In looking back at 2012 for a moment, I think Woody Allen's comment that "80 percent of life is just showing up" is a strong candidate for a truly abbreviated summary.

2012 was the fifth consecutive year of outflows from long-only equity investment vehicles, as an awful lot of investors' time remained preoccupied with "known-unknowns" and the fear that every tick down is a harbinger of another 2008. Political and investment decision-makers engaged in a seemingly perpetual back and forth regarding the nonsense du jour surrounding the state of affairs in this country, much of which provided insight into their own political bias, hopes, and dreams rather than what would constitute a better process or a more favorable outcome.

In the meantime, the leaders of publically traded companies did what 92.5% of the population in this country does-got out of bed, went to work, and tried to make the best of what always seems like the current muddle. And even with the concession that we are living with a pathetically conflicted state of global affairs, the default movement of a generally capitalistic and democratic society is grudgingly forward. Both life and investing become much easier after starting from that premise.

At Cove Street, we continued to dig deep and perform basic fundamental research into what companies are doing for a living, how they are valued, and who is running them. Armed with some general sense of the facts on the ground-rather than holding our heads in the macro sky-we worried less about "market timing" and had the confidence to buy new stocks or stick with existing holdings when things were messy. We were also willing to lean the other way when the dust appeared to settle. While this is the same old stuff I have been boring you with for years, clients are clearly benefitting from the Cove Street structure that has been designed and staffed from the bottom-up to properly process information and make investment decisions within a classically-defined value process.

Within the context of 2013 being just another year to apply a time-tested discipline, there are a variety of subtextual questions that come to mind. Have equity markets in general moved so much that it is difficult to find value? Answer: finding cheap stocks is more difficult, but there is still a legacy 2008-like mistrust of markets that a strong 3 weeks of inflows has not fixed and thus there remains an eclectic mix of value available. In reality, the previous question is by far the most important question to be asked and answered. If you research and conclude that you have found value, you should step in before reading the day's paper. (This still works.) Should an investor be worried about giving Cove Street more assets to manage after a strong relative and absolute performance year? Answer: not much more than usual. The difference between Cove Street and an index fund is that we "own differently" than we did a year ago and thus it is incorrect to assume that since what we owned a year ago did fabulously well, the upside from here must be absolutely and relatively inferior. In 2012 our turnover reached what is likely to be an all-time high in small cap, as we stayed disciplined and leaned into what did overly well, and we rotated capital into what hadn't done well (yet) or represented new and potentially fertile value ground. The point is that we will not be riding the same elevator down, although we recognize that 2013 will likely be full of interim bumps given the world in which we live. Please refer back to the fourth paragraph-we will repeat it every year. And dare we remind the fair reader that we do not invest for any one year-but it's not so bad when good things happen sooner rather than later.

It is inherent in the concept of probability is the likelihood that improbable things will happen. The investment world remains locked in a four-year-old debate over the relative force of the headwinds of debt-deleveraging and inconceivably counterproductive fiscal and political policy on one side versus expansive global monetary policy and some sense of cyclical normality on the other. As always, there are numerous, articulate ways to point to the specific things that are wrong with the world, yet stock markets had an excellent year last year and are off to an excellent start this year. Didn't it used to be true that stocks were always to be looked at as leading indicators? And isn't it possible that 2013 will be the beginning of the end of the 30-year bull market in fixed income and thus there will be a tidal wave of money flowing into equities? Is it possible that Ben Bernanke is going to pull a rabbit out of the Fed's hat and truly create a wealth effect that compounds through the world economy through a George Soros-like Theory of Reflexivity? How rarely do you hear, "what if something good happens?" What if the clown-fest in Washington improbably produces something other than a rolling fiscal crisis? What if both Europe and China manage to limp along without political revolution or a currency disaster (ruining yet more vacation plans)? I can vividly recall in 1983, with the Dow at an already improbable 1,200, a First Boston strategist released a report entitled "On a Clear Day You Can See 2,000" and the derision was palpable from the smart-guy segment. Absurdity-the market had already doubled from "The Lost Decade" (the other one) and a never-ending stream of Harvard research was put forth arguing against a reversion to higher prosperity and higher stock prices.

Or does the resilience of stocks mean absolutely nothing, or worse, does it signal the beginning of the lemming trade as the Federal Reserve is finally succeeding at its morally complex game of pushing a realistically conservative mindset toward increasingly poor investment choices? The Fed has already flown the flag of victory in the fixed income world in this regard…why not conquer equities as well? The negative view remains most factually supported at www.hoisingtonmgt.com and it has the resoundingly attractive intellectual backing of a group of smart bond managers/economists who have essentially been long 30-year bonds for 30 years. Yes, another subset of human beings smarter than long-only equity managers has been identified.

Even if one accepts this argument that slow growth and deflation remain the prevailing headwinds and equities are hopelessly over-anticipating future profitability and growth that will not be achieved, it is in fact the opposite scenario that poses the greater risk for an equity investor in the intermediate term-stronger growth and a whiff of inflation that moves the Federal Reserve off its quantitative easing program and suppression of market-led interest rates. While I would argue that the equity world is clearly NOT presently using a risk-free rate of 1.9% with which to discount cash flows (beware the soon to be published Dow 65,000), my guess is that there would be a fair amount of "price consternation" in the period immediately following a change in policy.

And since this is a forward-looking, typical January kind of a piece, we would throw in the possibility that Japanese political change and the new government's attempt to overtly politicize its Central Bank and exchange rate moves currency wars from "unknown-unknown" risk to a "known-unknown" risk for 2013.

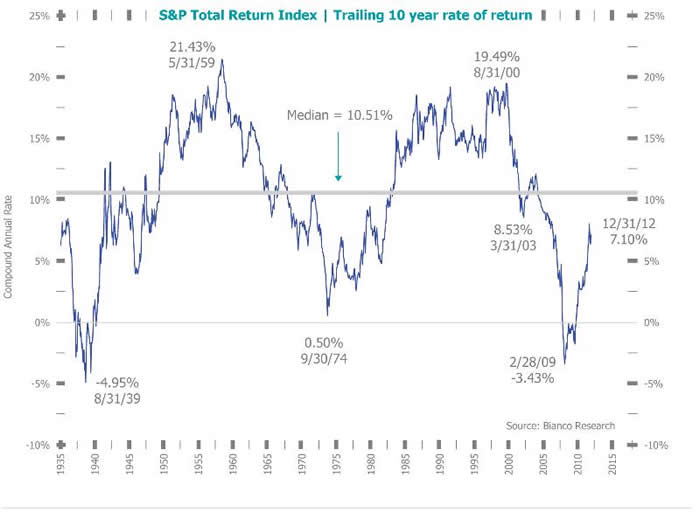

While I am as cognizant of the things wrong in the world as the next middle-aged guy-and I say that with the full moral authority of a California taxpayer-I have spent a lot of time over decades studying the history of the weird mix of valuation, the waxing and waning of capitalism's animal spirits, psychology, and the probability work that constitutes investing. What is clear to me today is that trillions of dollars are leaning the wrong way and equities remain very much under-owned vis-a-vis historical and current alternatives. The "Lost Decade" has been found with a trailing ten-year return for the S&P 500 of 7.1%, a respectable number that will likely be moving higher as the index's return sheds more dismal years. You can just anticipate the resulting headlines and the resulting enthusiasm for equities, justified or not. We have a number of large institutions who have either partially funded us or are "waiting for the dip" to fund us initially or further, and that is likely the number one reason this market isn't settling down. The market hates to be reasonable when you need it to be.

As satirist H.L. Mencken once said "the American people deserve the government they get, and they deserve to get it good and hard." As Senator Barrack Obama said in 2006, "the fact that we are here today to debate raising America's debt limit is a sign of leadership failure. It is a sign that the U.S. government can't pay its own bills. It is a sign that we now depend on ongoing financial assistance from foreign countries to finance our government's reckless fiscal policies."

These are a Few of My Favorite Things for 2013:

- The return of the FICA tax rate to 6.2%;

- A 4.6% increase in the top marginal tax rate to 39.6%;

- A phase-out of itemized deductions (mortgage interest expense, various state taxes-income, property and sales-and charitable gifts) for high-earners;

- A phase-out and elimination of personal exemptions for high-earners;

- An increase in the tax rate to 20% for capital gains and dividends for high-earners;

- A 3.8% surtax on capital gains, dividends and other investment-type incomes for high-earners;

- A 0.9% surtax added to the Medicare tax for high-earners;

- A 2.3% excise tax on medical device manufacturers;

- California Prop 30 hiked marginal income tax rates retroactive to 1/1/12, adding another $12 billion tax increase for 2012-13, with the impact falling almost all in 2013;

- Current committed Federal spending cuts: ZERO.

© Cove Street Capital