This week we consider recent information and data regarding California, GDP and the employment picture. We also touch on “why I worry” about the next six months (at least). We conclude with a wrap up of the data imported into DIVER last week and coming road trips. Also, be on the lookout for a Lumesis press release and “Topic of Interest” paper later this week.

California : S&P lifted the State’s ratings to A.

According to several published reports (yours truly did not have access to the report), there was much ado about California’s budget and the expectation that a surplus of $851 million will materialize. S&P cited, at least according to reports available to us, the Governor’s plan to pay down more than $35 billion of debt. And, one article said, according to the nonpartisan Legislative Analyst’s Office, “the State was on track to collect $5 billion more in tax revenue this month than estimated in Brown’s budget.” The reports noted concrete steps the State has taken to raise revenue – increase income and sales taxes.

Based on what we reviewed, it appears a portion of the basis for the ratings action was based on a budget, an expectation, a plan to act and on pace to collect. Things that will happen according to the State. While I’m sure S&P’s rating action was well-considered and the subject of a significant amount of diligence, the level of reliance on forecasts is striking. We all can point to instances where expectations, plans and our on pace efforts have not come true – not because of a lack of integrity but because an expectation, plan to act and staying on pace are all based on factors and assumptions, many of which are not in our control (would a corporate be upgraded based on their projections for 2013? Should you bet on a horse because she is on pace to win?).

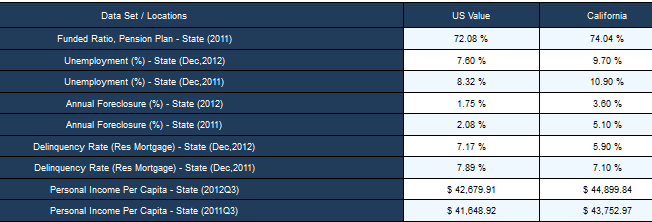

Not to say there are not positive and improving factors critical to California’s economy. The table below highlights some of these factors such as Funded Ratio for Pension Plans, declining Unemployment, Delinquencies and Foreclosures declining and Personnel Income Per Capita up about 2.7%.

Source: DIVER Analytics; Data Access Module.

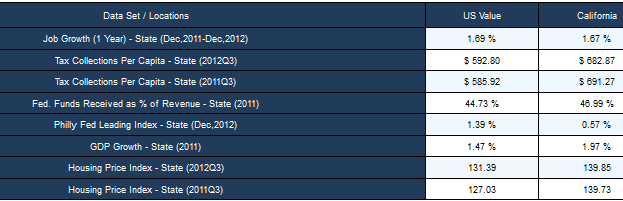

On the other side of the equation: Job Growth is marginal at 1.67%, Tax Collections (year on year) were down, the State has a high reliance on Federal Funds (remember that little issue of indiscriminate spending cuts that kick in March 1), the Philly Fed doesn’t have a terribly favorable view of growth and Housing Prices have been kind of flat.

Source: DIVER Analytics; Data Access Module.

A lot to digest. The point is, as we routinely mention, to look at the factors you deem most critical and draw your conclusion.

Taxes and GDP : Two other items worth noting (and you can apply the second one to California or any other State or municipality for that matter). Let’s start by saying we don’t doubt California’s expectation for increased tax receipts for “this month.” However, restating a point from last week’s commentary, we do wonder how much of that is due to bonuses and dividends being paid in December 2012 to beat the tax increases that went into effect and how much tax receipts for 2013 will be impacted? (An early factor of “why I worry” – more to come). Finally, we all saw that GDP contracted for the US in the fourth quarter but this was brushed off by many as they declared the decline was temporary. Again, we refer our readers to last week’s commentary where we cited the belief of some that the expiration of the tax holiday (check your paycheck v. last year) will have a negative impact on GDP in 2013 taking the expected 2-3% growth to flat or negative. See the table above – we snuck in California’s GDP Growth for 2011 for you. Might that be negatively impacted by increased taxes?

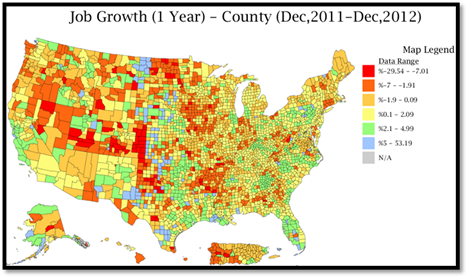

Employment : Friday saw the latest national employment figures from the BLS. Jobs were created (157,000) but the Unemployment Rate went up to 7.9%. Based on a sampling of reports and the equity market’s reaction, the response ranged from very positive to “it could have been worse.” The Liscio report notes that employment growth may be narrowing and note that, at the current rate of job growth, it would take 5 years to get back to the employment /population ratio of the good ol’ days. The following is some data on job growth over the one year period December 2011-2012 (January’s State and county level data has yet to be released).

For the one year period, 1,781 counties (out of 3,235) saw Job Growth (greater than 0%).

Source: DIVER Analytics; Map Module; Bureau of Labor Statistics

We encourage our subscribers to explore the same to understand geographic trends in the context of the possibility that employment growth may be narrowing.

Why I Worry : By now you may think I look at the world with a bit of pessimism. Not true. Its just that I worry that things are not quite as rosy as some make it appear and that too many people subscribe to the philosophy that, so long as the stock market is moving up, all is well (by the way, in many cases, these are the same people who blame pretty much everything on Wall Street).

To the point. I am feeling a bit better that the boys and girls in DC seem to be trying to get a few things done – negotiations yielding results where neither party gets all of what they want. However, what is worrisome is the complete lack of attention to March 1, the Sequestration deadline, and the reality that addressing the deficit, debt ceiling and spending (or revenue) has, yet again, been kicked down the road (at least now linked to the specter of our elected officials losing their pay if they don’t address these issues). As it relates to readers of this commentary, I strongly encourage taking a look at who is most reliant on dollars from their Uncle Sam and have they contemplated their allowance being frozen or cut. Remember, at this point, the cuts are the indiscriminate meat clever – just a few months back people were not thrilled with that idea. Perhaps we’ll be surprised and the scalpel will be used where it should and can. Time will tell. For now, like my Mom would say, “I worry.”

This Week’s Data (and there is a lot) :

- FEMA Disasters, County, Jan YTD 201

- Federal Funds Received, Fed. Funds Received As % Revenue, Fed. Funds Received per Capita, State, 2012

- Philly Fed Leading Index, December 2012, State

- Drought Intensity, County, 1/29/2013

- Weekly Initial and Continued Jobless Claims, State, 1/19/2012

- Recovery Act Contracts, Grants, Loans, and Funds Received, State, Q4 2012

- Homeownership Rate and Homeowner Vacancy Rate, State, 2012 Q4

- UPDATED: Debt Outstanding, as % of Personal Income, and Per Capita (CAFR), 2012, State

- Labor Underutilization, State, 2012 Q4

- CAFRs Filing Index, 2012, State

- UDPATED: Funded Ratio, Pension Plan, State, 2012

- UPDATED: ARC as % of General Fund Revenue and Expenses, State, 2012

- UPDATED: Percent of ARC Paid, State, 2012

- Delinquency Rate (Res. Mortgage), State, December 2012

On the Road : Mike will be in Minneapolis, St. Paul and Chicago this week. Please look for our booth (and us) at the upcoming Bond Buyer, Texas Conference in Austin and be sure to attend the “Municipal Regulatory and Disclosure Update” session. Check our website for the list of conferences we will be attending.

Gregg L. Bienstock

CEO& Co-Founder, Lumesis, Inc.

© Lumesis