- We expect the ongoing recovery in new housing construction from unsustainably low levels to contribute roughly ½ percentage point to real GDP growth this year, and emphasize the risks to the upside of this forecast.

- Imminent employment growth in housing-related industries will provide an important channel for secondary “multiplier” effects of the housing recovery. We expect job gains in these sectors soon to average 25,000 per month.

- Applying recent house price increases to the entire stock of owner-occupied housing overstates their likely wealth effect on consumer spending. This response will likely be seen in full force only for the small cohort of home owners with greater home equity than they anticipated at the time that they made the purchase.

The recovery in housing demand remains skewed toward rental units, with most of the supply response to date coming in the multi-family sector. Stabilization in the preference for homeownership should underpin a continued gradual rise in home sales and single- family construction, but the primary contribution of the housing sector recovery to the broader economy will be in the value of new construction. Housing- related industries will soon begin to add substantially to headcounts, with monthly gains of 25,000 expected soon. Yet we caution against extrapolating the wealth effect of recent house price increases: they are likely to affect only the small cohort of home owners with greater home equity than they anticipated at the time that they made the purchase.

Housing recovery: preference to own still muted

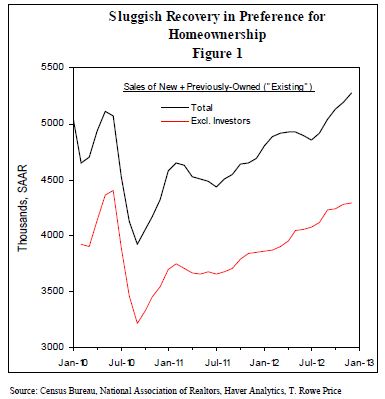

Despite declines in December, home sales continue to trend broadly, if only gradually higher: a 1% dip following gains in four of the previous five months left home re-sales1 13% above June’s pace and 12.8% ahead of December 2012. In a similar vein, the surprising 7.3% drop in sales of newly-built homes, to a 369,000 annual rate, was offset by back-month revisions totaling 28,000 (annual rate).

Investors accounted for 21% of December’s re-sales, but a gradual upward trend – restrained by still-tight mortgage credit conditions – is evident even when these transactions are excluded (Figure 1). We expect further modest gains in home sales in the months ahead: home builder sentiment remains elevated, and mortgage applications for home purchase, though volatile, are peeking beyond the upper bound of the range that has prevailed since late 2010.2

House price wealth effect will take time to accrue

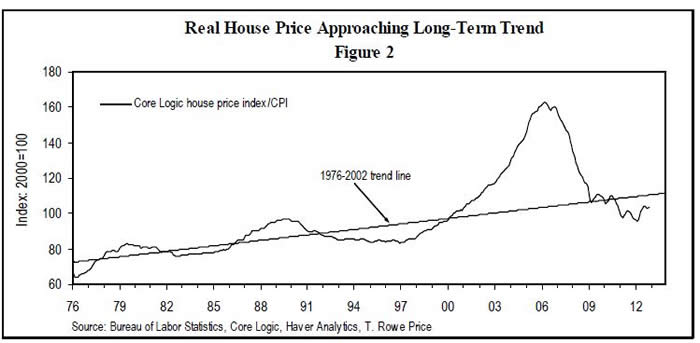

The faster pace of housing transactions has underpinned a turn toward renewed growth in prices. Median prices of new and existing homes sold are 13.9% and 11.5% higher than a year ago, respectively, and a repeat sales index compiled by Core Logic is up 7.4% in the 12 months to November. Gains of that magnitude are possible over the next 1-2 years the real house price returns to its 1976-2002 trend line over that time frame (Figure 2, page 2).3

The simplest reckoning of the wealth effect from recent house price increases calculates a $1.1 trillion increase value of household real estate over the four quarters of 2012 and asserts roughly a $50 billion fillip to consumer spending (based on a 5% marginal propensity to consume out of housing wealth). This overstates the likely near-term impact on consumer spending, in our view. We judge that the wealth effect of rising home values on consumer spending only gains full force homeowners’ equity is higher than it was expected to have been at a given point in time. Home prices may be substantially higher than they were a year ago, but they are

- roughly aligned with their long-term (1976-2002) trend, suggesting that current homeowners who purchased their homes during that pre-bubble interval are not yet observing an unexpected increment of housing wealth to backstop additional consumption;

- below levels prevailing during the 2004-2008 period, suggesting that current homeowners who bought their homes at that time are in negative equity positions, with no housing wealth to extract;

- higher, to varying degrees, for most of those who bought homes beginning in January 2009, the first month in which the Core Logic house price was below its current level (net an unrealized capital gain).

In this framework, only the third cohort is likely to have experienced, in general, an unexpected appreciation in the value of their houses since the date of purchase. The 17 million homes sold over that period is just 20% of the current stock of owner-occupied housing, and the associated wealth effects are far smaller than the rough calculation presented above. Indeed, we estimate an aggregate increase in housing wealth of $87 billion for homes purchased beginning in January 2009.4 If current trends5 continue, housing wealth in the cohort that purchased homes since January 2009 would rise by a further $222 billion in 2013, a two-year total ($308b) roughly 1/10 of that obtained by applying recent price increases to the universe of homeowners.

1 Better known as “existing” home sales.

2 A 2.5% rise in the January 18 week lifted the Mortgage Bankers Association index of mortgage applications for home purchase to its highest level since May 2010, with the expiration of government incentives for first-time homebuyers.

3 After returning to the pre-bubble trend, real house prices would presumably grown in line with the 1.5% annual rate observed over the 1976-2002 period.

4 We estimate the aggregate increase in housing wealth as by adding the changes in value of housing purchased during each month beginning in January 2009. The date-of-purchase value of housing is estimated as the product of the number and median price of homes sold (less those purchased by investors) during the reference month. The current value of housing purchased in an historical reference month is obtained by applying to the date-of-purchase value the growth in the Core Logic house price index from the reference month through November 2012 (the latest data available).

5 For 2013: A 7% increase in the Core Logic house price index, 10% increases in sales and median prices of new and existing homes.

Issued in the USA by T. Rowe Price Associates, Inc., 100 East Pratt Street, Baltimore, MD, 21202, which is regulated by the U.S. Securities and Exchange Commission. The material is not intended to be a solicitation for any product or service not available to U.S. investors, including the T. Rowe Price Funds SICAV, and may be distributed only to institutional investors.

Issued in Japan by T. Rowe Price International Ltd, Tokyo Branch (“TRPILTB”) (KLFB Registration No. 445 (Financial Instruments Service Provider), JSIAA Membership No. 011-01162), located at NBF Hibiya Building 20F, 1-7, Uchisaiwai-cho 1-chome, Chiyoda-ku, Tokyo 100-0011. This material is intended for use by professional investors only and may not be disseminated without the prior approval of TRPILTB.

Issued in Canada by T. Rowe Price (Canada), Inc. T. Rowe Price (Canada), Inc. enters into written delegation agreements with affiliates to provide investment management services. T. Rowe Price (Canada), Inc. is not registered to provide investment management business in all Canadian provinces. Our investment management services are only available to select clients in those provinces where we are able to provide such services. This material is intended for use by accredited investors only.

Issued in Australia by T. Rowe Price International Ltd (“TRPIL”) (ABN 84 104 852 191), Level 50, Governor Phillip Tower, 1 Farrer Place, Suite 50B, Sydney, NSW 2000, Australia. TRPIL is exempt from the requirement to hold an Australian Financial Services license (“AFSL”) in respect of the financial services it provides in Australia. TRPIL is authorised and regulated by the UK Financial Services Authority (the “FSA”) under UK laws, which differ from Australian laws. This material is not intended for use by Retail Clients, as defined by the FSA, or as defined in the Corporations Act (Australia), as appropriate.

Issued in New Zealand by T. Rowe Price International Ltd (“TRPIL”). TRPIL is authorised and regulated by the UK Financial Services Authority under UK laws, which differ from New Zealand laws. This material is intended only for use by persons who are not members of the public, by virtue of section 3(2)(a)(ii) of the Securities Act 1978 and is not intended for public distribution nor as a solicitation for investments from members of the public. This material may not be redistributed without prior written consent from TRPIL.

Issued in the Dubai International Financial Centre by T. Rowe Price International Ltd ("TRPIL"), 60 Queen Victoria Street, London EC4N 4TZ, which is authorised and regulated by the UK Financial Services Authority (the "FSA"). This material is communicated on behalf of TRPIL by the TRPIL Representative Office which is regulated by the Dubai Financial Services Authority ("DFSA") as a Representative Office. This material is not intended for use by Retail Clients, as defined by the FSA and DFSA. Retail Clients should not act upon information contained within this material.

Issued in Hong Kong by T. Rowe Price Hong Kong Limited (“TRPHK”), 21/F, Jardine House,1 Connaught Place, Central, Hong Kong, a Hong Kong limited company regulated by the Securities & Futures Commission. This material is intended for use by professional investors only and may not be redistributed without the prior approval of TRPHK.

Issued outside of the USA, Japan, Canada, Australia, New Zealand, DIFC and Hong Kong by T. Rowe Price International Ltd, 60 Queen Victoria Street, London EC4N 4TZ, which is authorised and regulated by the UK Financial Services Authority (the “FSA”). This material is not intended for use by Retail Clients, as defined by the FSA.

This material is provided for informational purposes only and is not intended to be a solicitation for any T. Rowe Price products or services. Recipients are advised that T. Rowe Price shall not offer any products or services without an appropriate license or exemption from such license in the relevant jurisdictions. This material may not be redistributed without prior written consent from T. Rowe Price. The contents of this material have not been reviewed by any regulatory authority in any jurisdiction where this presentation is being made or by any other regulatory authority. This material does not constitute investment advice and should not be exclusively relied upon. Investors will need to consider their own circumstances before making an investment decision.

T. Rowe Price, Invest With Confidence and the Bighorn Sheep logo is a registered trademark of T. Rowe Price Group, Inc. in the United States, European Union, Australia, Canada, Japan, and other countries. This material was produced in the United Kingdom.

The views contained herein are as of January25, 2013, and may have changed since that time.

Copyright © 2013 by T. Rowe Price Associates, Inc. All rights reserved.