In the ensuing days and weeks there will be plenty of opinions about what passed and what will continue to be negotiated in the drama known as the fiscal cliff. The spectacle of across-aisle dealings makes for a well rated "Reality" show (Fiscal Riff?), but poor ratings for both effectiveness and efficiency in governance. With US-centric issues in the forefront, the focus has been taken off the ongoing Euro Zone talks, which continue to plod along. Contrary to popular opinion at the start of 2012, the Euro Zone ended the year as it entered it—with 17 currency sharing members. For the wider European Union (EU), instead of disintegrating, and despite the United Kingdom's uncertainty about continuing its membership, it continues to receive applications for membership. In late 2012, the EU was awarded the Nobel Peace Prize for its role in advancing peace and reconciliation, democracy and human rights in Europe. Negotiations are never very pretty or fast enough for the impacted observer, who can become as nervous as a first time cliff diver, as the sound bites used by participants stir up deep seated emotions.

To repeat what has been our position all year, things are generally going in the right direction despite hauling around the deadweight of Europe and dealing with persistent uncertainty in the U.S. While both the developed and developing economies have recovered from the 2008 recession, the well financed emerging and developing economies are outpacing the debt ridden, developed economies. The GDP in Britain, Japan and the EU is at about the same level as it was the first quarter of 2007, with the US about 5% above and other EU economies still below those levels. The developing economies continue to gain ground against the old guard and, during the same time frame, economic output is ahead more than 25%, with China never dropping into negative growth territory. While the developing world growth rates are slowing, there is still a wide gap between the economic growth rates of the developed and developing world.

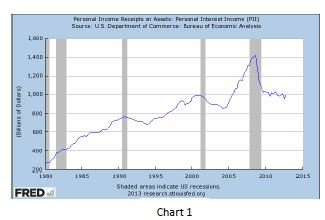

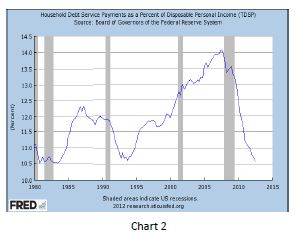

Behind the scenes, the ultra-low interest rates we have both endured and benefited from over the last four years have created a very potent macro-economic foundation for our economy. But, this longer-term economic benefit has a cost, as low interest rates are a double-edged sword. On one edge, investors that live on interest income derived from CD’s, Municipal, Corporate or Government bonds have seen their income levels shrink (Chart 1), unless they have sought out alternatives (see the 08/01/2012 Stellar White Paper). On the other edge, borrowers (businesses and individuals) have seen their debt service expense shrink dramatically, increasing their net disposable income (Chart 2). This has created a stealth redistribution of income, where debtors benefit at the expense of creditors.

If long-term interest rates begin rising (a scenario we have previously discussed), a stealth redistribution of wealth will also occur, as locked in low interest rates on debt become an asset for borrowers and a liability for lenders.

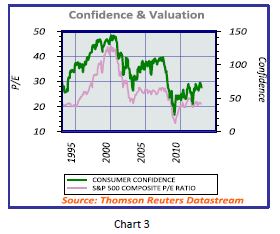

Confidence is critical to the success of any capitalistic society. It impacts the desire of companies to hire, lenders to lend, borrowers to borrow, companies to invest and consumers to spend. It drives the velocity of money and the valuation of investment assets. Higher confidence levels are typically correlated to high valuation levels (Chart 3).

The lack of certainty about fiscal issues has contributed to lower confidence levels and reduced economic output as sensible business owners have held off making marginal hiring and investment decisions. If certainty improves in 2013, confidence should also improve, leading to more improvements in the economy and higher valuations for investments. Rising confidence would be good for equity investors, as rising P/E (price/earnings) ratios could more than offset the expected lower earnings growth rates for the S&P 500 companies. It is a different story for bond investors, as rising confidence is also correlated with rising interest rates (Chart 4), and falling bond prices.

There is ample and well founded concern about the near-term future of the developed economies, as many domestic and European issues remain up in the air at this writing. Typically markets tread water until a clearer picture develops. However, as we have seen, with limited investment alternatives to low interest rates, an absence of bad news can attract cliff dwelling investors to stocks.

Happy New Year!

Stephen J. Taddie

Managing Partner

December 31, 2012

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this newsletter (article), will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for your portfolio. Due to various factors, including changing market conditions, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter (article) serves as the receipt of, or as a substitute for, personalized investment advice from Stellar Capital Management, LLC. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. A copy of our current written disclosure statement discussing our advisory services and fees is available for review upon request.

© Stellar Capital Management