Currency War or Something Altogether Different?

“Anyone who does not understand that the price of every stock and every bond is being artificially altered by the fact that interest rates are being manipulated by the Federal Reserve should not be risking any money in the markets.”

Michael Lewitt, The Credit Strategist

“Who is afraid of currency wars?” asks Gavyn Davies in the FT (see here). I have known Gavyn for 25 years and have to confess that he is way out of my league intellectually. He is one of the smartest people I have ever met and, thankfully, also one of the humblest. He rarely gets things wrong so, when I occasionally disagree with him, it always makes me slightly uneasy. In his latest post in the FT, he makes the valid point that the currency war debate has flared up yet again following newly elected Japanese Prime Minister Abe’s decision to change tact and openly bully his own central bank into action.

Yet Gavyn - and he is certainly not alone in that regard – ignores one important aspect in his argumentation and that has to do with what actually drives exchange rates. Just because a currency is depreciating doesn’t mean it is subject to manipulation. A quick look at chart 1 makes it pretty clear that the recent weakening of the yen is just a tiny blip on the curve (a rising bar equals a weaker yen).

Over the past 52 weeks USD/JPY has moved from a low of about 76 to a shade below 93 today. Towards the end of the great equity bull market in the late 1990s USD/JPY was close to 150. 15 years earlier, at the beginning of the same bull market, one U.S. dollar would cost you over 250 yen. For political leaders all over the world to openly attack Japan now that the yen has given back just a tiny fraction of those massive gains of the previous three decades, is simply preposterous.

Before anyone accuses me of being hopelessly naive, let me make one thing very clear. I have no doubts whatsoever that, given the economic and fiscal predicament many governments find themselves in at the moment, currency manipulation (as in “let’s manage it down”) is on most political agendas. They probably all want to do it, but they can’t all succeed in doing it, at least not simultaneously. There is however an altogether different, yet poorly understood, reason why currencies may depreciate over time (in the following I shall ignore all the trivial reasons why exchange rates move, such as interest rate and inflation differentials, etc.).

Chart 1: USD/JPY over last 40 years

Source: Bloomberg

It all begins with the outlook for bond yields which, if you believe various commentators, is extremely bleak. In fact, tracking down a bond bull these days is almost as hard as stumbling across snow clearing equipment anywhere near a UK airport on a snowy day. In truth, I cannot recall ever having encountered as much bearish sentiment when it comes to the outlook for bond prices, as I see in the markets today. The low yield environment, or so the argument goes, is bound to end in tears as the bond vigilantes eventually gain the upper hand and punish governments for their profligate spending. The question I will be asking in the following is: could this argument possibly be flawed?

Accounting identities matter

Now, let’s remind ourselves of a couple of general misconceptions. Firstly, the notion that foreigners can pull out of, say, UK assets just because they lose faith in UK economic policy is fundamentally flawed. National income accounting principles assure that net foreign capital inflows into the UK will always equal the UK current account deficit (the flow identity). For precisely the same reason, the total stock of UK assets held by foreigners must equal the sum of all past deficits (the stock identity). These two principles are accounting identities and will always be valid, whatever country you look at. So long as a country runs a current account deficit, foreigners will accumulate claims on it whether they wish to do so or not. Likewise, countries that run a surplus will accumulate claims identical to the size of the surplus.

The second mistake is the failure to recognise that when foreigners become disenchanted with Her Majesty’s Government, they can be ‘appeased’ either through higher bond yields or through reduced currency risk. In plain English, the bond market is not the only adjustment mechanism. Whilst we all sit and wait for bond prices to fall out of bed, the currency may in fact take the brunt of the adjustment.

Hence the question investors should really be asking themselves is under what circumstances will bond yields rise and under what circumstances will the currency weaken? This has little to do with currency wars and much more to do with an economic theory developed by James Tobin (amongst others) back in the 1970s and 1980s.Let’s have a crack at it.

How the theory works

The first factor to consider is asset preferences. Let’s assume that foreign investors have become disenchanted with UK bond yields which they consider to be unattractively low. As a result, they wish to sell their UK gilts and invest the proceeds in UK equities instead (remember, they cannot ‘exit’ UK assets altogether due to the accounting identities discussed above). Assuming domestic investors’ asset preferences remain unchanged, virtually all the adjustment will take place in the currency markets. The logic is straightforward. Since domestic investors’ asset preferences are unchanged, the moment they observe falling bond prices and rising equity prices, they will take advantage of those price moves and reinstate what they consider to be the equilibrium between bond prices and equity prices. As a result, under the circumstances described above, the currency bears the brunt of any adjustment necessary to appease foreign investors. By the same token, should domestic and foreign investors become disenchanted at the same time, bond yields will rise whereas the currency will only be modestly affected.

Precisely the same argument can be put forward as far as inflation expectations are concerned. Should these change simultaneously for domestic and foreign investors, bond yields will rise. Should foreign investors change their inflation expectations for the worse whilst domestic investors remain more sanguine, the currency will take most if not all of the impact.

The third dynamic to consider is trade and hence the current account deficit. Assume for example that foreign investors’ asset preferences have begun to affect the exchange rate. This may in turn have an effect on the trade deficit over time, as the weakening currency is likely to favourably impact the level of competitiveness. Then again, the more the trade deficit improves as a result of the weakening currency, the more bond yields may rise over time due to the law of supply and demand of funds. Why? Because the improving trade deficit leaves fewer pounds in the hands of foreigners to be invested in UK assets.

Finally, consider the savings rate. It may or may not change as a result of the above but let’s assume for argument’s sake that total domestic savings increase by an amount equal to the improvement in the trade deficit. If that were to happen, the supply/demand argument in the previous paragraph falls away, as the falling demand from foreign investors due to the improving trade deficit will be offset by increased demand from domestic investors due to the growth in savings. In this case, bond yields will be unaffected.

Could currencies soak up most of the pressure?

When Tobin put his ideas into economic theory, he had no reason to suspect that, in 2008, the world would very nearly be overwhelmed by the most dramatic economic crisis since the Great Depression. Nor could he foresee that, as a result of that crisis, a fifth dynamic would enter the frame, namely that of central bank policy.

Over the past few years monetary policy has become largely synonymous with asset price manipulation, mainly executed through regular bond market interventions. This has only reinforced my belief that, before this crisis is well and truly over, foreign exchange rates are more likely than bond yields to endure a period of extreme volatility, and any investor who positions himself for a major bear market in bonds may end up thoroughly disappointed. Chart 2 below illustrates very well that, despite the recent weakening of the yen, currency volatility remains at very suppressed levels. This may be about to change.

Chart 2: USD/JPY 3-Month Volatility

Source: Bloomberg

Consider the economic reality and the options available to policy makers. A mountain of debt so huge that it almost defies belief. Under normal circumstances, the best prescription for debt elimination is economic growth but, in the current environment, it will be next to impossible to engineer enough of it to solve the problem through growth alone.

The most effective tool at policy makers’ disposal may be a ‘controlled’ rise in inflation (I use inverted commas because, once the inflation genie is out of the bottle, there is always a risk that policy makers lose control) combined with artificially suppressed bond yields, in effect setting the stage for negative real yields for a sustained period of time. Japan has already moved its inflation target to 2%. It won’t be long before the first central bank drops its inflation target altogether – if not explicitly then implicitly – and begins to prioritise growth over inflation.

Negative real rates (low funding costs on existing debt combined with modestly higher inflation) will do the job over time, as long as investors are cognisant of the fact that ‘over time’ means many years. There are no easy solutions.

Recapitalising the banks

The added advantage of this strategy is that the banking system will be able to recapitalise itself without the use of tax payers’ money. Well, not entirely correct. There is no explicit use of tax payers’ money in this model; however, zero rate interest policy is enormously damaging to all those people who rely on their savings to take them through retirement, but that is a story for another day.

The recapitalisation of the banking sector has been made possible through an undertaking that central banks will keep policy rates low for an extended period of time. This permits banks to engage in a virtually risk-free carry trade by borrowing at the short end of the curve and investing at the long end – levered up many times.

No appetite for ‘nuclear’ options

So, in summary, expect various measures of economic stimulus, expect the bond market to be manipulated through regular interventions and expect inflation to drift higher. I believe that will be the core ingredients of economic policy for years to come. It is a high risk strategy. Not only may the inflation genie be let out; it is also a strategy that encourages reckless investor behaviour and thus repeated asset price bubbles, but what are the alternatives? The Austrian school of economics advocates wholesale bank closures and other ‘nuclear’ solutions, but I see no political appetite for such drastic methods.

This leads me to make the first two predictions of 2013:

- public spending, and thus government deficits, will stay high for much longer than generally perceived, and

- the combination of monetary and fiscal policy currently being pursued in the U.S., Europe and Japan, is likely to lead to big changes in exchange rates over the next few years.

This begs the question: Since not all currencies can simultaneously depreciate in value, which ones are likely to appreciate and which ones will most likely depreciate?

Let’s do a little detour by reviewing how the world’s major currencies have actually performed over the past twelve months. Charts 3 a-d, which I have borrowed courtesy of Zero Hedge, provide a graphic illustration of the performance of each of the four currencies (you can see the whole study here).

If the chart is predominantly green, the currency being reviewed has depreciated in value against most other currencies in the world over the past twelve months. On the other hand, if it is mostly red, the currency has been strong over the past year. Now look at the four charts.

The charts pretty much speak for themselves. The yen has weakened against all other currencies, explaining the coordinated attack on Abe and his much trumpeted Abenomics. Meanwhile, to the horror of the political leadership in Europe, the euro has defied all logic and outpaced all other major currencies over the past year. This is really the last thing Europe needs with almost half of the eurozone countries in dire economic trouble, again explaining why leading European politicians such as German finance minister Wolfgang Schäuble have been particularly outspoken.

Chart 3a: USD v. other currencies over past 12 months

Chart 3b: GBP v. other currencies over past 12 months

Chart 3c: EUR v. other currencies over past 12 months

Chart 3d: JPY v. other currencies over past 12 months

Source: Zero Hedge

Conclusion

Now to the $64 million question: Knowing that not all currencies can depreciate, which ones are likely to fall from here and which ones should gain in value?

The easy one first. Acknowledging the fact that most Asian currencies are artificially low (a point I have made repeatedly in the past), over time, I would expect Asian currencies in general to gradually appreciate in value against all four currencies in our analysis, i.e. USD, GBP, EUR and JPY. As the economic crisis deepens, and it will, those four currency blocks will be prepared to use increasingly desperate measures to stop the systematic manipulation of exchange rates happening across Asia. Eventually, they will succeed.

As far as the four currencies in our analysis are concerned, I strongly suspect that JPY will prove the weakest link. There are at least a couple of reasons for that. The fiscal problems in Japan are well documented and shall need no further substantiation other than to say that the weaker the fiscal outlook - and it is extraordinarily weak in Japan – the higher risk premium bond investors should demand, all other things being equal.

However, the situation in Japan cannot be directly compared to that of Europe and the U.S.; Japan has been running a sizeable current account surplus for decades and, as a result, does not have to rely on foreign investors to finance its deficit as the U.S. and many countries in Europe do. Japan’s current account may be about to take a turn for the worse, but let’s not confuse ‘stocks’ with ‘flows’. Japan still enjoys the second largest foreign exchange reserves in the world (behind China) and will not have to rely on foreigners to finance its deficit for some time to come.

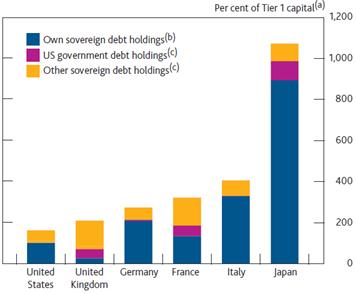

This obviously assumes that domestic investors continue to support the bond market. In that context I note that Japanese banks have effectively taken control of the Japanese bond market with more than 40% of all JGBs now in their hands, and with the combined holdings equal to 9 times their tier one capital (chart 4). You can argue that this is a disaster waiting to happen. On the other hand, you can also argue that the banks simply cannot afford not to continue their support of the Japanese bond market. Anything else would be suicidal.

Chart 4: Sovereign debt holdings by selected banking systems

Source: “Financial Stability Report”, November 2012, Bank of England

Going back to the original discussion, this leads me to conclude that, as long as asset preferences of Japanese investors remain unchanged, the exchange rate more so than the bond market should take the brunt of the adjustment that is likely to come Japan’s way. I would not be at all surprised to see USD/JPY at 120-130 a few years from now.

This is very bullish for Japanese exporters and is the key reason we have recently increased the allocation to Japanese equities in our clients’ portfolios. Meanwhile the currency risk has been hedged in order not to give all the gains away again.

The other extreme to me is the U.S. dollar which I see as potentially the strongest of the four. USD is a very ‘political’ currency, partly because it is the world’s primary reserve currency and partly because so many other currencies around the world are linked to it, whether directly or indirectly. Given all the economic problems facing Japan and countries all over Europe, a substantial depreciation in the value of the greenback would be completely unacceptable.

All of which leaves the two major European currencies – EUR and GBP. Being a much smaller currency, of the two, sterling is the easier one to manipulate. If you add to that the fact that the UK gilt markets are heavily dominated by UK pension funds who are captive investors, the chances are that the adjustment process in the UK will take place primarily through the currency markets which implies that EUR may very well outperform GBP over time, but it is not a straightforward call.

Niels C. Jensen

5 February 2013

© Absolute Return Partners LLP 2013. Registered in England No. OC303480. Authorised and Regulated by the Financial Services Authority. Registered Office: 16 Water Lane, Richmond, Surrey, TW9 1TJ, UK.

Important Notice

This material has been prepared by Absolute Return Partners LLP ( ARP). ARP is authorised and regulated by the Financial Services Authority. It is provided for information purposes, is intended for your use only and does not constitute an invitation or offer to subscribe for or purchase any of the products or services mentioned. The information provided is not intended to provide a sufficient basis on which to make an investment decision. Information and opinions presented in this material have been obtained or derived from sources believed by ARP to be reliable, but ARP makes no representation as to their accuracy or completeness. ARP accepts no liability for any loss arising from the use of this material. The results referred to in this document are not a guide to the future performance of ARP. The value of investments can go down as well as up and the implementation of the approach described does not guarantee positive performance. Any reference to potential asset allocation and potential returns do not represent and should not be interpreted as projections.

Absolute Return Partners

Absolute Return Partners LLP is a London based client-driven, alternative investment boutique. We provide independent asset management and investment advisory services globally to institutional investors.

We are a company with a simple mission – delivering superior risk-adjusted returns to our clients. We believe that we can achieve this through a disciplined risk management approach and an investment process based on our open architecture platform.

Our focus is strictly on absolute returns. We use a diversified range of both traditional and alternative asset classes when creating portfolios for our clients.

We have eliminated all conflicts of interest with our transparent business model and we offer flexible solutions, tailored to match specific needs.

We are authorised and regulated by the Financial Services Authority.

Visit www.arpinvestments.com to learn more about us.

For the theoretical part of this letter I have leaned heavily on the work of our economic consultant Woody Brock for which I am very grateful.

© Absolute Return Partners