The end of money and the new normality

Financial discipline is collapsing and with it, trust in the value of money. Many heavyweight thinkers in America, such as Nobel laureate Paul Krugman have suggested that a solution to avoid national debt ceilings imposed by Congress would be to mint a trillion dollar platinum coin. Meanwhile, heavyweights close to policy makers in Britain and Japan have been musing whether their central banks should write-off the mountains of government bonds they have bought recently. Although each has a low probability of happening, they demonstrate the increasingly surreal nature of policy debates; and that politicians of every hue have abandoned any vestigial attempts to tackle the fundamental weaknesses in their own budgets and other structural deficits, or to reduce national indebtedness. For the foreseeable future, every effort will be made to ensure that a widespread credit bubble is carefully engineered whatever the consequences. The next proof will be a fudge concocted by Congress to avoid the "looming debt ceiling crisis"; similar to the eleventh hour deal in December as Congress histrionically evaded the self-imposed "fiscal cliff".

The new normality is a post-fiat money system. After WWII, exchange rates were fixed to the dollar backed by gold tradable between central banks, because floating rates were seen as one cause of the Great Depression. That system collapsed in 1971. Floating rates and fiat money (unbacked paper) followed, but the value of paper money was still underwritten by future tax receipts or government surpluses. This structure too has collapsed. The new normality is to maintain and increase structural deficits, deliberately debasing every leading currency. The purpose is to reduce the real cost of government debt to a fraction of its current value. This is to be assisted by ultra low interest rates, below the rate of inflation rate and which it is hoped will rise significantly. This last trend reverses three decades of trying to lower inflation because trust in money was evaporating. Thus investment has entered a wholly new era. The long-term effects cannot be foreseen but it is hard to believe it ends well. Yet understandably investors are looking forward at most a handful of years.

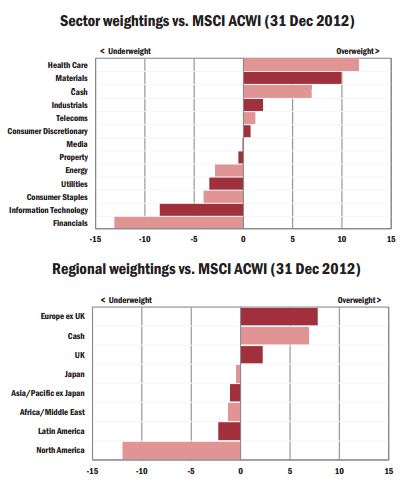

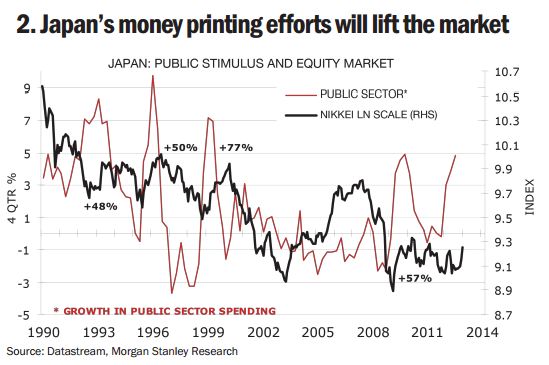

Both individual and institutional investors have been quick to recognise these changes and the corresponding consequences. In America they have increased markedly their commitment to equities, domestic and international whilst reducing cash in their money market accounts. Equity market volumes in other countries - again such as Japan and the UK - have soared. In the former, this change has been dramatic because the new PM Mr. Shinzo Abe wants to reverse the grinding deflation of the last 20 years and join "the West" in a borrow, spend and inflate spree irrespective of longer-term consequences (chart 2, p.4). The major beneficiaries are clear; equities, both for their yields and the potential for real capital gains, stores of value such as bullion and other real assets such as farmland. The risks in bond markets however have soared.

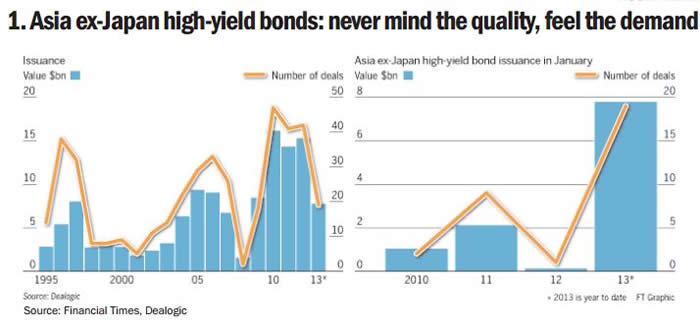

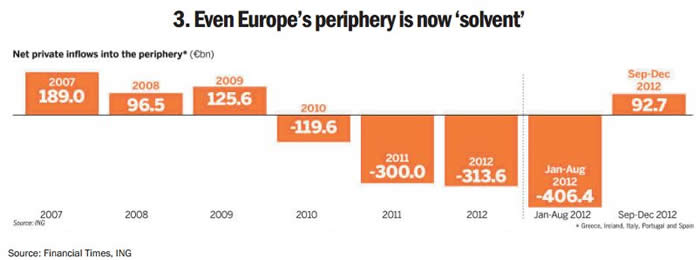

In commencing the man-made destruction of the real value of money thus debt, the risks of financial meltdown so evident in early 2012 have much reduced. The huge money outflows from Europe's periphery have reversed (chart 3, p.4). Sovereign bond yields have tumbled, so although still structurally broke, governments can now issue even more debt without the prerequisite of international support. At the company level too there is a dramatic change. Europe's financial groups, viewed as lepers a year ago, issued more dollar denominated bonds in January alone than the whole of 2012. In emerging markets, companies have been quick to tap into the hunt for any yield, however low or risky. Even before the month of January has ended, the value of high yield bond (junk) issuance in Asia exJapan was nearly $8 billion – more than the previous three years combined (chart 1. P4).

Monetary purists may weep at these bubbles intentionally created by governments, but spendthrift policies are popular. True, the rapid increase in debt as a percentage of GDP in the developed world is failing to achieve the desired economic effect; for every dollar borrowed the universal result is growth worth less than 50 cents. A really bad investment. But it is growth and even better, seemingly cost free. Nor is it helping growth in company profits in many sectors because consumers remain cautious, higher employment stubbornly elusive. Yet equity indices have responded heroically throughout December and January, floating upwards on the ever higher tide of free money. Valuations are at best neutral. Yet despite markets at five year highs, significant falls or a major de-rating carry low probabilities because these policies will continue to provide massive liquidity support. Other support also arises because in many developed countries, the amount of equity paper in issue has actually been contracting; and because pension funds, banks and insurance companies are so bloated with government and corporate bonds that an increase in exposure to equities is a certainty.

Anomalies in valuations are becoming profound and commonplace: equities with sustainable yields better than their corporate bonds; enormous quantities of cash in many companies with no home save to buy other companies through takeover, to pay out more in dividends or to buy back their own shares, thus shrinking supply further. This balance sheet strength has not been seen since the 1950s, an economic Stone Age from which a prolonged bull market developed. Last year many pundits announced the death of equities. It never happened. The Cult of the Equity is returning at an awesome speed.

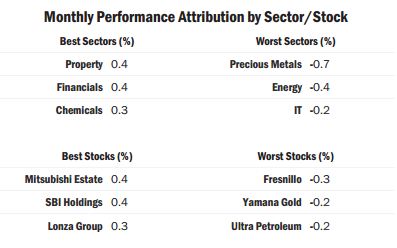

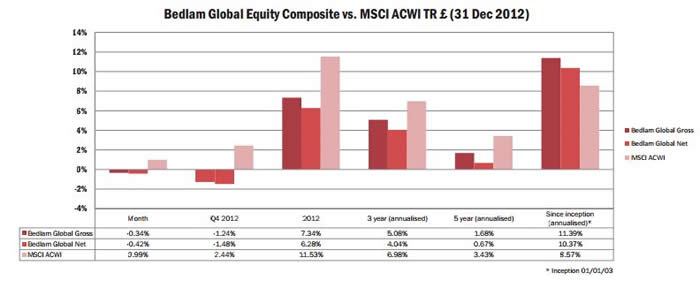

The major "Santa Claus" rally at the end of December was provoked by the realisation that the fiscal cliff was a chimera. The mythical beast hurt performance because of the portfolio's underexposure to sufficient cyclical financials. Whilst disappointing that it did not keep pace better, the more so given the its positioning for a rebound in other cyclical assets following earlier sales in increasingly overpriced defensive areas such as consumer staples, these stocks did not commence their often rocket-like trajectories until the New Year. However, the most important single cause for the lag was the correction in the gold price, during the year a peak to trough fall of 19%; hence three of the five worst performers were the bullion miners Fresnillo, Yamana and Goldcorp. All are well managed but their share prices could not buck the falling gold price. Given the new post-fiat money world, however, good gains in the gold price and related shares seem as inevitable as sunrise in 2013..

There were major gains in Japan. The weighting at the year end was 7% and has subsequently risen further. Especially noticeable were Mitsubishi Estate, one of Tokyo's dominant commercial property companies, and the largest internet broker SBI Holdings. Another financial position which began to soar in January was the Japan Exchange Group, a merger of the Tokyo and Osaka stock exchanges controlling the world's second largest equity market. Barely researched, the undervaluation is blinding both for its potential profitability and relative size. The market cap. of $1.5bn is out of line in comparison with smaller exchanges such as Deutsche Börse ($12.5bn) or Brazil ($13.7bn). After the month-end Sumitomo Real Estate was also purchased because policy changes in Japan make already cheap cyclical stocks very attractive.

The low weighting in technology stocks is working to the portfolio's benefit – witness Apple's collapsing share price. By geography, Japan and Europe ex-UK tied as the best performing regions. In the latter, the widespread "surprise" of a stronger Euro helped but there were also good price gains by Sanofi (pharma) and Syngenta (agri), and even retail companies; Germany's Gerry Weber and Dutch/US Ahold. Two new additions to the portfolio emphasise the search for anomalies. Aimia is a Canadian operator of airline and other loyalty schemes now branching out into America and Europe. Its business model has been particularly successful in periods of weak consumer sentiment. DE Masterblenders was bought back at a lower price than its sale earlier in the year after demerging from Sara Lee. The CEO's track record is excellent. As head of the No. 3 coffee maker globally, he is expected to squeeze better earnings growth and increase market share. Of the outright sales, Germany's Symrise and Henkel had been long held, performed well and easily exceeded their once optimistic price targets. Oriflame in contrast was cut as management continued to struggle to turn around the cosmetics business. Konami's earnings are likely to fall; its competitors have revised guidance sharply lower on weaker demand for computer games franchises.

Bedlam Asset Management plc is authorised and regulated by the Financial Services Authority (212757). Bedlam Funds plc is regulated by the Central Bank of Ireland pursuant to the European Communities (Undertakings for Collective Investment in Transferable Securities) Regulations, 2003 as amended by the European Communities (Undertakings for Collective Investment in Transferable Securities) (Amendment) Regulations, 2003 (the "UCITs Regulations") and is a recognised collective investment scheme for the purposes of section 264 of the United Kingdom Financial Services and Markets Act, 2000. Shares in Bedlam Funds plc may only be sold on the terms of, and pursuant to, its most recent prospectus.

This document is not investment advice or a recommendation to purchase, hold or sell a security. Past performance is not a reliable indicator of future results.

© Bedlam Asset Management