Opine Less, Think More

A Worthwhile 2013 Resolution, Which I May Honor… Or Not

The festive season is also one for socializing and once more, at dinners and cocktails, I was struck by the plethora of opinions and the paucity of thought. Everyone has an opinion on the Arab Spring (Summer, Fall?), the U.S. Fiscal Cliff, tax systems everywhere, oppression of women in India or corruption in China, to mention but a few favorites.

Of course, most of these opinions are self-centered, one-sided, formulated in black and white, and totally ignorant of the multidimensional complexity of most political, social and economic problems. Yet, already in the 19th century, political economist Frederic Bastiat explained why this simplistic view of the world is dangerous (Selected Essays On Political Economy – 1848):

In the economic sphere an act, a habit, an institution, a law produces not only one effect, but a series of effects. Of these effects, the first alone is immediate; it appears simultaneously with its cause; it is seen. The other effects emerge only subsequently; they are not seen; we are fortunate if we foresee them.There is only one difference between a bad economist and a good one: the bad economist confines himself to the visible effect; the good economist takes into account both the effect that can be seen and those effects that must be foreseen.

There is no doubt that we are living in an increasingly complex world. Not necessarily because the world itself has become more intricate, but because we are swamped by an incessant flow of news coming from the farthest corners of an increasingly global world and delivered by the media indiscriminately, without regard to significance. How to cope with this “data onslaught” is one challenge for the investor: we can try to gain some altitude or distance, to discern only what stands out, or we can try to simplify the problem. Sometimes, the problem becomes so complicated that the solution becomes simple: “We’re surrounded. That simplifies the problem!” (Lt. General Chesty Puller).

On The Lookout For The Next Black Swan

Most economists and market strategists failed to anticipate the Great Recession and financial crisis of 2007-2010. So, naturally, they now are vying to predict the next “Black Swan”. Of course, this is paradoxical since the term popularized by Nassim Taleb is meant to describe a hard-to-predict and rare event that is beyond the realm of normal expectations.

With regards to Black Swans, however, I tend to subscribe to the definition of Prof. Jeffrey Frankel, of Harvard:

“In my view, ‘Black Swan’ should refer to… an event that is considered virtually impossible by those whose frame of reference is limited in time and geographical area, but not by those who consider other countries and other decades or centuries.” (A Flock of Black Swans – Project Syndicate – 8/20/2012)

The problem is that knowing that a Black Swan is possible, or even increasingly probable, is not much help in timing investment decisions. The possibility must remain “in the back of our minds”, hopefully to sharpen our alertness to otherwise innocuous “straws-in-the-wind”.

For example, Charles Gave recently pointed, again, to the danger posed by “overconfident and over-educated control-engineers” at the world central banks. These economists’ misguided manipulation of the price of money (exchange and interest rates) is distorting the notion of risk, he argues. (Gavekal, 12/14/2012)

Gave further quotes science philosopher Karl Popper, also a reference for Black Swan author Taleb: “In an economic system, if the goal of the authorities is to reduce some particular risks, then the sum of all these suppressed risks will reappear one day through a massive increase in the systemic risk…” Gave suggests that in a world of “suppressed volatility”, as today, the way to reduce risk is to invest in assets that have been sold by many precisely because of their volatility.

Another, not entirely unrelated area where trouble with unknown ramifications may be brewing is that of interest rates. In their efforts to fight the recessionary effects of de-leveraging on the world economies, central bankers have ushered an era of “suppressed interest rates” not experienced in the United States since the 1940s.

The term “suppressed interest rates” refers to the setting of interest rates by central banks below the rate of inflation – amounting to a negative real cost for borrowers but also a negative real return for savers. This is what can currently be observed on inflation-indexed U.S. Treasury bonds, for example. Such a distortion of incentives has the potential to become very painful when it is reversed.

Among the countries vulnerable to rising interest rates is the United States, where much of the government borrowing is relatively short-term and would therefore need to be refinanced at higher rates fairly quickly, thus aggravating the country’s fiscal conundrum since interest payments on the national debt already are a significant component of America’s budget expenditures.

Perhaps even more dangerous (though with a local twist) is the situation of Japan, with a very high ratio of debt to G.D.P. and a fast-aging population. Against the expectations of many, Japan has so far weathered well its enormous government debt because much of that debt has been purchased and held by insular Japanese savers willing to accept zero returns for the presumed safety of their government credit. But, with the aging of the population now accelerating rapidly, savers are being transformed into retired dis-savers and the domestic market for placing Japanese Government Bonds will soon be shrinking fast. When Japan is forced to attract foreign savings to finance and service its debt, it probably will have to pay a multiple of its current interest rates, throwing the government finances into a serious fiscal crisis.

As Black Swan events, these potential crises are fairly predictable, but it is hard to ascertain what will trigger them and when or how exactly they will unfold. For example, the rise of interest rates may come from an acceleration of inflation or, simply, from a growing savers’ indigestion with government paper. But either way, as economist Herbert Stein once said: “If something cannot go on forever, it will stop”.

An Encouragement To Do Little

Besides being aware of the possibility of Black Swans and historical episodes with which they may “rhyme”, I have found the work of Professors Ken Rogoff and Carmen Reinhart (“This Time Is Different”, published in 2009, as well as preceding and subsequent papers) to be a very useful roadmap during the recent financial crisis and its aftermath.

In a more recent paper (October), the two professors describe the slow and halting growth of the U.S. economy since 2009 as “quite typical of post-war systemic financial crises around the world”. Indeed, beyond the political theatrics and the media hype, the aftermath of the crisis has developed pretty much as announced in their opus.

After reading their original work I had armed myself with a great deal of patience, to wait for the economic recovery and financial de-leveraging to slowly (and haltingly) unfold. So, my main effort since then has been to refrain from over-activity … and over-writing, since I can only write so many reports entitled: “Ditto”.

While I was doing little, the world stock markets recovered on schedule. In the United States, the Dow Jones Average and the Standard & Poor’s 500 are within shooting distance of their 2007, pre-crisis highs, while the Apple-heavy NASDAQ is back above 3,000.

Germany’s DAX index and the United Kingdom’s FTSE 100 are not far from their previous highs either. France’s CAC 40, on the other hand, has been held back by confusing and counterproductive policy initiatives, and remains nearly 40% below its pre-crisis peak, barely edging out crisis-ridden Italy and Spain (Greece, despite nearly doubling since June, remains almost 80% below its 2007 high).

Standing out are Tokyo and Shanghai, which both remain around 40% below their 2007 highs, while a number of industrializing countries, including India and Brazil have almost recovered to their previous peaks. On the other hand, so has Pakistan, which makes it hard to draw definitive conclusions about opportunity, risk and investor wisdom.

By and large, however, most stock markets have recovered relatively strongly from their most recent lows.

Lasting Improvement Or Not, Economic Bears Are Getting Tired

It is probably fair to say that no lasting, comprehensive solution has been agreed upon to solve the world economies’ structural problems (government deficits/debts, and welfare/demographic time bombs). But, with a mixture of “kicking the can down the road”, some help from government stimuli and the global spread of loose monetary policies, the cyclical (shorter-term) outlooks have improved. One thing is clear: after a typical lag behind financial markets, economies, too, are giving signs of recovering more or less on schedule.

While Europe has not solved all its sovereign credit and banking problems, some visibility seems to have been restored for businesses, possibly allowing for a cyclical bottoming out process to start in 2013. Of course, I believe the region’s prospects would be greatly improved if France’s president Hollande borrowed a page from the late Francois Mitterrand’s script.

After starting his first term with hardline socialist programs (nationalizations, wealth tax, etc.), Mr. Mitterrand saw the light and made a spectacular economic U-turn in 1983, proudly proclaiming in a 1984 interview to the magazine Challenge, “The French are beginning to understand that it is the enterprise that creates wealth, which determines our standard of living and our place in the world hierarchy”.

Unfortunately, Mr. Hollande does not seem to have learned from his mentor’s experience … yet.

In the United States, indicators are pointing up for housing and other depressed industries. Despite the expected brake effect from higher taxes on economic activity in 2013, a number of economists expect the hit to be initially offset by recovering housing activity and the release of pent-up demand suppressed during the recession – including investment demand. This could allow for slow GDP growth to continue during the first half of the year. In any case, I observe that many of the formerly most pessimistic forecasters are, as we say in France, putting some water in their wine.

In China, the days of 10%-11% GDP growth are probably over. As we had expected, the country never had a recession in recent years, but it is clear that the new norm for economic growth going forward is closer to 8%. The reason is mathematical.

Private consumption has been growing at around 13% per annum for much of the past decade. But while what Andy Rothman, of CLSA, has described as the world’s best consumption story may continue at this fast pace for a number of years, it is unlikely to accelerate much. Wages and salaries already have grown at very high rates and the propensity to save will remain high as long as health care and pension schemes remain embryonic.

Meanwhile, one of the reasons that the ratio of consumption to GDP (now 35%-40%) has remained relatively low is that total investment has been growing even faster than consumption, at a 25% annual rate for the last nine years. But today’s percentage of investment to total GDP seems unsustainable over the long term. After the nearly-bubbly booms in housing and infrastructure construction, homebuilding is likely to settle at a lower cruising speed, with a new focus on low-cost (social) housing. Meanwhile, the bulk of the very large infrastructure investments having now been completed, regional projects will have to sustain heavy construction. Thus, while continuing to grow, overall investment will likely decline as a component of GDP.

Note that China’s controversial export machine, while extraordinary, contributes much less to GDP on a “net trade” basis than is generally realized, since much of what is exported must first be imported, in the form of materials and components. Thus, exports and imports tend to move up and down in unison.

The growth rate of consumption, perhaps aided by the announced granting of more city-residency permits (with associated privileges) to migrant workers, will remain high and become more visible within the total economy but, overall, the growth rate of GDP will probably stabilize closer to an 8% average.

In Japan, Premier Abe, with the apparent cooperation of the central bank, has announced steps to boost G.D.P. growth, weaken the overvalued yen to help exports, and end price deflation (i.e. engineer some inflation). For once, it appears that the government is serious in delivering on its promises, so that various estimates now put Japan’s growth in 2013 at around 2%.

Altogether, with the Eurozone growing around 0% but emerging economies following the leads of the United States, China and Japan, a fairly complacent consensus has settled around a year of moderate growth for the world economy in 2013.

But, before we open the Champagne…

Economy And Market: The Odd Couple

A July, 2012 client letter from BNY Mellon Asset management, reminds us that “as counterintuitive as it might seem, data suggest that high [economic] growth rates do not necessarily correlate with the highest long-term stock market returns”. This hardly is a new discovery, as evidenced by two quotes cited by the author:

“If you spend 13 minutes a year trying to predict the economy, you have wasted 10 minutes.” (Legendary fund manager Peter Lynch)

“The stock market has called nine out of the last five recessions.” (Nobel Prize and economics professor Paul A. Samuelson)

And the letter concludes: “Over longer time periods, the statistical correlation between the quarterly change of real U.S. GDP and the S&P 500 is virtually zero. The correlations between the EuroStoxx 50 and the Eurozone GDP since 1999 and between the DAX and the German GDP since 1991 are similarly small”.

There is a large body of studies pointing to the futility of trying to make investment decisions based on predictions of economic growth. Among the latest is one by the Vanguard group, which studied equities’ returns going back to 1926, looking at the predictive power of important economic variables. (The Economy and Stocks: A big Disconnect – New York Times, 12/15/ 2012) The conclusion was that: “none of these factors… come remotely close to forecasting accurately how stocks will perform in the coming year”. In fact, even over a 10-year time horizon, only price-to-earnings ratios had a meaningful predictive quality (emphasis mine).

These studies do not make the economy irrelevant to investing but once more, if you wish to make money, it will be time better spent to concentrate on valuation.

The Secular Story On Valuation

Ben Graham, the father of security analysis, pointed out that, in the short term, the stock market is a voting machine (rather than a weighing machine). He meant that crowd psychology, much more than fundamental value, is the main determinant of the market behavior over shorter periods.

More recently, in a January 2013 letter to Oaktree clients, Howard Marks noted that, within a cycle, securities prices rise and fall much more than profits, and concluded: “Over the years, I’ve become convinced that fluctuations in investor attitudes toward risk contribute more to major market movements than anything else.”

Over longer periods, a number of market students, notably including Crestmont Research’s Ed Easterling (Probable Outcomes – Cypress House – 2011) and Millennium Wave Investments’ John Mauldin (Endgame – John Wiley & Sons - 2011) have pointed out that, while there are no usefully discernible patterns in stock prices themselves, secular moves in the stock market can be identified by looking at the market P/E (price-to-earnings) ratio.

When I write about secular moves, I do not mean mere ups and downs associated (or not) with the business cycle. In post-war history, for example, the team at research house Strategas identifies only two secular bull markets:

• 1942 to 1961, when the S&P 500 P/E ratio rose from below 10 to the mid-20s over 19 years;

• 1979 to 2001, when the P/E ratio rose from about 6 to the high-20s in 22 years.

In between, there was an 18-year secular bear market, from 1961 to 1979, when the index’s P/E ratio declined from the mid-20s to 6. In their view, we are now in another secular bear market that started in 2001 with a P/E of nearly 30, and has so far declined to the high teens.

Unfortunately, P/E ratios are not a tool for forecasting stock market prices precisely. On the other hand, investors that have used current P/E ratios to anticipate likely stock market returns over the following 7, 10 or 20 years seem to have had a good batting average over time.

This is because a significant portion of the gains during bull markets and of the losses during bear markets is due to changes in P/E ratios, rather than to changes in the less-cyclical earnings. So, buying when P/E ratios are low and selling when they are high simply follows one of the most basic tenets of stock market investing: “Buy low, Sell high”.

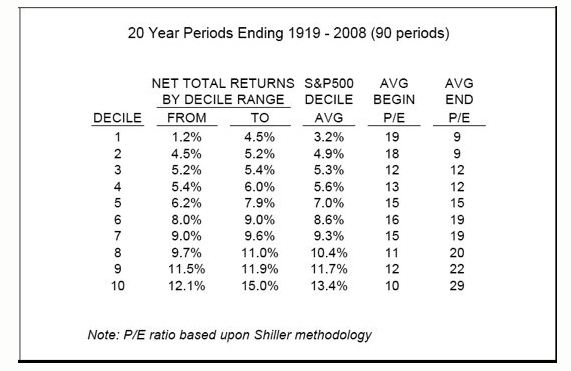

The following table from Crestmont Research, which I have used before, confirms that in general the higher the P/E ratio, the lower the subsequent 20-year average return, and vice-versa.

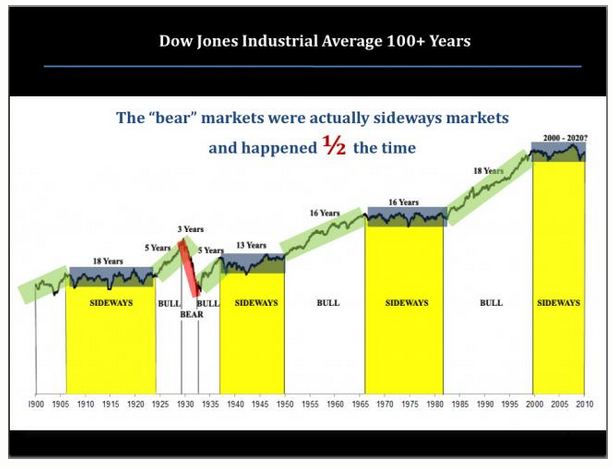

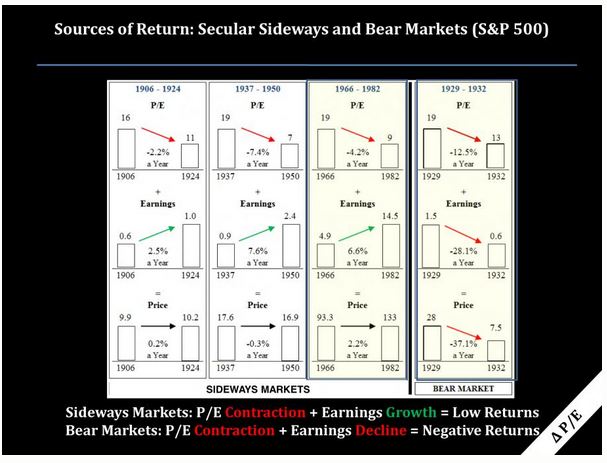

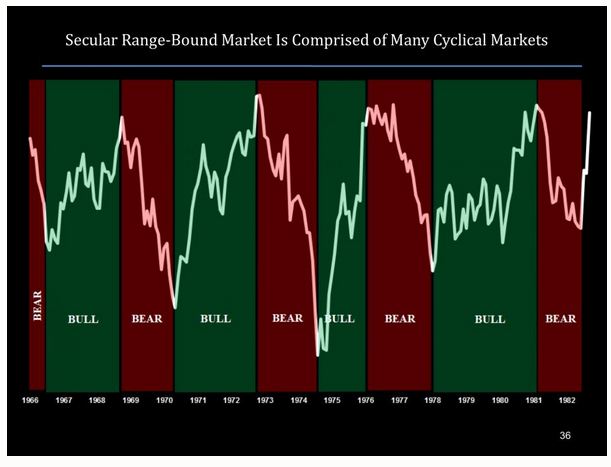

Secular bear markets, when looked at in a longer time frame, do not always fit the popular image of crashes or catastrophic events. As pointed by ContrarianEdge’s Vitaliy Katsenelson (The Little Book of Sideways markets – Wiley – 2011), most bear markets since 1900 actually were sideways markets.

In most such instances, the lack of progress in stock prices was the net result of earnings gains, offset by an erosion of P/E ratios, as illustrated in a recent presentation by Katsenelson.

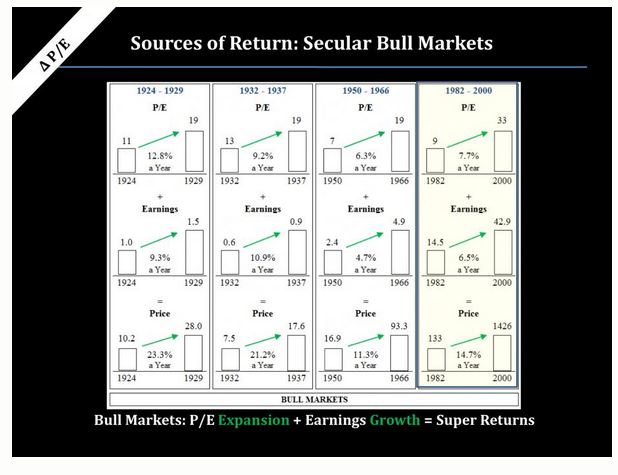

Secular bull markets, in contrast, benefited from both earnings gains and P/E ratio expansion.

Katsenelson also reminds us that secular bear or sideways markets may encompass very significant intermediate bull and bear moves. Having personally experienced most of the ups and downs depicted in the chart below (presumably derived from the Dow Jones Industrial Average), I can testify that this was no time to fall asleep at the wheel.

For Every Risk, There Should Be A Reward

One of my road maps, the post-financial-crisis scenario of Rogoff and Reinhart, calls for more of the long restoration and consolidation of the economies that we have been experiencing. The other one, the interpretation of long market cycles based on valuations rather than simply price, says that we are only in the middle of a secular bear cycle. Combining these two approaches, I don’t get the impression that a major bull market is about to take off.

However, as I have repeatedly argued in these letters, the important question to answer, for an investor, is not “Will the market go up or down?” but “How much money do I stand to make or to lose if I am right or wrong?”

Today, I am tempted to assume that the stock markets will continue to oscillate within broad bands, without breaking out to major new highs or new lows. But if I am wrong and the U.S. stock market, for example, soars to major new highs, how far could it go ?

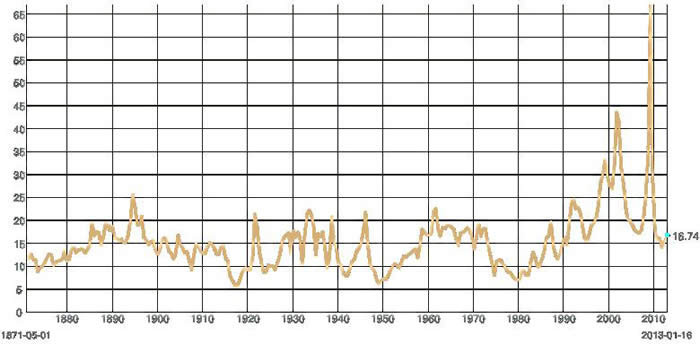

The P/E ratio on the S&P 500 Index reached a historical peak in the mid-30s towards the end of the “tech” bubble, in 1999. Many experts, from Ben Graham to Yale Professor Robert Shiller, argue in favor of calculating the price/earnings ratio using a 7-10 year moving average of earnings to smooth cyclical and other extraneous influences. But I find the choice of averaging periods just as subjective and distorting of reality as the annual figure. Therefore, I am simply ignoring abnormally high P/E readings due to depressed earnings, such as during the most recent crisis. Thus, from a high in the 30s, the “market” P/E is now back to just below 17.

Many analysts take comfort from the fact that 17 is often viewed as the historical average of the S&P 500 P/E, implying that we have returned to normal. But, looking at the chart below, it appears to me that, if the bubbles of the 2000s are ignored, 17 is closer to the higher band of the historical range. In other words, close to average, but not cheap.

S&P 500 Price-Earnings Ratio on Trailing Twelve Months Earnings

Source:multpl.com

In any case, Mauldin and Easterling have pointed out that, historically, the market P/E has almost never dropped from a high to its historical mean without going through this mean to a new low before rising again to a high.

What Can Valuations Do For An Encore?

Today’s P/E ratio has benefited from a “perfect storm” of favorable factors, which means that many factors making the current level possible are likely to deteriorate at some point in the future.

U.S. corporate profit margins, which determine the E in P/E, have reached historical records as a result of massive cost-cutting (including labor) and some restraint on capacity-related investments (as opposed to productivity-related). According to Strategas drawing data from S&P Compustat, current S&P 500 sales are 32% above their 2008 level, while its “Cost of Goods Sold”, is down 19%. With income taxes up only 14%, Net Income is 71% higher than in 2008.

There is only so much that management can cut out of costs, and future earnings gains will depend more heavily on sales growth than on further margin improvement. In that respect, Strategas is not overly optimistic, noting that S&P sales have remained very lukewarm since the 2009 low.

Today’s fairly rich market valuation also takes support in the idea that, in the United States, for example, the expected return on common stocks competes with the risk-free yield on Treasury bills. From this perspective, the lower the level of interest rates, the higher the level of price/earnings ratios. But, sooner or later, “suppressed” interest rates will make room for more realistic interest rates, making it hard for price/earnings ratios to rise from current levels.

Finally, a number of economists have pointed out that domestic margins of U.S. corporations have not been quite as excessive as their overall margins appear to be. This is because the contribution of foreign profits has been rising. But, at a time when we are seeing more and more foreign corporations moving operations to the United States to take advantage of lower costs (often related to the much cheaper energy input), I have some questions about a sustained future contribution of foreign profits to the S&P’s total earnings.

Conclusion

Institutional investors, after being severely under-invested as a group for four years, reportedly are “capitulating”, i.e. are aggressively moving back into stocks. This, from a tactical/contrarian viewpoint, naturally makes me lean toward caution. I feel this way all the more since, as I explained earlier, I fail to envision significant stock market gains from current valuations.

It seems credible that, before a decisive upside breakout above their 2007 highs, stock markets might have to continue experiencing more backing and filling. But, as Katsenelson’s chart of the sideways market from the mid-1960s to the early 1982s illustrates, during such periods, cyclical (as opposed to secular) opportunities do become available. From memory, it was possible to make money during that long sideways market, by concentrating on valuation and selective stock picking.

I recently read a headline proclaiming “The End of Stock Picking”. After a few years of macro-driven stock markets, I take this as an encouraging sign that individual stock selection is about to make a comeback.

François Sicart (in Mexico)

January 17, 2013

DISCLOSURE:This article reflects the views of the author as of the date or dates cited and may change at any time. The information should not be construed as investment advice. No representation is made concerning the accuracy of cited data, nor is there any guarantee that any projection, forecast or opinion will be realized.

We periodically reprint or quote extensively from articles published by other sources. When we do, we provide appropriate source information, including hyperlinks to websites we borrowed from. The quotes and material that we reproduce are selected because, in our view, they provide an interesting, provocative or enlightening perspective on current events and the topic discussed. Their reproduction in no way implies that we endorse any part of the material or investment recommendations published.

Author:

Francois Sicart

© Tocqueville Asset Management