Trying And Failing To Make The Math Work For Long-Term Bonds

- For the past 31 1/2 years, owners of 10-year U.S. Treasury bonds have earned “real” total returns of 6.7%—on par with the long-term real return to equities.

It’s little wonder that some managers are now seeking to “lever up” such low volatility return streams. Such a strategy certainly appears backward-looking, however.

- Long before government bonds matched real stock returns, they suffered a 55-year period that offered investors a real return of zero. This, in all likelihood, will be close to the real return government bond owners will earn over the next decade (if not longer).

- The short-term implications of higher U.S. Treasury rates on asset allocation decisions. We look at the 30-day correlations of a variety of asset classes to 7-10 Year U.S. Treasury returns.

Having turned prematurely bearish during the tech bubble of the late 1990s, we vowed to “play” the next bubble in a savvier manner. In fact, the experience motivated us to build upon our existing disciplines in ways that might help us capture a bigger piece of the next “unjustified” market move, while not entirely abandoning fundamental underpinnings.

So how did that work for us?

In the case of industrial metals stocks, it worked wonderfully. But in the case of the 30-plus year bull market in bonds, not so much.U.S. government bonds, we thought, were no bargain by the middle of the 2000s. But it turned out the fun was far from over…the market and economic collapse of 2007-2009 resulted in a sort of “depression bid” under the Treasury bond market that has yet to evaporate—even with the U.S. economic recovery approaching four years in length.

- We recognize today’s fixed income allure extends beyond the fears of another 2008. Government bonds have been the only asset class to offer protection during the stock market’s several (temporary) setbacks following the great 2009 low. Bonds might well offer the same protection in the next correction, but Treasury yields have drifted so low that the long-term risks now (in our opinion) outweigh the short-term (and largely “statistical”) rewards of a heavy bond position.

- Bearish bond commentary usually centers on the long-term inflationary risks of Fed money printing, euphemistically known as QE. We share these fears, but find the task of timing such “monetary debasement” inflation nearly impossible (as if forecasting any other form of inflation was easy). But we envision a very sobering scenario for bond investors with no forecast of inflation whatsoever: “initial conditions” (i.e., current low yield levels) heavily favor the bond bears over the next decade. Count us among them.

The Two Sides Of Bond Market History

Few investment shops have a greater affinity for complex mathematics like the “average” and “median” than us. That being said, there are certain arenas in which the average outcome has almost never occurred. The bond market is one of them, and possibly a reason why our interest rate calls in recent years have been less than prescient.

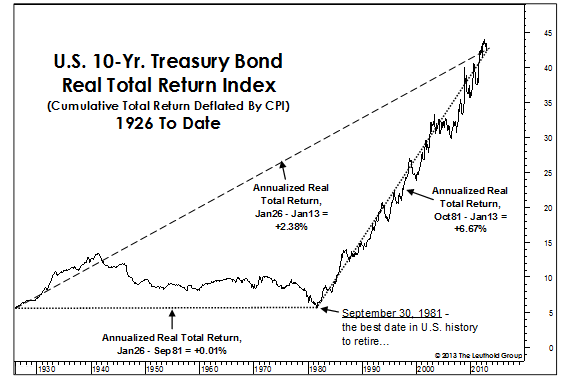

Bond managers with a sense of history will tell you the 10-year U.S. Treasury bond has delivered a long-term average total return of about 2.5% above CPI inflation. Disingenuous ones might be tempted to inflate that real return figure, simply by shortening the period of history under consideration. But the diagram below shows the modern history of Treasury bonds is a dichotomous one in which no single summary statistic is helpful.

- Intermediate and long-term Treasury bonds amounted to nothing more than certificates of confiscation for the first 55 years of the “Ibbotson history”—i.e., 1926 to 1981. The U.S. 10-Year Treasury delivered a real total return of one basis point per year over that period. (Can you name a single bond trading guru from that period? I didn’t think so!)

- The second span on the chart (September 1981-to-date) is certainly more popular among bond managers (not to mention purveyors of Liability Driven Investing (LDI) and “risk parity” strategies). Over the past 31 1/2 years, the plain vanilla 10-year Treasury has delivered a real total return of +6.7% —equal to the long-term real total return to stocks!

- While the short-term is cloudy, long-term bond market math is easy. Today’s yield is about 2%. The financial engineering types who have cleverly (and belatedly) decided to “lever up” recent real returns can only hope to repeat them in an environment of significant (4-6%) deflation (yet bond investors somehow think QE is their “friend”).

The Two Sides Of Bond Market History

We aren’t betting on any future deflation, let alone the significant consumer price deflation that would be required to reward today’s government bond buyers with any sort of decent real return.

One of the better bond forecasting tools over the past several decades involves no inflation forecast whatsoever. It turns out the prevailing yield on the 10-year Treasury has provided a wonderfully accurate forecast of bond market total returns 10 years out. In fact, the correlation between current yields and the subsequent 10-year total return is a stunning 0.96 based on monthly data back to 1930!

- As accurate as these forecasts have proven, they have never been bullish enough throughout the 30-plus year secular bond bull. Yields continued falling below the initial “forecast” level, leading to further capital gains. But the scope for such “surprises” has diminished as bond yields have moved toward their zero bound.

- The projected 10-year annualized total return for 10-year U.S. Treasury bonds as of January 31, 2013, is pretty straightforward: it is simply the month-end 10-year Treasury yield of 2.02%. But instead of agreeing with a model that’s been 96% accurate, I’m going to second-guess it and argue this estimate is too high—perhaps by 2-4 percentage points annualized. Check back in January 2023.

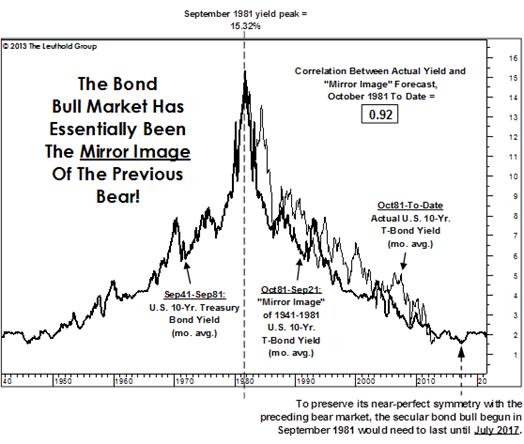

Low Yields: Mirage… Or Mirror Image?

It’s been at least 15 years since I was first introduced to the diagram below. Sadly, I filed it away in the darkest recesses of my bond market files, when I should have used it to load up on T-bond futures (using only the appropriate leverage dictated by the tenets of “risk parity,” of course).

While the prevailing 10-year bond yield has historically offered a good estimate of total bond returns ten years out, the technique below provided us with a surprisingly accurate roadmap to the bond bull market more than 30 years ago!

- The diagram assumes that, at the onset of the secular bond bull market in October 1981, 10-year yields trace out a perfectly symmetrical (or “mirror image”) path relative to the preceding 36-year bear market in bonds. This incredibly simplistic assumption (one that is even more naïve than the one on the preceding page) prescribed a yield path that is 92% correlated with the actual movements in 10-year yields over the past 31 1/2 years. We certainly “get” the great disinflation that has occurred over this period, but one would have a hard time convincing us there isn’t some internal, human “hard-wiring” behind this stunningly symmetric move.

- The symmetry in terms of time isn’t quite complete; according to the diagram, the mirror-image low in yields isn’t due until July 2017. On the other hand, the symmetry in yield level has already been satisfied. In fact, the 1.55% (monthly average) yield record in July 2012 was two basis points below the “model projection.” Bond bulls holding out for the 2017 projection do so at their own peril.

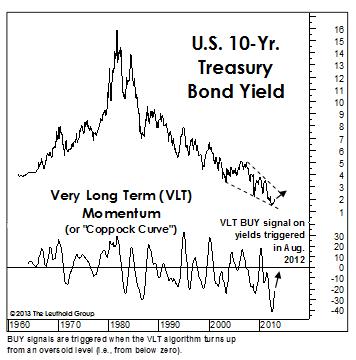

For many decades, we have used the Very Long Term (VLT) Momentum algorithm in our stock market and industry research. But we’ve found the same tool—a “smoothed” momentum measure known by others as the Coppock Curve —useful in other markets like bonds and foreign currencies.

- U.S. 10-year Treasury bond yields hit an all-time low of 1.43% on July 25, 2012. A few bold forecasts of sub-1% yields surfaced around that time, but just over a month later VLT quietly issued a long-term SELL on the 10-year Treasury bond (or, alternatively, a BUY signal on 10-year yields). Yields have risen “only” 60 basis points in the five months following this bear signal—a fraction of the yield spike that often follows such VLT upturns. Bernanke’s announcement of “QEternity” came along two weeks after this major signal. However, if VLT has truly confirmed a cyclical change in the bond market, QE will provide little resistance.

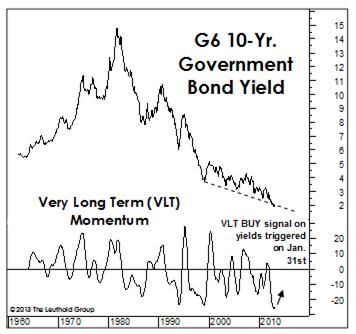

- The mania for long-term government paper extends to other developed countries with equally suspect issuer credentials. Our composite of “G6” 10-year bond yields dipped below 2% for the first time ever in November 2012, before ticking up enough the last two months to trigger a VLT bear signal. The disadvantage (and sometimes the beauty) of this type of signal is that we don’t know why it’s occurred. But the “confirming” action in foreign markets is another reason to suspect the upswing in U.S. yields is for real.

- Might the bond market vigilantes be back at last?

Yields And Stock Prices

Question : When will rising rates become a problem for stocks?

Response : First, to completely circumvent your question, we suspect the next bear market in stocks will be triggered by something other than a rise in rates. We’re already convinced the bull market is in its final innings; rising bond yields (or rising short-term rates, for that matter) aren’t currently on the short list of things we’re watching. But that, of course, could change.

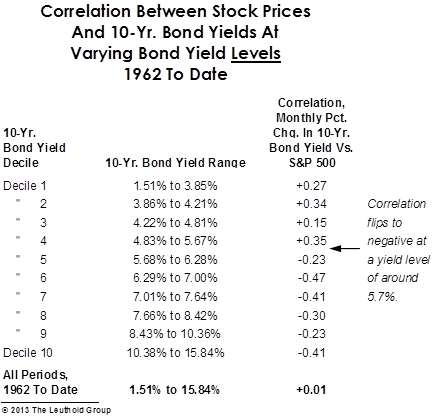

Historically, rising bond yields have not typically posed a threat to stocks until 10-year Treasury yields climbed to about 6%. As shown in the table below, the correlation between monthly changes in stock prices and bond yields has been positive at yield levels of 5.67% and below. We’ve facetiously said before that yields could triple before they pose a threat to stocks. But the reality is that yield increases will blow out the federal deficit (via increased interest expense) long before the old 6% threshold is reached. So the table below, though instructive, might be of limited future value for stock investors.

Today’s low yields are the symptom of sluggish nominal activity. Accelerated economic growth, along with a whiff of inflation, could be bullish for the stock market in a manner that would outweigh the stiffer competition from higher yields—up to a point. But we’re convinced that point is well below 6%.

Visit www.leutholdfunds.com for further information and research.

Disclosures

This report is not a solicitation or offer to buy or sell securities. The Leuthold Group, LLC provides research to institutional investors. It is also a registered investment advisor that uses its own research, along with other data, in making investment decisions for its managed accounts. As a result, The Leuthold Group, LLC may have executed transactions for its managed accounts in securities mentioned prior to this publication. The information contained in The Leuthold Group, LLC research is not, without additional data and analysis, sufficient to form the basis of an investment decision regarding any one security. The research reflects The Leuthold Group, LLC’s views as of the date of publication, which are subject to change without notice. The Leuthold Group, LLC does not undertake to give notice of any change in its views regarding a particular industry prior to publication of their next research report covering that industry in the normal course of business. The Leuthold Group, LLC may make investment decisions for its managed accounts that are inconsistent with, or contrary to, the views expressed in current Leuthold Group, LLC reports. Weeden Investors, L.P., Weeden & Co., L.P.'s parent company, owns 22% of Leuthold Group’s securities. A Managing Director of Weeden & Co., L.P. is a member of The Leuthold Group, LLC board of directors. Weeden & Co., L.P. member FINRA, NASDAQ, and SIPC.

© The Leuthold Group 2013