- Housing is off the floor, but faces ceilings

- The cost of housing could be a source of increased inflation

- January’s FOMC meeting should not break any new ground

Twenty years ago, mortgage rates were falling fast. I suggested to my wife that we take advantage by refinancing the loan we had taken out to purchase our starter home just a few years before. She had a different idea…why not use the same monthly payment to pay for a bigger house? Our family was growing, we needed to begin thinking about schools, and (this was her hook) wouldn’t I like a bigger kitchen?

The next few weeks were a blur to me, but I do vaguely recall a climactic occasion with lawyers around where I was asked to sign a lot of papers and a rather large check for the down payment. What followed were several months of weekly visits to furniture and home improvement stores, with the attendant damage to our finances.

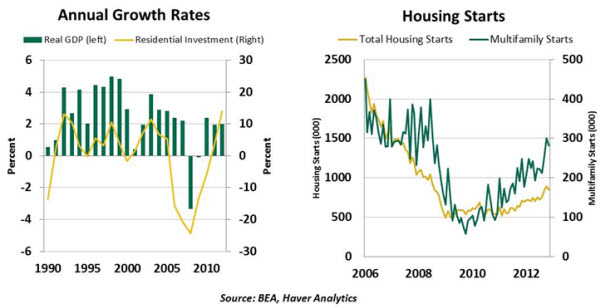

Needless to say, I became acutely and personally aware during that interval of the economic stimulus generated by housing. The industry’s rise drove the US economy powerfully for many years…until it precipitated the Great Recession. The slow recovery of American housing has been one reason that the current expansion has lacked the momentum of its predecessors.

However, 2012 will likely go down as one of the strongest years of growth that the housing sector has ever had. Granted, readings on starts and sales began the year from a very low base; but many forecasters have been surprised at the pace of recent gains.

The demand for lodging is somewhat independent of economic performance. “Household formation” is increased by population growth and the graduation of children from their parents’ dwellings to their own, while mortality and family consolidation subtract from it. Since the Great Recession began in 2007, more than 3 million households have been formed.

Many of these new households, though, are not great candidates for a new home purchase. Raising a sufficient down payment is not as easy as it once was, and lending standards are much tighter than they were six years ago. This has precipitated a shift toward renting, which can be seen in an accelerated pace of apartment construction and upward pressure on rents.

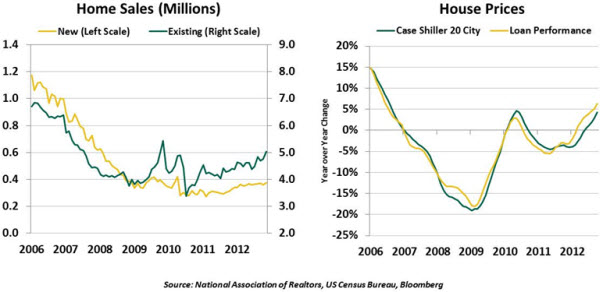

Some of the new demand has been satisfied by the conversion of single-family homes to rental units. In many markets, investors have been purchasing blocks of property and turning them out for lease. This activity has helped absorb the backlog of property for sale, and helped to create modest increases in home prices.

The improvement in prices is fairly widespread; eighteen of the top twenty markets tracked by Case Shiller have shown increases over the last year, and markets like San Francisco (which I had the good fortune to visit this week) are very strong.

When property values are uncertain, lenders will typically seek more protection in the form of higher down payments, additional mortgage insurance, and heightened credit standards. Now that home prices are improving, prospective financiers have a clearer line of sight.

Clarity is also replacing uncertainty in the area of mortgage regulation. The Consumer Financial Protection Bureau (CFPB) was created by the Dodd Frank Act and charged with reforming standards for loan origination. After extensive study, the CFPB recently announced a broad set of new guidelines that govern:

- The responsibility of lenders to establish a borrower’s ability to repay

- Compensation for loan originators, which prohibits tying compensation to loan terms

- Screening standards for originators

It will take time for lenders to adapt to the new rules, but at least they are established. From here, underwriters are expecting updated guidelines on the sales of loans into the secondary market.

Meanwhile, major mortgage underwriters are settling liability claims from those who purchased loans that subsequently defaulted. These claims had absorbed a lot of management attention and a lot of capital that might otherwise be employed in extending credit.

Little by little then, some of the hurdles that hindered the housing recovery are falling. Unfortunately, some rather larger barriers remain. The most major of them are the nation’s high unemployment rate and debt levels which still need to be worked down.

Additionally, at the end of the third quarter 22% of American homes were still underwater, meaning that values remained below mortgage obligations. These residents are very limited in their ability to consider a new home purchase; many may join the ranks of renters before long.

Secondary markets for mortgage loans are still not functioning normally. The Federal Reserve has been purchasing a very large fraction of new origination of “conventional” mortgage-backed securities, making it difficult to gauge broader investor demand. The market for “nonconforming” loans (which are of a much larger size) is still essentially closed.

Finally, the Federal Agencies which support the American mortgage market remain deeply troubled. Freddie Mac and Fannie Mae are still in search of a revised mission. And the Federal Housing Administration, which had been the sole agent offering home loans to those with more marginal credit scores and down payments, is reevaluating its standards amid growing losses.

Recent developments have put a floor under single-family housing, but the sector still faces a ceiling formed by weakened household balance sheets and the uncertain structure of the mortgage market. Residential activity should continue to progress nicely this year, but the shift to rental will make developments look quite a bit different than we are used to.

Housing Costs Could Complicate the Inflation Picture

Headline inflation readings are quiescent, for now. But there are components within the Consumer Price Index (CPI) that could tell a different story soon and put upward pressure on measured inflation.

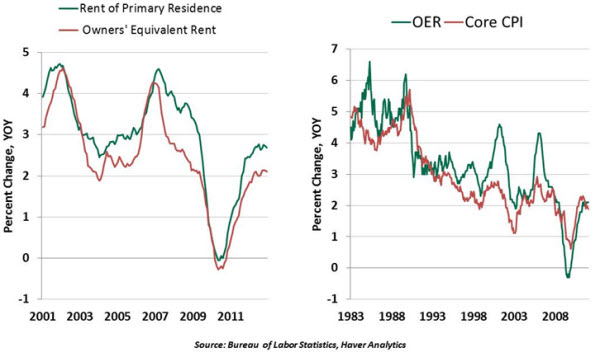

The candidate that comes to mind is owners’ equivalent rent (OER), which is part of the shelter cost component of the CPI. The OER is the proxy used to measure lodging costs for those who own their dwellings, as opposed to renting.

OER has a substantial influence on measured inflation, accounting for roughly 24% of the CPI. The weight of OER increases to a hefty 32% of the core CPI (which excludes food and energy).

By definition, the OER estimates that the “cost of shelter for a homeowner is the amount that the homeowner would have to pay in order to rent their home or a comparable home.” The BLS gathers rental information from 87 metro areas in owner occupied neighborhoods to compute OER. Therefore, rental trends influence the behavior of OER, not home prices.

Of late, the rent of primary residence component of CPI has been trending up (see following chart) at a noticeable pace. Based on the methodology used to compute OER, it is not surprising to see that it has also moved up after decelerating during 2007-2010. Historically, OER and core CPI are highly correlated.

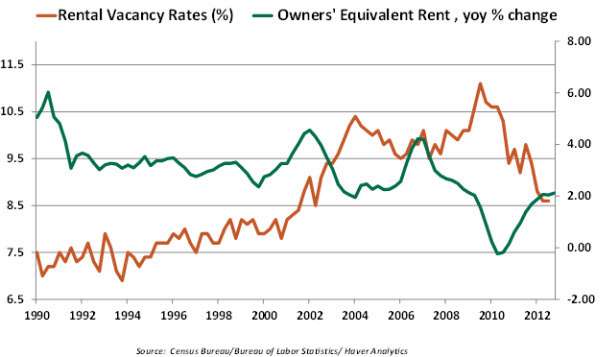

Underlying the recent increase in rents is the impact of the economic crisis, which led to millions of households shifting to rental property. The US homeownership rate declined from a peak of 69% in 2004 to 65% in the third quarter of 2012. Consequently, rental vacancy rates have dropped and pressure on rents has risen.

The important conclusion is that the relative price of owner-occupied housing can signal bothersome inflation because of developments in the rental market. It is not difficult to conjure up a situation where rents pressure the OER, and by association, the CPI. This would put policy makers in a tight spot. If household formation continues to increase at its recent pace, further pressure on rental costs is likely and a corresponding increase in OER is inevitable. That would challenge the Fed as it attempts to balance the two sides of its dual mandate.

A Calm FOMC Expected

The Federal Open Market Committee (FOMC) will conduct its first meeting of 2013 next week. Each January there is a rotation of four voting members from among the regional Fed Presidents. (The President of the New York Fed is a permanent voting member.)

This year, Presidents Charles Evans (Chicago), Eric Rosengren (Boston), Esther George (Kansas City), and James Bullard (St. Louis) will replace Presidents Lacker (Richmond), Pianalto (Cleveland), Williams (San Francisco), and Lockhart (Atlanta) as voting members of the FOMC.

Presidents Evans and Rosengren are presumed “doves,” favoring an aggressive continuation of quantitative easing. Presidents George and Bullard have both spoken out about the limits of quantitative easing, but it is not clear whether either of them would be inclined to carry on Lacker’s recent string of dissent.

The Fed is widely expected to restate its commitment to purchase $85 billion of MBS and Treasury securities each month until there is “substantial” improvement in the labor market. In the customary policy statement, the evaluation of economic conditions will be tweaked marginally as developments in the economy have not been sufficiently eventful to prompt a marked change from the December appraisal. This meeting does not include new economic projections or a press conference.

In January 2012, the Fed put forth broad outlines of its policy strategy pertaining to inflation, employment, and balancing of risk as part of the program to improve communications. The title of the statement was “Longer-run Goals and Policy Strategy” and the contents were consistent with the title. The focus was on the longer-run, as opposed to the short time span between meetings. Next week, the Fed will revisit these principles and possibly present a modified version of the 2012 statement.

The January 2012 statement noted the Fed’s longer run inflation target as 2.0%, measured by the change in the personal consumption expenditure price index. There is little reason to expect any change to this target. The Fed may, however, talk further about the appropriate phrasing around an employment target. Vice Chair Janet Yellen heads the FOMC’s communications sub-committee. Her speech on November 13, 2012 bearing the caption “Revolution and Evolution in Central Bank Communications” highlighted the Fed’s differing views about full employment. Yellen’s remarks indicate that new color on the longer-run normal unemployment rate is possible in the strategy statement.

“Unfortunately, there is a considerable range of disagreement in the economics profession and on the FOMC itself about what this longer-run normal rate of unemployment is. Moreover, there is widespread recognition that whatever the normal rate might be today, it can change over time. So the consensus statement notes that, as of January 2012, FOMC participants' estimates of this rate had a central tendency of 5.2 percent to 6.0 percent. I expect the FOMC to review its estimates of the longer-run normal rate of unemployment in its annual reaffirmation of the consensus statement on goals and strategy.”

Other than these fine tunings of communication, the outcome of the meeting should be very uneventful. The FOMC discussions likely won’t get interesting until later in the year, when several members have suggested that quantitative easing should be reduced or ceased.

© Northern Trust