Out With the Dragon In With the Snake

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

|

During this Chinese New Year, more than a billion people will be welcoming in the Year of the Black Water Snake, celebrating with family and friends all week long. The previous Year of the Black Water Snake was in 1953, which was when China launched its first Five-Year Plan and the average annual income for a family in the U.S. was about $4,000.

As the Dragon took its last breath of the year, it exhaled plenty of fire into China: Looking at year-over-year data as of the end of January, new bank loans, passenger car sales and exports all rose while inflation was slightly lower. Imports of key commodities we track, crude oil, aluminum and copper, were also exceptional, with month-over-month increases of 6 percent, 4 percent and 3 percent, respectively.

Increasing money supply and easing policy in China have also helped to breathe life back into China’s equity market. Below is an update of the chart we showed Investor Alert readers back in October when the venomous sentiment toward China was at extreme levels. We believed Chinese stocks were significantly undervalued compared to emerging markets and that its equities were due for a rebound. I indicated that an increase in money supply would be the needed oxygen for an equity resurgence.

Over 2013, we expect the government to continue its accommodative efforts, which should reinforce the equity rally. In addition, the new pyramid of power is focused on growth, as it seeks to improve and reform policies that will provide its residents with opportunities and social security, increase incomes and raise standards of living, which should encourage domestic consumption.

Growth is set to be considerable over the next several years: Jefferies Equity Strategy team anticipates that China’s GDP will grow at a compound annual growth rate of 6.9 percent and by 2025, will almost equal that of the U.S.

In addition, China’s GDP per capita is projected to climb to about $18,000 on a purchasing power parity and domestic consumption is likely to make up a larger portion of its GDP, jumping from about 49 percent in 2012 to 73 percent of GDP by 2025, says Jefferies.

To achieve these goals, there needs to be significant reforms to promote a “new urbanization.” While China has been anticipating the rise of urbanization by building out the country’s infrastructure of medical services, housing, water, high speed rail system, and roads, the mobility of many residents remains restricted by its internal residence status, called the hukou (pronounced “who-cow”).

First put into place in 1958, the hukou system was a means of controlling migration throughout the country. It designates where a person or household may reside by geographic area. According to J.P. Morgan’s Jing Ulrich, “the system’s primary function was to maintain a sufficient agricultural labor force, while preventing excessive strain on urban resources.”

Under this registration system, if a resident does not have an urban hukou, the family has no access to social benefits such as free education, health care and pensions that are provided to permanent residents of that city.

Michael Ding, portfolio manager of the China Region Fund (USCOX), was raised in rural Dalian and remembers what it was like living under the registration system, which he says was driven by the government’s need to ration food. Still fresh in leaders’ minds were memories of millions of people dying from starvation, and the government wanted to ensure there was enough food for urban residents.

With this upbringing, Michael developed a knack for quickly understanding rationing systems, as his family was unable to purchase additional food regardless if they had money or grow vegetables in their backyard.

So while it was reported that more than half of China’s population lives in an urban area, only about one-third of the total population holds an urban hukou. Andy Rothman from CLSA calls these roughly 250 million migrants “quasi-urbanized,” which means that one worker lives in the city, while the rest of the family remains in the rural home. This equates to a real nationwide urbanization rate of only about 35 percent. You can see in Jefferies’ chart how the official urban residence status differs across the country compared to the urbanization ratio.

If the government reforms the hukou, it is estimated that 600 million people might move to the cities over the next 20 years. This includes 300 million migrants becoming “new urban residents” and 300 million rural residents moving to urban areas by 2030, says Citi Research. According to its data, “urbanization could bring another 150 million surplus rural laborers to the cities.”

“[P]otential reforms in hukou registration and healthcare systems together with extended substance allowance will likely encourage more migrant workers to live in cities for the long term with higher consumption propensities,” says Morgan Stanley. Because urbanization is a big driver for the housing market, CLSA believes property sales in China’s 600 third-tier cities could significantly benefit from hukou reform, as about 100 million migrant workers currently reside in these cities.

The government has begun to factor in the massive ramifications of these families moving to the cities. According to J.P. Morgan, “investments in urbanization are already placing a heavier emphasis on the human benefits of development.” Regarding social housing, in 2012, the country met its goal of starting on 7.2 million units and completing about 5 million units, according to the research firm. For 2013, China’s plans call for an additional 10 million units that will be under construction or complete by the end of the year.

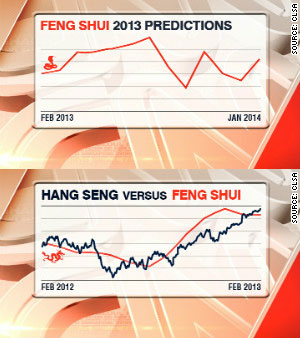

What to Expect in the Year of the Snake: Bite or Might?

Maybe both, if you follow CLSA’s Feng Shui Index. Every year since 1992, CLSA Asia-Pacific Markets team takes a lighthearted look at the fortunes that may befall the Hang Seng Index.

|

During the Year of the Dragon, CLSA’s predictions of the Hang Seng Index came amazingly close to how stocks actually performed. Equities in China fell into a bit of a slump toward the beginning of the year. Then the Dragon woke up and fired up the markets toward the latter half of the Chinese year.

Over the next several months CLSA foresees Chinese stocks to slink like a snake, rising in the beginning of the year before sidewinding in the latter half of the year. According to CLSA, the elements fall out of balance, as “the crucial Fire element all but dies away, Earth falls, Metal overshoots and Water puts a damper on prospects.”

Download your copy of CLSA’s Feng Shui Index here.

In times of growth, a young snake sheds its skin often, sloughing off a worn exterior to reveal a fresh layer of scales. The Asian giant has experienced growth the world has never seen before, and during the Year of the Snake, we look forward to seeing a new leadership take action, sloughing off worn policies to unveil a stronger vibrant economy. See how we’ve positioned the China Region Fund to benefit from this potential growth.

Index Summary

- The major market indices generally finished higher this week. The Dow Jones Industrial Average fell 0.12 percent. The S&P 500 Stock Index increased 0.31 percent, while the Nasdaq Composite gained 0.46 percent. The Russell 2000 small capitalization index closed the week with a 0.27 percent gain.

- The Hang Seng Composite Index fell 2.04 percent; Taiwan rose 0.65 percent, while the KOSPI fell 0.35 percent.

- The 10-year Treasury bond yield fell 7 basis points this week, to 1.95 percent.

Domestic Equity Market

The market ended higher for the sixth week in a row and continues to power ahead. Earnings season is winding down and earnings have been well received. With earnings more or less in the rearview mirror, focus will likely shift back to macro factors influencing the market which could potentially add volatility.

Strengths

- The consumer staples sector led the way this week with broad based strength. Food related stocks have been strong all year with household names such as Tyson Foods, Hormel Foods and Dean Foods among year-to-date leaders.

- Technology was also strong this week led by FLIR Systems, First Solar and Electronic Arts. Apple was also a strong performer this week on talk of returning more cash to shareholders.

- FLIR Systems was the best performer in the S&P 500 this week rising 12.19 percent. The company reported mixed results but the outlook for 2013 was strong.

Weaknesses

- The telecom services sector was the worst performer but the losses were modest and likely just taking a breather after strong performance the past two weeks.

- The materials sector was among the worst performers for the second week in a row with continued weakness in the chemicals complex with FMC Corp, CF Industries and PPG Industries among the worst performers.

- McGraw-Hill was the worst performer in the S&P 500 this week losing 26.9 percent. The Department of Justice is filing a civil case against Standard & Poor’s (a McGraw-Hill subsidiary) in relation to mortgage ratings.

Opportunity

- Earnings will begin to wind down next week but there are still notable names that will report including Coca-Cola, Cisco Systems and PepsiCo.

Threat

- After the best January in more than 20 years a pullback would almost be expected.

The Economy and Bond Market

Treasury bond yields declined modestly this week as economic news was sparse and what was released was more or less in line with expectations. There was a reactionary flight to safety into Treasuries early in the week as political rumblings in Spain and Italy caused a knee-jerk reaction. Later in the week European Central Bank (ECB) president Mario Draghi commented on the importance of exchange rates to price and growth stability. The market took that as a sign the ECB is concerned about the strength of the euro, which recently hit the highest levels in six months.

Strengths

- The January ISM nonmanufacturing index was little changed from last month but remained at a high level and indicates continued economic improvement.

- January retail sales appeared to be better than expected as same-store sales rose 4.5 percent. The U.S. Census Bureau will release official January results next week.

- Chinese economic data for January was generally better than expected with strength seen in exports and money supply.

Weaknesses

- Factory orders in December rose 1.8 percent but were well below the 2.8 percent expected.

- Fourth quarter productivity fell 2 percent as unit labor costs rose 4.5 percent and hours worked rose 2.2 percent.

- Political volatility surfaced again in Europe this week and reminds us of the still relatively fragile nature of the recovery.

Opportunity

- The debt ceiling debate appears to be pushed into May, allowing the market to focus on economic fundamentals.

- While some Federal Reserve members expressed concerns over continued quantitative easing, the Fed still remains committed to an extremely accommodative policy until the economy improves.

- Globally central banks are increasing their stimulative policies, as Japan’s recently elected prime minister vowed to take on deflation and deflate the Yen.

Threat

- The economy appears to gaining momentum and bonds have sold off, the risk for bondholders is that this trend continues.

Gold Market

For the week, spot gold closed at $1,667.20, down $0.25 per ounce, or 0.01 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, gained 0.43 percent. The U.S. Trade-Weighted Dollar Index gained 1.42 percent for the week.

Strengths

- One more stroke in the column for “Peak Gold” production this past week with Peru’s Minister of Energy and Mines reporting that gold production was down nearly 3 percent for 2012. Platinum is also getting traction now with trading taking the price to a 16-month high on concerns that strikes and spiraling operating costs in South Africa will restrict supply. South Africa is the world’s largest platinum producer accounting for 73 percent of global output.

- Mainland China’s gold imports from Hong Kong increased 94 percent to a record 834 million tons per annum in 2012. This data coupled with recent strong volumes on the Shanghai Gold Exchange reinforce the robust demand story in China. With volatility so low, the Chicago Mercantile Exchange announced this week that margin requirements on gold, copper, silver, and platinum futures will be lowered as of the close on February 12. Cash posting for gold futures are set to be lowered by 10 percent.

- Silver Wheaton announced an updated 2013 production guidance of 33.5 million ounces of silver equivalent including 145,000 ounces of gold. The company forecasts 2017 production to reach 53 million ounces of silver equivalent, an 80 percent increase over 2012 production. This news come on the back of Silver Wheaton’s recent $1.9B acquisition of 25 percent of life-of-mine production from Vale’s Salobo mine, and 70 percent of 20-year streams from some of Vale’s Sudbury mine complex.

Weaknesses

- Australian Treasurer Wayne Swan reluctantly announced that Australia raised only $131 million in tax revenue during the second half of 2012 through its Mineral Resource Rent Tax (MRRT). The country’s Treasury had forecasted the tax would raise over $3.0 billion over the full fiscal year ending June 2013.

- The General Mining Act of 1872 was enacted to encourage development of the frontier enabled gold prospectors to remove precious metals and other minerals from U.S. lands without paying royalties. Opponents of this policy regularly lobby the public that this policy allows highly profitable mining companies to extract these minerals for free. Environmentalists stress these resources are the property of every American and that imposing royalties would raise billions of dollars for the government. However, as in the recent example above involving Australia, very little money was brought in and, as we have observed, governments tend to lean towards imposing too high of a royalty and thus the minerals stay in ground with no economic benefits captured.

- George Topping and David Hove from Stifel Nicolaus dug deeper into the all-in cash costs measure suggested by the World Gold Council that would vastly understate the cost of gold production at around $1,100. Realistically, the four senior gold producers real total cost of production is closer to $1,800. We commented previously on Newmont’s gold production decrease from 7.5 million ounces to 4.98 million ounces over 10 years despite spending $16 billion in capex. Topping noted the picture was not any better for Barrick Gold according to the report; over the last six years Barrick’s gold production declined 15 percent to 7.3 million ounces, all this while spending $20 billion in capex. He is completely right in pointing out that if a company is not increasing production then all capital expenditures must be considered sustaining capital expenditures. We are in agreement that if you do not measure your costs, you will not get an improvement in your performance.

Opportunities

- According to Bank Credit Analyst (BCA) research, the gold equity selloff represents a nadir in investor sentiment, typical of major bottoms. Gold equities are trading back at 2007 levels while bullion prices have increased two-fold since 2007.

- BCA notes that money flows have largely been channeled to physical gold ETFs and have bypassed gold mining stocks in this cycle, thus the major gold stock indexes have underperformed. BCA suggest that in addition, during periods of extreme risk aversion the appetite for bullion is simply greater. However, BCA believes 2013 will likely be dominated by decreasing “tail risk” which makes a strong case for a rerating of individual gold mining stocks versus buying bullion.

- Investor disappointment by generalists over the last few years in the senior gold mining companies has left many gold equities under owned and cheap. Six gold mining CEOs lost their jobs last year in shakeups that are usually an indication of significant shifts in corporate strategy according to BCA.

Threats

- Fred Hickey, editor of The High-Tech Strategist, noted in his most recent issue “Up It Goes, Until It Blows – Round 3” that the Dow Jones Industrial Average had its biggest January gain in 19 years. Investor bullishness is approaching levels seen in 2007 and the CBOE Volatility Index is near multiyear lows.

- Hickey eloquently captures the enthusiasm of the market towards an investment in bullion at this point in the cycle. “Gold? We don’t need no stinkin’ gold. You only need that when there’s fear.” After all, Goldman Sachs just last month forecast a gold price of $1,200 an ounce by 2018 and Credit Suisse analyst Tom Kendall stated that he believes it is highly likely we have seen the absolute high in gold prices.

- Hickey in his previous 25 years of newsletters noted he had only used the title “Up It Goes, Until It Blows” in two prior issues. The first time was in December 1999, when the Fed was vigorously pumping money into the system as Y2K approached. Nasdaq peaked in March at 5,000 and that was the end of the “Tech Bubble.” In reaction to that the Fed began a process of slashing interest rates, driving up real estate and market prices to levels that were delusional. This prompted Fred to pin a second essay “Up It Goes, Until It Blows (Again)” in June 2007. Investors then found out what a credit crisis felt like with all that debt on the books. Incidentally, the debt has not gone away and the Fed has now embarked on unlimited quantitative easing.

Energy and Natural Resources Market

Strengths

- Copper remains well supported near $3.80 per pound after data showed that copper imports by China, the world’s largest user, advanced by 2.9 percent in January from a month earlier as trading firms bought the metal before Lunar New Year in preparation for a recovery in demand in March. Inbound shipments of refined metal, alloy and products were 351,000 metric tons last month, the General Administration of Customs said on its website this week.

- Positive data continues to flow from China as the country reported that January coal imports rose 56 percent from a year ago, according to data released by the Beijing-based General Administration of Customs.

- Brent crude oil continued its ascent, rising as high as nearly $118 per barrel this week, reflecting a tighter fundamental picture as demand prospects improved amidst optimism for global economic growth. Also contributing to the rise were indications that Saudi oil production held steady in January after the kingdom cut output in November and December 2012 to the lowest level since May 2011, according to IEA estimates.

Weaknesses

- China’s January coal imports fell 13 percent month-over-month, against record December imports according to preliminary customs data.

- According to China Iron & Steel Association, the country’s crude steel output fell 0.45 percent to 1.906 million metric tons in the last 11 days of January compared with 1.914 million metric tons in mid January.

Opportunities

- The U.S. Federal Reserve's balance sheet grew to a record size in the latest week, Fed data released on Thursday showed. The Fed's balance sheet - a broad gauge of its lending to the financial system - stood at a record-large $2.997 trillion on Feb. 6, compared with $2.991 trillion on Jan. 30 and the previous record of $2.994 trillion as of Jan. 23. The Fed's holdings of Treasuries totaled $1.717 trillion as of Wednesday versus $1.710 trillion the previous week.

- U.S. coal markets may tighten on the news that workers at Colombia's largest coal exporting company, Cerrejon, began a strike on Thursday. The company’s first in more than two decades began after the two sides failed to reach an agreement during last-minute talks on wages and benefits. The dispute adds to problems in the Andean nation's coal industry, which is facing an environmental inquiry into Drummond, the second-largest exporter, and a dispute at a mine owned by a Goldman Sachs Group, Inc. affiliate. In total, about 85 percent of Colombia's daily coal production will be shut down as a result of the sector's recent problems.

Threats

- A new IHS study challenges assumptions that China will remain a top coal importer. The study suggests that the imports will drop on the back of a moderation of demand along with a rise in domestic supply, improved transportation and a diversification of fuel sources. The analysis suggests that the imports may have peaked at 145 million tonnes of standard coal equivalent in 2012 and should now enter a gradual decline through 2035.

- Geo-political risk for natural resource development projects are always a threat. The government of Mongolia is withdrawing support for a potential $6 billion in project financing that Rio Tinto is negotiating with lenders including the European Bank for Reconstruction and Development, the World Bank’s International Finance Corp. and private sector banks. Rio Tinto Group plans to resume talks with Mongolia this month to resolve concerns that spending at their jointly owned Oyu Tolgoi mining project is overshooting and the country is not benefiting enough from the development. Shareholders met in Ulan Bator yesterday to discuss outstanding issues surrounding the gold and copper venture.

Emerging Markets

Strengths

- China January money supply (M2) was up 15.9 percent year-over-year, beating the market estimate of 14 percent. New January bank loans were Rmb1.07 trillion, or 15.4 percent year-over-year, better than the market expectation of Rmb1 trillion. Total Social Financing increased Rmb2.54 trillion versus Rmb1.63 trillion in December last year.

- China January exports were up 25 percent year-over-year, better than the market estimate of 17.5 percent; imports were up 28.8 percent, also beating the market expectation of 23.5 percent. In spite of belated January base effect last year, the number showed a positive trade trend which can drive up shipping rates and port throughput.

- China January Consumer Price Index was in line with the market expectation at 2 percent year-over-year, and the Producer Price Index was also in line with market expectation down 1.6 percent, which was improved from negative 1.9 percent in December, showing the demand recovery.

- China January passenger vehicle sales were up 49 percent year-over-year, primarily due to a lower base last year and higher demand prior to Chinese New Year which falls on February 10.

- Hong Kong loan and deposit (ex-Rmb) grew 9.6 and 8.8 percent in 2012. Annualized fourth quarter loan and deposit growth rose to 11.2 and 18 percent respectively, supporting a robust property market.

- China January HSBC service Purchasing Managers Index was 56.7 percent versus 51.7 percent in December, driving a strong service sector performance in H shares.

- Chilean exports surged 7.4 percent to $6.94 billion in January year-over-year on the back of increased demand for copper exports to China. The resulting $244 million trade surplus crushed analyst expectations for a $120 million trade deficit.

Weaknesses

- Increasing fears of government intervention in curbing the housing market had caused negative sentiment for developer stocks in Hong Kong listed H shares in spite of robust January sales and price increase.

- Indonesia 2012 GDP growth slowed to 6.2 percent versus 6.5 percent in 2011, primarily due to business unfriendly regulations and weak global commodity demand over the past year which dampened investment and consumption growth, though the economy is still robust.

- The Colombian government has suspended Drummond’s coal port operating license as it investigates the company’s responsibility in the dumping of a coal load into the ocean earlier this year. This added to the work stoppage at Cerrejon Mine, Colombia’s largest coal producer by output, has brought 80 percent of the country’s coal production to a halt. Colombia is the fourth largest coal exporter in the world with an annual output of 91 million tons.

Opportunities

- The chart above shows China January total social financing increased to a record high, indicating China’s investment demand is in momentum. Recent data also showed M1/M2 ratio is turning up after being on the down trend for most of 2012. This indicates that faster deposit growth allows the banks to lend more to the economy, confirmed by better-than expected January bank loans.

- Peru’s Central Bank President Julio Velarde has encouraged pension funds to increase their investments abroad in an attempt to devalue the sol from a 16-year high. The Finance Minister of Colombia has vowed to decrease U.S dollar borrowing in favor of local currency borrowing and to narrow the fiscal deficit in an attempt to prevent further Colombia peso revaluation.

- An almost 10 percent correction in Turkish stocks since the recent high presents a buying opportunity, according to J.P. Morgan. There has been no change in the macro outlook, as evidenced by the practically unchanged bond yields and lira exchange rate.

Threats

- The People’s Bank of China (PBOC), the central bank, warned of inflation pressure as global central banks are increasing money supply through quantitative easing. Though there probably is no immediate inflation threat in 6 to 9 months, the price increase for energy, materials and food (please refer to the natural resources section of this report) year-to-date are indeed at relatively fast pace and threatens China as the country’s investment demand is recovering.

- Brazil has vowed to allow the Brazilian real to appreciate a further 5 percent before resuming its currency intervention policy amid stagflation concerns. The expansive monetary policy pursued over much of last year accelerated inflation to 6.15 percent while GDP growth remained around the 1 percent level.

- Regulatory action, competitive pressure, and austerity measures are impacting revenue recovery of Eastern European telecom companies, making it difficult for them to maintain current high dividend yields.

© US Global Investors