent a delay of their paychecks. Lawmakers also struck a deal earlier in the year that temporarily suspended the statutory debt ceiling until May 18.

Effectively, Congress has to contend with four deadlines between now and mid-May, and the uncertainty surrounding them will not help economic performance. One can only hope that the second half of the year will be free of budget hoopla, with only economic fundamentals driving market movements.

The opinions expressed herein are those of the author and do not necessarily represent the views of The Northern Trust Company. The Northern Trust Company does not warrant the accuracy or completeness of information contained herein, such information is subject to change and is not intended to influence your investment decisions.

© Northern Trust