Expanding Horizons: The Most Difficult Environment for Generating Income in 140 Years

Key Points:

- The current environment is the worst for generating income in 140 years

- Global equities are one of few assets offering at least historical average yields

- Asset returns in the 1951–1981 bond Bear Market suggest significant headwinds for fixed income

- Global dividend equities are cheap and offer compelling yields

- Dividend yield is historically more effective in global markets

than in the U.S. markets

- Global dividend payers offer diversification of income generation

across monetary, fiscal, interest rate, and currency regimes

- Global dividend-paying equities should be an effective agent of

income generation and growth of principal for years to come

Einstein once said, “The measure of intelligence is the ability to change.” The current environment is one in which change is indeed necessary. It is second to none in both the necessity and difficulty of income generation. Since 1871 there has not been a more difficult period for generating yield in investor portfolios.Over the past 140 years a 60% equity /40% fixed income balanced portfolio generated an average yield of 4.4 per-cent. As of the end of 2012, the yield on that portfolio fell to an all-time low of just 2.0 percent (see Figure 1).

It is ironic that yields reach their secular nadir when, according to the Pew Research Center, ten thousandBaby Boomers turn 65 each and everyday until 2030. Presumably, demand for income-producing assets will increase in the coming decades as the baby boomers increasingly draw on their retirement assets.

Given uncertain monetary, fiscal, and tax policies, we argue that the most prudent course of action is a diversifiedapproach to income generation which includes a combination of stocks, bonds, and real assets. Our objective in this commentary is to assess the risks inherent among myriad income-generating options inorder to design a portfolio with a highlevel of current income whose principaland income grow in excess of inflation over time.

Our research leads us to believe that high quality, global, dividend-paying equities often under-allocated in investor portfolios could be the primary agent of income generation and growth of principal in portfolios for years to come.

A Survey of Income-Generating Options

Relative to history the current yields on the spectrum of assets available to the income seeker is shocking(see Fig. 2).Yield is one of few measures of valuation that is comparable across asset classes. Higher yields signal a cheaper valuation, while lower yields indicate an expensive proposition. Clearly, different layers of risk are captured in each asset-specific range of yields over time. But you can get a sense for each asset’s valuation by comparing its current position relative to its historical high, low, and average. You will immediately note that we are charting new lows across the majority of assets. Notably, in July 2012, 10-Year Treasury yields reached their lowest levels ever since 1790!

All assets except dividend-paying equities are trading below their historical average yield for the longest data sets we are able to obtain. Addressing each asset is beyond the scope of this commentary, but we will touch on the highlights.

Lessons from the Previous Bear Market in Bonds

Treasurys are likely nearing the end of their miraculous three decade BullMarket. Long-termTreasurys returned11.3 percent annualized from 1981–2011. However, history tells us that there exists an inverse relationship between the performance of a given asset in bond Bull and Bear Markets (see Table 1). An investor in long-term U.S. Treasury bonds in the 30 years leading up to the September 1981 peak in bond yieldsreceived a 1.8 percent annualized return (before inflation). Prices generally move inversely with yields. Intermediate government bond investors would have fared slightly better at 4.0 percent annualized (before inflation). And for the record, inflation ran at an annualized rate of 4.3 percent from1951 to 1981. During that same period,stocks had an annualized return of 9.8 percent. Stocks significantly outpacedmunicipals, long- and intermediate-termgovernment bonds,highyieldcorporates,Treasury bills, and inflation.

There is even greater significance to these findings in the face of the United States’ current poor fiscal condition. We are often asked how this unprecedented environmentimpacts our analysis of historical asset returns. Interestingly, there is historical precedent. In 1945, the country’s debt-to-GDP ratio ballooned to 121 percent as deficits in excess of 20 percent fueled wartime spending. But by 1981 our debt-to-GDP ratio had declined to 32 percent. In the face of this astonishing recovery, the government ran fiscal surpluses in only eight of those 36 years!

How is this possible? For the most part, we overcame this massive debt via the path of least resistance: inflation. Year-over-year inflation rose from nearly zero percent in the early 1950s to 13.5 percent in 1980. If inflation becomes the chosen path, Table 1 provides a good indication of what asset returns could look like in the face of elevated inflation levels.1

Fixed Income:Caveat Emptor

Most investors are concerned with the next three years, not the next thirty.Across the fixed income classes shownin Figure 2, we argue thatinterest rate risk should be the primary consider-ationfor fixed income assets. Though the Federal Open Market Committeehas announced its intent to continuemonetary stimulus, the impact of price declines—as measured by duration—from even modestly rising interestrates would, in most cases, dwarf any income received on those assets.2 For long-term Treasurys, a one per-cent rise in interest rates would result in an approximate20percent pricedecline, the equivalent of almost sevenyears worth of income at current yields.

The concept of price declines in bonds,though temporary if the bond is held to maturity, brings up a unique but little discussed attribute of bond funds. In bond funds, temporary price declines can become realized if the manager is forced to sell assets to meet redemptions. One could quickly conceive of a scenario where bond fund investors rush to the exits in a rising interest rate environment, resulting in principal losses for the remaining fund shareholders.

Another popular option, municipal bonds, offer tax-exempt income and have performed well the last few years, making them a prime choice among investors. But municipal bonds, despite solid recent returns, should be viewed with scrutiny due to interest rate, credit and political risks. The Barclays Municipal Bond index offers a 2.0 percent yield with duration of 6.2—indicating an approximate 6.2 percent price decline for each one percent rise in interest rates.3

Municipal bonds are not only subject to interest rate risks, but also tectonic shifts are occurring in this asset class. A recent report published by the Federal Reserve Bank of New York argues that defaults in the $3.7 trillion municipal bond market are signifi-cantly understated and are, in fact, 36 times greater than reported by the rating agencies.4 Further, historical defaults in the space may no longer serve as an appropriate yardstick by which to predict future defaults.

Prior to the credit crisis, large, highly-rated insurers like MBIA,Ambac, or AIG underwrote insurance policies for the benefit of bond holders in theevent of default. With the demise of the municipal insurers, that backstop exists in reduced form. In-depth research on the underlying credit quality of the 54,000+ municipal issuers is now the name of the game. For these reasons, one could argue that—in addition to risks associatedwith rising interest rates—the rate of municipal defaults could also increase from its historical average.

Finally, the tax-exempt feature of municipal bond interest has come under fire repeatedly in Washington. Three times since 2011, the idea of reducing the exemption has been advanced under the auspice that high income earners receive the lion’s share of tax savings. This exemption is what generally drives lower yields in tax-exempt versus taxable bonds. Should the exemption be reduced, yields on the impacted municipal bonds would need to rise to compensate investors for the increased tax burden.As discussed earlier, rising yield resultsin price declines.

Though fixed income surely has a placein a diversified asset allocation scheme,exposure to fixed incomeshould, in our opinion, berelegated to shorter duration instruments with a keen eye to the aforementioned other risks.

Real Assets: Not the DiversifierYou Thought

Real assets are physical or tangible assets like real estate, precious metals, or oil. The oft-stated benefits of including real assets in a portfolio are centered on inflation protection and their low correlations with other assets. Because we are focusing on income generation, the scope of our discussion is limited primarily to publicly traded REITs and MLPs. Both assets are excellent options to generate additional yield but, as is always the case, there are risk/return benefits to consider.

Historically, REITs and MLPs provide suitably low correlations to the S&P 500 (0.58 and 0.38, respectively), which substantiates the claim ofdiversification.5But upon closer inspection,correlations between these two asset classes and equities (asproxied by the S&P 500) have been rising steadily since the early 2000s. As of December 2012, the trailing three-year correlation between the FTSE NAREIT Index and the S&P 500 stood at 0.86. For theAlerianMLP Index, that same correlation was 0.70. In short, correlations are cyclical and can change significantly over time.

The credit crisis serves as a ready explanation for this convergence. A key feature of REITs and MLPs are the legal vehicles under which they operate. REITs and MLPs are legal structures created by legislation which allows investors to access the asset classes in a tax-preferred manner.

A condition of their existence is the requirement that 90 percent of their income be distributed. The greatest implications from this structure: (1) REITs and MLPs are inextricably tied to credit markets to finance growth and (2) the inflation protection historically provided is at least in part attributable to the availability of easy credit to finance growth in distributions. Should credit markets dry up, these assets will suffer alongside their equity counterparts. MLP and REIT investors learned this lesson all too well when these assets registered double digit monthly declines during the credit crisis in late 2008 and early 2009.

Another nuance that should becare-fully considered in portfolio construction:real assets are implicitly heavily concentrated in one industry. The totalmarket capitalization of MLPs is 89 percent attributable to either energy or natural resources.6

Naturally, Real Estate Investment Trustsfocus on real estate. Though sector concentration is not necessarily a bad thing, investors must be aware that theconcentration exists and understand the associated risks during times of stress.

Global Dividends:Unloved and Under Appreciated

Let us shift our attention to the asset class that has received little attention in the quest for yield. When dividendsare mentioned, large, stable U.S.corporations with mature businesses and ample cash flows often come to mind.Pedestrian yields across asset classespreviously discussed have propelledmassive amounts of investment dollarsinto theseU.S.dividend-paying stocks.

However, our research indicates that the opportunity lies inglobaldividendpayers for the following three reasons:

- Global companies provide access to growth at substantial discounts andhigher yields than U.S. companies.

- Dividend yield has historically been a superior factor for stock selection in global markets.

- A global portfolio provides diversification of income generation across monetary, currency, and interest rate regimes.

Global Growth & Yield on Sale

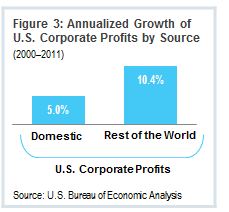

For some time now, U.S. companies have been deriving a substantial portion of revenues from foreignsources. In 2011, 46 percent of S&P 500 revenues were generated from outside the United States.7Corporate profits paint an even more dramatic picture of this trend. The share of U.S. corporate profits generated outside the U.S. has grown at twice the rate of those from domestic sources and represents 33 percent of U.S. corporateprofit growth since 2000(see Fig. 3).8

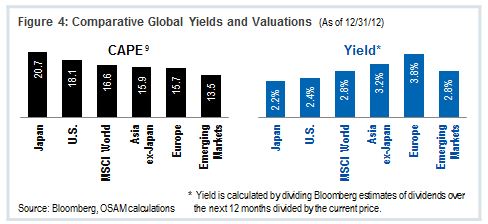

If U.S. corporations have implicitly bet on foreign markets, perhapsU.S. investors should follow suit and cut out the middle man. The opportunity cost of arbitrarily restricting an incomeportfolio toU.S.companies isimmensewhen viewed through the prism of valuation. A cursory review ofvaluations across regions in Figure 4 reveals that, ex-Japan, the rest of the world is trading at considerable discounts to the United States. Based on the Cyclically Adjusted P/ERatio (CAPE), regions such as Europe are trading at a 14 percent discount while offering a 60 percent greater indicated dividend yield.9

Certainly, other regions in the world are experiencing challenges at the sovereign level which must be considered. But in investing, crisis andopportunityare often inextricably linked.Case inpoint, Verizon is a stalwartU.S.Telecom with ample cash flow, ready accessto capital markets, and a strongdividend yield. Should an investor avoid Verizon because the U.S. has a high debt-to-GDP ratio? Probably not. This would beanalagous to avoiding high-quality foreign companies because their countries of domicile are in poor fiscal condition. When put into context, arbitrarilyrestricting a company like Verizon due to perceived sovereign risks seems as ridiculous as avoiding quality foreign stocks. This is exactlywhy we focuson selectingcompanies—notcountries.

Dividend Yield is More Effective in Global Markets

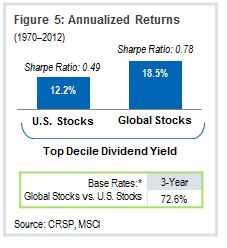

Our research has shown that dividend yield is an excellent factor for stock selection in the United States, but an exemplary one in the global markets. From 1970 to 2012, an investment in the topdecile of dividend-yielding stocks in the global markets would have outperformed their high-yielding U.S. counterparts by 6.3 percent per year (annualized)—a nearly 52 percent greater average annualized return—with a better risk-adjusted return as determined by the Sharpe Ratio.*And in the 481 rolling three-year periods since 1970, global dividend yield outperformed U.S. dividend yield 73 percent of the time.

Global Dividends ProvideDiversification of Income Generation

When we further refine our research on the efficacy of dividend yield in global markets to seek well priced, high-yielding firms with solid balance sheets and ample cash flows, the result is a portfolio diversified across geographies, currencies, interest rate regimes, and monetary policies.

An Enhanced Dividend®portfolio, forexample, which seeks companies withsimilar characteristics, currently represents approximately 15currencies and 20 unique economies (both developed and emerging). As shownin the white paper “Stocks, Bonds, andthe Efficacy of Global Dividends”,10different global regions exhibit a range of yields at any given time. These economies operate independently of the U.S. government and Federal Reserve, which is important because reliance on any individual monetary authority introduces a number of risks into portfolios—not the least of which is that the goals of the authority maybe contrary to that of the investor.

Bill Gross refers to this in what he terms “financial repression,” which is the idea that manipulation of interest rates and asset prices by U.S. monetaryauthorities is to the detriment of savers—that is, the same baby boomers discussed earlier.

An oftenunderlooked consideration is that of corporate dividend policy itself. From 1990 to 2000 the percentage of dividend-paying companies in the United States was nearly cut in half.10Dividends, as opposed to share buy-backs, are generally more prevalent in non-U.S. markets, thus making the global landscape a broaderopportunity set from which to seek high quality, cheap dividend payers. While this nuance is a perfect example of a long-term structural difference in dividend payers, the Fiscal Cliff serves as an example of short-term considerations. As of December 17, 2012 (according to Bloomberg), 113 U.S. companies had chosen to issue special dividends in anticipation of potential tax rate increases on dividends. These companiesare altering long-term corporate policy due to a short-term circumstance. Aglobal investor would have mitigated exposure to this arbitrarydeviation—whereas aU.S.-onlyinvestorwould have been beholden to it.

Accessing yield via multiple regions can help ease short- and long-term risks associated with incomegenerationby diversifying exposure to multiplecurrencies, interest rate regimes, monetary policies, and corporate dividend policy.

Allocation Decisions as Seen Through the Lens of History

Finally, we evaluate an incomeapproach from 1977 to 2012 in order todemonstrate the efficacy of global dividend payers and their relevance in investor portfolios. Our objectives are(1) high current income, (2) growth of income and principal above inflation, and (3) reasonable levels of volatility.

We use the basic 60/40 balanced portfolio as a starting point and then augment the allocations to reflect diversified exposures to stocks, bonds, and real assets. Given our assessment that bonds could face headwinds in the coming years, we include fixed income instruments with shorter durations (the Barclays Aggregate) and those that are less sensitive to increases in interest rates(high yield debt). REITs are given anallocation in the portfolio in order todiversify the sources of income and for a degree of inflation protection. Equities make up the largest allocationin the portfolio. Table 2 shows historical levels of yield, total return, risk-adjusted return, and consistencyfor two portfolios. In Table 2a we showreturns and characteristics for fiveindividual assets. In Table 2b we showthe results of combining the fixedincome and real asset optionswith either U.S.-only high yield equitiesor global high yield equities. Adding in global dividend payers improves the return of the U.S.-only incomeapproach by 3.5 percent, with a 30 percent boost in risk-adjusted return.

A diversified exposure to global high dividend equities, fixed income, and real assets (REITs) provides an attractive mix of yield, total return,manageable volatility, and risk-adjustedreturn superior to any of the individual assets. The consistency ofdelivering positive returns is exceptional.Of the 397 rolling three-year periods tested from1977 to 2012, the portfolio produceda positive annualized return in391 periods for a 98 percent base rate* (fees and transaction costs are not considered).

* Notes: High Yield Debt = Barclays U.S. HY Corp. Index; REITs = FTSE NAREIT All Equity REIT Index; U.S.-only = top decile dividend yield U.S. Large Stocks; Global = top decile dividend yield MSCI All Stocks.Base ratesare a batting average for how often a strategy beats its benchmark over certain rolling time periods.

Source:Global Financial Data, Morningstar EnCorr, Compustat, MSCI, OSAM calculations

CONCLUSIONS

We believe that the most prudent course of action—given the uncertain monetary, fiscal, and long-term tax environment—is a diversified approach to income generation. We assessed a number of assets that, except for high-yielding and global equities, are all trading substantially below their long-term average yields. Historical precedent suggests that rising yields in combination with elevated inflation levels can significantly reduce return expectations for a number of these assets. In inflationary environments, equities have historically outperformed other assets while delivering inflation-beating returns.

Given that domestic corporations are sourcing growth from a globalopportunityset, we advocate that investors do the same. Valuations of internationalequities are discounted, while yields are offered at tremendous premiums compared to the United States. Our research leads us to believe that high-quality, global, dividend-paying equities—often under-allocated in investor portfolios—will be an effective agent of income generation and growth of principal in investor portfolios for years to come.

1 For a study that shows how equities typically outperform bonds see “Inflation and the U.S. Bond and Stock Markets” (http://www.osam.com/commentary.aspx).

2 Duration is defined as the percentage change in a bond’s price for each one percent shift in interest rates. Prices and rates move in opposite directions.

3 Barclays Capital (as of 12/7/2012)

4Appleson, Parsons, and Haughwout, “The Untold Story of Municipal Bond Defaults” 8/15/2012

5 Morningstar EnCorr, FTSE NAREIT All Equity Index 1972–2012;Alerian MLP Index 1996–2012

6National Association of Publicly Traded Partnerships, 8/1/12

7S&P Dow Jones Indices, “S&P 500® 2011: Global Sales”

8 U.S. Bureau of Economic Analysis, OSAM calculations

9The cyclically-adjusted P/E ratio (CAPE) is calculated by

dividing the current price by the average of earnings-per-share over the trailing 60 months.

10See “Stocks, Bonds, and the Efficacy of Global Dividends”(http://www.osam.com/research.aspx)

* TheSharpe Ratiois a measure of annual return in excess of a 5 percent risk-free rate divided by the annualized standard deviation of return.Base ratesare a batting average for how often a strategy beats its benchmark over certain rolling time periods.

Past performance is no guarantee of future results.Please see important information below.

General Legal Disclosure/Disclaimer andBacktestedResults

The material contained herein is intended as a general market commentary. Opinions expressed herein are solely those of O’Shaughnessy Asset Management, LLC and may differ from those of your broker or investment firm.It should not be assumed that your account holdings correspond directly to any comparative indices. Individual accounts may experience greater dispersion than the composite level dispersion (which is an asset weighted standard deviation of the accounts in the composite for the full measurement period). This is due a variety of factors, including but not limited to, the fresh start investment approach that OSAM employs and the fact that each account has its own customized re-balance frequency. Over time, dispersion should stabilize and track more closely to the composite level dispersion. Gross of fee performance computations are reflected prior to OSAM’s investment advisory fee (as described in OSAM’s written disclosure statement), the application of which will have the effect of decreasing the composite performance results (for example: an advisory fee of 1% compounded over a 10-year period would reduce a 10% return to an 8.9% annual return). Portfolios are managed to a target weight of 3% cash. Account information has been compiled by OSAM derived from information provided by the portfolio account systems maintained by the account custodian(s), and has not been independently verified. In calculating historical asset class performance, OSAM has relied upon information provided by the account custodian or other sources which OSAM believes to be reliable. OSAM maintains information supporting the performance results in accordance with regulatory requirements. Please remember that different types of investments involve varying degrees of risk, that past performance is no guarantee of future results, and there can be no assurance that any specific investment or investment strategy (including the investments purchased and/or investment strategies devised and/or implemented by OSAM) will be either suitable or profitable for a prospective client’s portfolio. OSAM is a registered investment adviser with the SEC and a copy of our current written disclosure statement discussing our advisory services and fees continues to remain available for your review upon request.

Hypothetical performance results shown on the preceding pages arebacktested and do not represent the performance of any account managed by OSAM, but were achieved by means of the retroactive application of each of the previously referenced models, certain aspects of which may have been designed with the benefit of hindsight.

The hypothetical backtested performance does not represent the results of actual trading using client assets nor decision-making during the period and does not and is not intended to indicate the past performance or future performance of any account or investment strategy managed by OSAM. If actual accounts had been managed throughout the period, ongoing research might have resulted in changes to the strategy which might have altered returns. The performance of any account or investment strategy managed by OSAM will differ from the hypotheticalbacktested performance results for each factor shown herein for a number of reasons, including without limitation the following:

Although OSAM may consider from time to time one or more of the factors noted herein in managing any account, it may not consider all or any of such factors. OSAM may (and will) from time to time consider factors in addition to those noted herein in managing any account.

OSAM may rebalance an account more frequently or less frequently than annually and at times other than presented herein.

OSAM may from time to time manage an account by using non-quantitative, subjective investment management methodologies in conjunction with the application of factors.

- The hypothetical backtested performance results assume full investment, whereas an account managed by OSAM may have a positive cash position upon rebalance. Had the hypotheticalbacktested performance results included a positive cash position, the results would have been different and generally would have been lower.

- The hypothetical backtested performance results for each factor do not reflect any transaction costs of buying and selling securities, investment management fees (including without limitation management fees and performance fees), custody and other costs, or taxes – all of which would be incurred by an investor in any account managed by OSAM. If such costs and fees were reflected, the hypothetical backtested performance results would be lower.

- The hypothetical performance does not reflect the reinvestment of dividends and distributionstherefrom, interest, capital gains and withholding taxes.

- Accounts managed by OSAM are subject to additions and redemptions of assets under management, which may positively or negatively affect performance depending generally upon the timing of such events in relation to the market’s direction.

- Simulated returns may be dependent on the market and economic conditions that existed during the period. Future market or economic conditions can adversely affect the returns.

Notes:All factor portfolios cited in this are calculated using a compositing methodology. Monthly portfolios are created with a 12-month holding period based on a single characteristic within a universe of stocks. The 12 monthly portfolios are then combined together to create the composite portfolio.

Universes:The All Stocks Universe includes all stock included in theCompustat Database listed on a U.S. exchange with a market value greater than $200mm and a price per share greater than $1. The Large Stocks Universe consists of all the stocks in the All Stocks Universe where the market capitalization is greater than the universe average. The MSCI World Index is a free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets. The index includes securities from 24 countries but excludes stocks from emerging and frontier economies making it less worldwide than the name suggests. This index is net of withholding taxes.

Characteristics The dividend yield is a gross indicated yield. There is no guarantee that the rate of dividend payment will continue and the income derived is subject to taxes and expenses which will impact the actual yield experience of each investor.

© O'Shaughnessy Asset Management