This week’s commentary is a slight departure from our standard format. It’s been a few weeks since we mentioned the fiscal cliff, sequestration and the like. This is due to our collective saturation and the perspective of so many that the problem was solved. Well, we want to provide a reminder or two and throw a few thoughts at you to kick around. We conclude with a quick look at Maine and Illinois.

2013 started with us being told there was a solution to the “fiscal cliff.” Revenues will increase by virtue of a tax increase (or two) on the wealthy (sorry Phil Michelson) and as a result of the payroll tax holiday not being continued (that was not a tax increase but the expiration of the Bush tax cuts was a tax increase – darn semantics!)). The pundits relaxed, the news channels dismantled their fiscal cliff countdown clocks and we were told “problem solved.” The inauguration is passed and it’s time for a reality check: automatic spending cuts go into effect soon and the debt ceiling needs to be solved and not perpetually kicked down the road (although one can argue the Republicans seeming sense of cooperation was simply a clever maneuver to have the Senate finally put forth a budget after 4 years and address spending). There is talk of tax and entitlement reform – let’s see if anyone has the gumption to attack the big issues.

Why the reminder? While we are arguably in a recovery that is, according to some, picking up steam, we need to be cognizant of what some really smart people are saying and what one might expect from tax receipts – at all levels. Let’s start with the fourth quarter of 2012. Tax receipts will be up. Why? Many companies paid bonuses before the end of 2012 or declared special dividends to beat the tax increases. The media was able to provide a sense of what was going on as these practices related to public companies. The real question is how prevalent were these practices across private companies and how will 2013 income and tax receipts be impacted? Time will tell.

We can’t help but think 2012 fourth quarter tax receipts may inject an element of complacency or a view that the economy is stronger than may be the case. The real kicker for tax receipts may come a year from now when 2013 tax receipts are collected. Absent wage increases (which the data does not support), tax receipts for 2013 may be less than budgeted. Will those budgeted tax receipts be there?

Next up is the impact of increased taxes and the expiration of the payroll tax holiday. Let’s assume, for the moment that the rich people don’t change their spending habits. What about the rest of us? According to people much smarter than yours truly, the projection for GDP growth for 2013 is 2-3%. At the recent Barron’s Roundtable, Scott Black of Delphi Management suggested that the expiration of the 2% tax holiday alone can actually cause GDP to decline by .7%! Again, take a look at those budgets and the assumptions contained therein.

Speaking of budgets….

New York released its budget and seems all is good – no new taxes, increased spending, Sandy relief and pensions are highly funded. Oh, did you notice that little provision that allows municipalities to forego their pension contribution – the “Stable Rate Pension Contribution Option.” As the New York Times Editorial page put it:

Mr. Cuomo’s Low-Buzz Budget, Published: January 24, 2013

One of the more questionable aspects of the budget is a provision labeled the “Stable Rate Pension Contribution Option.” Innocent as that sounds, the provision would give local communities the freedom to stretch out their pension obligations to the state by paying less now, and almost certainly more later on. The mayor of Syracuse, Stephanie Miner, describes this as “kicking the can down the road.”

State Comptroller Thomas DiNapoli would have to approve this idea, a decision he should consider carefully. Communities like Syracuse pay pension costs into the state’s $150 billion pension fund, and lower contributions from these communities could make the state plan more vulnerable.

Besides, most of these cities need more help than this revision to the pension plan. Many are struggling with the 2 percent property tax cap Mr. Cuomo and the Legislature imposed in 2011, and there has been little relief from state mandates. Nor does this budget offer these communities anything new in the way of unrestricted state assistance.

Now, perhaps NY thinks it can afford this now given it is almost 100% funded but one has to worry what this looks like in 5 years. A little discipline now just might help preserve the “stellar status” of NY’s pension plans.

Speaking of Pensions….

If only Illinois had passed legislation perhaps Moody’s wouldn’t have downgraded them. We think there may be a bit more to that story. While the below Muni Index review focuses on Maine, our trend for Illinois has spiked from 13 in August of this year to 38 this month. Also, stories like the one in Friday’s WSJ cause us some concern. The cover story discussed how some State Pension Funds are leaning more and more on hedge funds to goose their earnings. It wasn’t too long ago there was quite a bit of noise around where and how pension funds are invested. While it is arguably prudent for long-term diversified portfolios to allocate a portion of their assets to unregulated higher-risk investments such as hedge funds, our concern is that portfolio managers may be tempted to over allocate to these areas in order to improve results and their related funded ratios. Not an unreasonable concern when we have seen several pensions bet (and lose) on rate bets through the issuance of pension bonds.

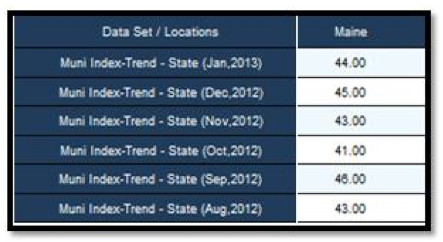

Last week, following Maine’s downgrade, we provided our clients and trial users the below snapshot on Maine. Check out where Illinois is on the map.

While we generally don’t follow-on a ratings action, we thought you might find the below of interest. Earlier [Tuesday], Fitch downgraded the State of Maine.

We call your attention to the DIVER Muni Index, Trend for the States, which looks at the relative rank (1 being the best) for the one year period for unemployment, tax revenue per cpaita, housing prices and personal income per cpaita. Below are the results since August 2012.

Source: DIVER Analytics, Data Access Module.

And January’s Muni Index Trend Map.

Source: DIVER Analytics, Map Module.

We took this a step further for you. Below is some interesting information regarding Maine’s counties and where they rank on our Muni Index, County Level (point in time and trend). The Rank is out of 3,113 Counties that are included in the Index. The below can be accomplished using the Data Access module or the Map module.

|

County |

Rank |

Percentile |

|

Androscoggin |

2336 |

24.96 |

|

Aroostook |

3002 |

3.57 |

|

Cumberland |

1895 |

39.13 |

|

Franklin |

2789 |

10.41 |

|

Hancock |

2972 |

4.53 |

|

Kennebec |

2884 |

7.36 |

|

Knox |

2726 |

12.43 |

|

Lincoln |

2716 |

12.75 |

|

Oxford |

2888 |

7.23 |

|

Penobscot |

3024 |

2.86 |

|

Piscataquis |

3027 |

2.76 |

|

Sagadahoc |

1923 |

38.23 |

|

Somerset |

2299 |

26.15 |

|

Waldo |

2724 |

12.50 |

|

Washington |

3016 |

3.12 |

|

York |

2721 |

12.59 |

We encourage our readers to look at a variety of factors that influence the fiscal realties for our State and local governments. We certainly are not second guessing Fitch or Moody’s (indeed, the above supports Fitch’s perspective) but encouraging our readers and clients to look at more than a single data point to reach your conclusions. While the OCC’s regulations are not applicable to many of our readers, their directive and our message is – look beyond ratings.

Data Updated in DIVER this past week includes:

- Debt Outstanding, as % of Personal Income, and Per Capita (CAFR), 2012, State

- ARC as % of General Fund Revenue and Expenses, State, 2012

- Funded Ratio, Pension Plan, State, 2012

- Labor Underutilization, State, 2012 Q4

- Percent of ARC Paid, State, 2012

- Weekly Initial and Continued Jobless Claims, State, 1/12/2012

- Drought Intensity, County, 1/22/2013

- Union Membership, 2012, State

- Coincident Index Change, December 2012, State

Wishing our readers a great week and we look forward to seeing some of you in Texas at the Bond Buyer conference.

Gregg L. Bienstock

CEO& Co-Founder, Lumesis, Inc.

![]()

A suite of powerful analytical and visualization tools serving Credit Analysts, Portfolio Managers and Risk Managers. Access over 225 datasets from more than 50 sources and generate detailed credit analysis by geography or CUSIP for your holdings.

![]()

Comprehensive information delivery and compliance solution serving Financial Advisor networks. Improve customer satisfaction, while protecting your firm. A simple to generate CUSIP-driven report delivers email ready content for your client and adherence to MSRB Rules and Compliance requirements.

![]()

Delivers CUISP-driven, dynamic, sector based reports that aggregate key information and data within seconds. Available for all 1.4M+ municipal bonds and displays the most current data available in the market including terms and features, EMMA disclosure filings, price and yield, call provisions, sector driven key economic and demographic data and links to primary news sources from every issuer community.

© Lumesis