Is the world engaged in a “currency war?"

February 1, 2013

- Is the world engaged in a “currency war?”

- January’s job report had some pleasant surprises, but more progress is needed

- Purchasing managers surveys suggest growth in the US, retreat for Europe

Just over forty years ago, major economies agreed to allow exchange rates to float. This ended a long period of fixed currency values, which had been forged at the Bretton Woods conference just before the end of World War II. John Maynard Keynes was among the participants at Bretton Woods.

My fifth grade teacher had used the Bretton Woods fixings to sharpen our skill at multiplying numbers with decimals. I can still recall the conversion rate for the British currency: 2.4 dollars to the pound. Today, a pound costs $1.60. And the rate has fluctuated widely, hitting a low of $1.07 and a high of $2.60 since 1970.

Currency rates have an important influence on trade flows, as variations make one country’s goods more or less expensive to importers. The drive to export is something of an international competition, with trillions of dollars at stake. The stakes become even higher when nations are trying to work their way out of recession.

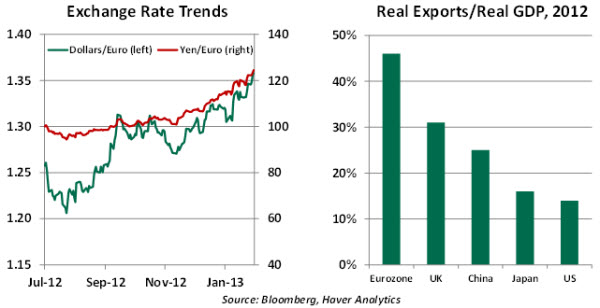

So it isn’t surprising that developments in the currency markets are getting very close attention at the moment. The euro and the yen have been at the center of that attention.

Over the past six months, the euro has appreciated by 10% against the US dollar and by almost 30% against the yen. Coincidentally, central banks here and in Japan are on an aggressive path of quantitative easing to stimulate growth. With more reserves floating around the international financial system and only modest growth in national income, these actions can also have the effect of lowering the value of the national currency.

In public statements, both the Federal Reserve and the Bank of Japan have justified their actions on the basis of their mandates. But that hasn’t stopped some from branding them as currency manipulators, intent on helping their respective Treasury departments gain ground in trade markets. Some have gone so far as to call the present state a “currency war,” or a race among nations to devalue their way to prosperity.

We think these accusations rest on shaky foundations and may, in fact, be counterproductive.

Firstly, there are many reasons why currencies fluctuate, and it is hard to single out central bank action as the sole contributor. Greater demand for goods and investments that originate in a particular country (or region) will make its currency stronger. For example, the recent stabilization of Eurozone debt markets might certainly be credited with aiding the value of the euro. Japan’s weak economy has diminished the yen.

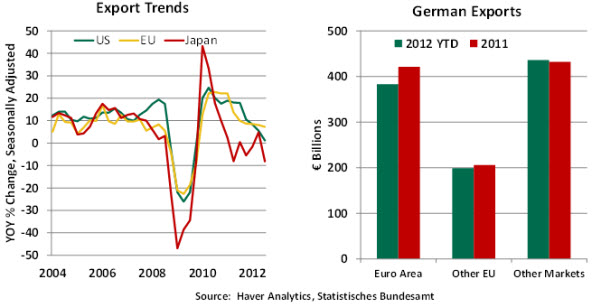

Secondly, the contraction in exports (which, as shown in the charts below, is a global phenomenon) is due in large part to the economic stagnation or retreat that many nations are currently enduring. High prevailing rates of unemployment and losses of income and wealth will diminish consumption on both domestic and imported goods.

Supporting this observation is the fact that German exports to other Eurozone countries have fallen off most sharply this year. The shared currency among these nations prevents any competitive devaluations.

In Europe, the most vocal concern about recent events is coming from Germany. This is understandable at one level; German exports contribute more than 50% to real GDP. But there are those who argue that Germany trades with a currency (the euro) that is weaker than might be the case if Germany were on her own. This advantage has helped German sales to other countries grow by 77% over the past decade.

And many of these new exports have gone to the peripheral countries of the Eurozone. In the event of any reorganization of the currency compact, Germany stands to lose a substantial amount of the ground gained in these markets. Providing aid to its partners in the euro area might be the best stimulus package that Ms. Merkel could enact.

A greater cause for complaint may come from developing countries like South Korea and Brazil, whose export competitiveness has been reduced by the recent strength of their currencies. Their ability to join the devaluation fray is limited; pushing their currencies down has the potential to raise the cost of imported food, energy, and other goods.

Finally, the suggestion that central banks are serving as agents of their governments in pursuing weaker currencies implies that the traditional distance between the two bodies has been diminished. The activism of Japanese Prime Minister Abe in pressuring the Bank of Japan (indirectly and through the upcoming appointment of BoJ governors) to pursue a 2% inflation target has raised concerns on this front.

By and large, however, the wisdom of separating monetary policy and fiscal policy still has tremendous international respect. The lessons of the last generation consistently support central bank independence.

If fiscal and monetary steps in major markets succeed in enhancing growth, then export markets for all nations will deepen. The recent depiction of policy as competition between countries, as opposed to an effort which could to boost the fortunes of all nations, seems myopic.

Employment Report: Some Nice Surprises, But More Improvement Needed

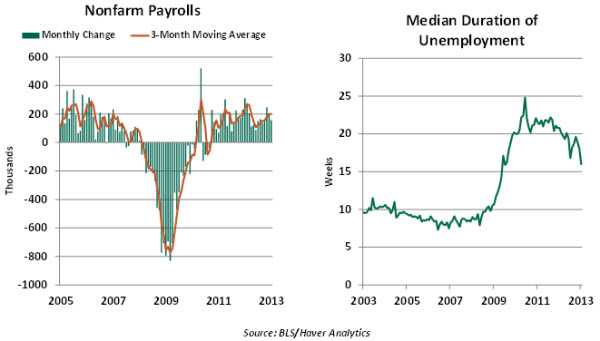

The headlines of the January employment report present a mixed message – A 157,000 gain in payrolls, a slightly higher unemployment rate. One needs to interpret the numbers with care this month because the figures contain a series of annual benchmark revisions.

The revisions to the payroll data added 127,000 more jobs than previously estimated in the November-December months. Average monthly payroll creation was revised up to 181,000 for 2012, much higher than the prior estimate of 153,000. The bottom line is that the job growth was stronger in 2012 than previously estimated.

The details of the establishment survey point to widespread gains in employment in January from construction (+28,000) to private sector services (+121,000). Factory jobs rose only 4,000 in January following a gain of 8,000 in the prior month. Factory payrolls have not moved up noticeably since May 2012 and warrant close tracking. Government payrolls continue to shrink.

Also encouraging was the news that the median duration of unemployment dropped to 16 weeks, down from 19.6 weeks in October 2012 and 20.8 weeks a year ago. Chairman Bernanke has cited the percentage of unemployed for over six months frequently to drive home his concerns about dire situation in the labor market. The good news is that this measure declined to 38.1% in January, the lowest since November 2009.

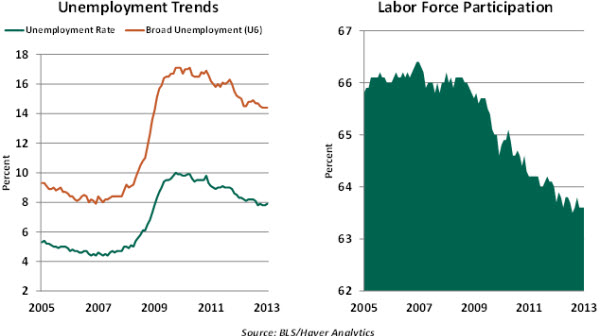

The unemployment rate moved up one notch to 7.9% in January. The labor force has grown by a little over a one million in the last five months and the participation rate is holding steady and not trending down. This combination is a positive development but in the interim it could result in a higher unemployment rate.

Hourly earnings advanced in January, but the trend continues to hover around a 2% pace that suggests only modest growth in consumer spending.

In sum, the January employment report paints the labor market in a different light compared with the situation a few months ago. However, the improvements do not imply that the labor market is out of the woods, meaning that the Fed will not terminate quantitative easing in the near term. At the same time, the good news in today’s release reduces the concern that followed the reported decline of fourth quarter real GDP.

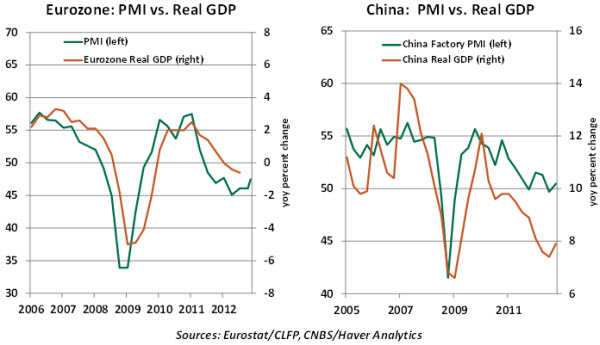

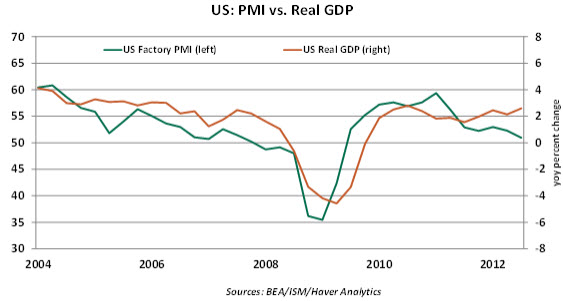

Factory Purchasing Managers’ Index – An Important Economic Signal

Purchasing Managers’ Indices (PMIs) of the factory sector from around the world are published on the first business day of each month and financial markets are sensitive to these numbers. Frequently, central bank rhetoric includes references to PMIs to defend monetary actions.

Factory PMIs are metrics computed from survey responses; they are not actual production data. Purchasing managers respond to questions about output, new orders, employment, prices, and other variables. The composite factory PMI is a weighted average of selected variables. By construction, readings of factory PMIs above 50 denote an expansion and those below 50 imply a contraction.

The factory PMI for a given month is timely as it gives an early indication of the status of business momentum prior to the publication of estimates such as employment, retail sales, and industrial production.

Despite their focus on the manufacturing sector, there is a strong positive correlation between the composite factory PMIs and year-to-year change in real GDP.

The factory PMI of the eurozone has languished below 50 since August of 2011, implying a contracting factory sector. Real GDP in the region has contracted for three quarters in a row. The January mark of the eurozone factory PMI (47.9) reinforces near term projections of soft economic conditions.

Here in the US, factory PMI was a tad below 50 in November, but has rebounded nicely to a level of 53.1 in January. Based on the historical relationship between the composite factory PMI and real GDP growth, it is plausible to infer that the latest reading supports expectations of continued growth in the US economy.

We will be tracking closely PMI readings in the months ahead to assess the likely course of the global economy. Financial markets will take their cues from purchasing managers’ surveys, as will monetary policy makers.

© Northern Trust