Robert A. Haugen, who passed away this month, found that stocks with lower price fluctuations tend to outperform riskier ones. This article summarizes several hypotheses advanced to explain the persistent low volatility anomaly, reviews the performance of low volatility strategies in up and down markets, and shows how adding a low volatility component can reshape a portfolio’s risk–return profile.

My heart was saddened when I learned that Professor Robert A. Haugen passed away Sunday, January 6, 2013. When given the opportunity to write this issue of Simply Stated, I could not resist calling out to our industry to remember and to pay homage to “the father of low volatility investing.” Bob was a respected scholar who spoke passionately about market inefficiency and the low volatility anomaly over the past half century. Together with Dr. James Heins, he discovered in the late 1960s and early 1970s that, contrary to the prevailing theory, low-risk stocks actually produce higher returns. As a researcher and a product specialist in low volatility strategies, I have often cited their seminal paper,Risk and the Rate of Return on Financial Assets: Some Old Wine in New Bottles (Haugen and Heins, 1975). I have also had the pleasure of speaking and corresponding with Dr. Haugen’s long-time associate, David Fallace, who shares his passion on topics related to low volatility. Dr. Haugen, according to David, cared deeply about educating investors and helping them make better decisions. I am saddened that I won’t have the opportunity to collaborate with Dr. Haugen on my low volatility research, but I know that his research and his passion will remain a significant influence on my work.

What is Low Volatility Investing?

Now let’s review Dr. Haugen’s proposal carefully and understand why he was so dedicated to promoting low volatility investing. Stated simply, low volatility investing means putting your money in stocks with lower price fluctuations. The surprise is that, contrary to the axiom of financial theory that investors are rewarded for bearing risk, those low risk stocks tend to outperform their risky peers. The empirical evidence is clear and has been since the work done by Dr. Haugen in the 1970s. However the investment community only started to pursue low volatility investing in the aftermath of the Global Financial Crisis. MSCI entered the game in April 2008 by creating the MSCI Global Minimum Volatility Indices using an optimization approach. Since April 2011, the S&P 500 Index has launched a series of low volatility indexes, whose constituents are weighted in proportion to the inverse of their realized volatilities. (In other words, the lower the historical volatility, the higher the weight.) PowerShares S&P 500 Low Volatility ETF (SPLV), launched in May of 2011, is now the largest ETF in the category with $3.2 billion.

With institutional investors announcing low volatility mandates and initiating manager searches at an unprecedented pace, investment consultants have joined practitioner researchers in producing white papers and journal articles on the topic.

There are four complementary hypotheses on the low volatility anomaly:

-

·The leverage aversion hypothesis holds that many investors who demand high returns are leverage constrained and choose to increase their expected returns by overallocating to high beta stocks, even if the latter have demonstrably lower Sharpe ratios. (See Black, Scholes, and Jensen, 1972; Frazzini and Pedersen, 2011.)

·The preference-for-gambling hypothesis argues that investors irrationally use high volatility stocks as lotteries; in this framework, investors are implicitly willing to accept lower expected returns by paying a premium to gamble with high volatility stocks. (See Baker, Bradley, and Wurgler , 2011.)

·Another plausible behavioral hypothesis attributes the anomaly to analysts’ optimism about more volatile stocks. Hsu, Kudoh, and Yamada (2012) find that analysts tend to produce high growth forecasts for high-volatility stocks; this can push up their prices and correspondingly reduce future returns.

·Finally, the delegated-agency model provides an explanation for why the low volatility premium could persist even when professional money managers have been aware of the anomaly. The theory contends that most portfolio managers are benchmarked against a common core equity index; they are simply unwilling to buy low volatility stocks, which would significantly increase their tracking error against the benchmark. (See Brennan, Cheng, and Li, 2012; Baker, Bradley, and Wurgler, 2011.)

It is also important to note that the low volatility effect is often related to the value effect, although neither completely subsumes the other. Generally, low volatility stocks also tend to be low price-to-book stocks; this is perhaps not surprising, as we wouldn’t expect growth stocks, like tech stocks to have low volatilities. For readers who have carefully tracked the low volatility literature, much of the pertinent research is related to understanding the low volatility premium in excess of the value premium.

How Does Low Volatility Investing Perform?

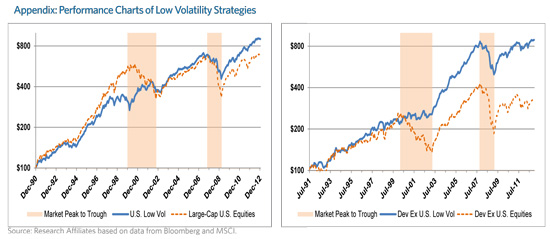

Given how long ago Dr. Haugen started advocating low volatility investing, the low volatility success is not a period-specific accident driven by the Global Financial Crisis of 2008. Let’s review the strategy’s performance over a number of bull and bear markets. The S&P 500 Low Volatility Index and the S&P BMI International Developed Low Volatility Index may serve to represent the low volatility family for this purpose. For comparison, the S&P 500 and the MSCI EAFE Index will represent the corresponding cap-weighted strategies.

Since its inception, the S&P 500 Low Volatility Index has earned an annualized return of 10.2% with a standard deviation of 11.2% (see Panel A ofTable 1). However, career risk probably discourages many professional money managers from offering a low volatility product, regardless of the strategy’s attractive performance over long measurement periods. And, as you can see, it would have proved most unfortunate to implement a low volatility portfolio at the outset of the dot-com bubble in the late 1990s: on an annualized basis, low volatility strategies underperformed their cap-weighted counterparts by large margins—18.5% in the United States and 7.4% in the Developed ex U.S. markets—over the following three years. However, outside of raging bull markets, it is not the case that low volatility portfolios always underperform when prices are rising. In the bull market of 2003–2006, low volatility investments provided higher returns than cap-weighted portfolios with approximately 25% lower risk. During the two most recent market collapses, the bursting of the high tech bubble and the Global Financial Crisis, the low volatility strategies significantly outperformed traditional cap-weighted investing while maintaining the desired low-risk profile.

Some market participants view low volatility investing as a special case of smart beta strategies because part of its outperformance relative to cap-weighted benchmarks comes from moving away from cap-weighting and thereby decoupling prices and portfolio weights. However, the risk-reducing mechanism of these portfolios also involves dropping growth-oriented glamour stocks, whose exclusion tends to ramp up the tracking error tremendously. Over the 138-month period from July 1991 through December 2012, the low volatility portfolios had tracking errors of 9–10% against the core equity indexes, as shown in Panel B. Other mainstream smart beta strategies typically exhibit tracking errors of approximately 3% against core equities. In this context, low volatility investing is unique among smart beta strategies and would mostly appeal to investors who seek to maximize their portfolio’s Sharpe ratio, earning a high return per unit of total portfolio volatility, and who are less concerned about the information ratio, which is dictated by tracking error relative to the benchmark.

What Can Low Volatility Stocks Do For Our Portfolios?

Table 2shows that low volatility portfolios tend to have higher returns, lower risks, and higher Sharpe ratios than traditional large-cap portfolios across different measurement periods. The Sharpe ratios of low volatility strategies dominate those of large-cap core equity indexes over past 5-, 10-, and 20-year timespans in both the United States and the rest of the developed world. The only asset class which displayed a stronger risk-to-return performance is Core Fixed Income, represented by Barclays Capital Aggregate Bond Index, which has benefitted tremendously from the secular decline of rates over the past 30 years. Thus, low volatility investing appears to be an attractive option to anchor the investor’s equity allocation in the long run. In addition, low volatility portfolios have average correlations of 0.4–0.5 with other major asset classes, whereas traditional large-cap equity strategies have average correlations above 0.6. The lower correlation with other asset classes suggests that replacing the traditional cap-weighted equity allocation with a low volatility equity portfolio in your asset mix can improve the overall portfolio diversification.

A comparison of efficient frontiers vividly illustrates the benefit from greater diversification as shown inFigure 1. The efficient frontier including all the “other” asset classes listed in Table 2 is plotted in orange; the portfolio yielding the highest Sharpe ratio (0.82) is marked by an orange dot at the intersection of the orange hyperbola and the dark grey dotted line. Adding the U.S. Low Volatility and Developed ex U.S. Low Volatility strategies causes the efficient frontier to shift upward and to the left, where it appears as the solid blue curve. Investors seeking the highest Sharpe ratio (0.98) would implement the asset mix represented by the blue dot.

Conclusion

Interest in low volatility investment strategies, championed by the late Robert A. Haugen, has increased substantially over the last few years. On a stand-alone basis, low volatility portfolios offer an improved risk-return profile in comparison with traditional cap-weighted core investments. Low volatility investing can be viewed as a smart beta strategy, with the caveat that the reduction in risk is accompanied by a significant increase in tracking error against core equity benchmarks. Finally, adding low volatility strategies is likely to result in greater diversification and a more attractive final portfolio for investors.

Appendix: Performance Charts of Low Volatility Strategies

Baker, Malcolm, Brendan Bradley, and Jeffrey Wurgler. 2011. “Benchmarks as Limits to Arbitrage: Understanding the Low-Volatility Anomaly,”Financial Analysts Journal, vol. 67, no. 1 (January/February):40–54.

Black, Fischer, Myron Scholes, and Michael Jensen. 1972. “The Capital Asset Pricing Model: Some Empirical Tests,” InStudies in the Theory of Capital Markets, New York: Praeger Publishing Co.

Brennan, Michael J., Xiaolong Cheng, and Feifei Li. 2012. “Agency and Institutional Investment,”European Financial Management, vol. 18, no. 1 (January):1–27.

Frazzini, Andrea, and Lasse H. Pedersen. 2011. “Betting Against Beta,” Working Paper (October 9).

Haugen, Robert A., and James Heins. 1975. “Risk and Rate of Return on Financial Assets: Some Old Wine in New Bottles,”Journal of Financial and Quantitative Analysis, vol. 10 no. 5 (December): 775–784.

Hsu, Jason, Hideaki Kudoh, and Toru Yamada. 2012. “When Sell-Side Analysts Meet High-Volatility Stocks: An Alternative Explanation for the Low-Volatility Puzzle,” Working Paper (May 17).

© Research Affiliates

www.researchaffiliates.com

© Research Affiliates

Read more commentaries by Research Affiliates