No, it's not a life aspiration. But it can work when it comes to investing. We had a rush of gains coming into the end of the year with the S&P[1] up 22% over the year. But it's also one of the more relaxed markets and start we've had in years. The political agenda is still front and clear and we're in a lull until the debt ceiling arguments gain steam. The markets know this but seem comfortably complacent. They're probably right to be. Some deal will be worked out and it's highly unlikely we'll get to the point where debt interest, social security, Medicare or veteran benefits won't get paid. Meanwhile, we had a welcome consolidation week with treasuries ahead, the S&P holding onto gains and Europe mercifully quiet. The one surprise was the ongoing strength of the euro which quickly caused some alarms in export sectors. Talking a currency down or up is tough and while it's good to see stabilization in the euro, any prolonged strength above €1.40 will be hard for recovery.

US Economy

Clear and encouraging signs in a busy week. Here's the summary:

| Favorable | Housing, unemployment, monetary policy (much better in recent weeks), claims, bounce in durable goods, inflation, Europe quiet and steady. |

| Still challenged | Debt ceiling, wage and compensation growth, nominal GDP, industrial production, exports, top line growth,ISMandNFIBsurveys weak. |

| "Good" but troubling | Inflation.PPIandCPIthis week were well below Fed guidance. Most of the drop is gasoline and evenOERis down. But this allows no top line growth for companies |

Housing is a lead story.

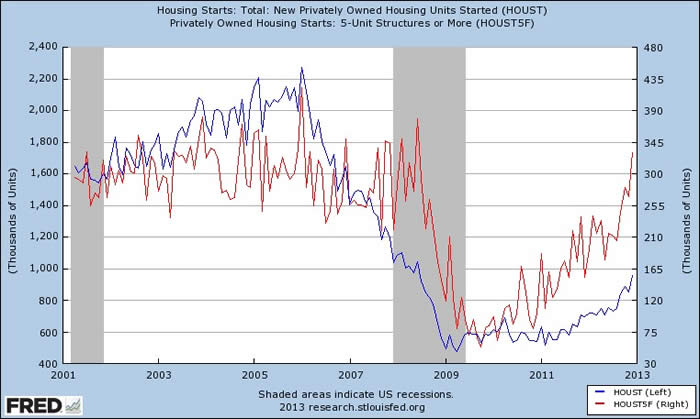

Prices, transactions and starts are all good. TheNAHBsurvey had a strong report on buyer traffic. Residential fixed investment is on track for the best quarter in years. And the Sandy rebuilds are still to come. The house price increases are important as is the lower inventory overhang because six months ago, only 55% of mortgages had a loan/value ratio under 80%. That's the threshold for refinancing. If prices continue to climb we're going to see more people eligible for refinancing as well as a positive wealth effect. Last week housing starts came in at 954,000, which is up 37% YOY and the best level since June 2008. Regular readers know we also keep an eye on the 5-units or more build which came in at 330,000 or twice the rate of last year. Why? Well more multi-family housing should relieve any rent pressures and accommodate household formation that would otherwise sit tight until single family houses become affordable. Here they are together:

Source: Federal Reserve Bank of St. Louis, Economic Research

The underlying trend in nearly all measures of housing is up and we have also seen sizable decreases in unemployment in some of the states with the hardest hit real estate problems. So in the last year, Nevada and Florida saw overall rates of unemployment fall nearly 3% and 2%, respectively.

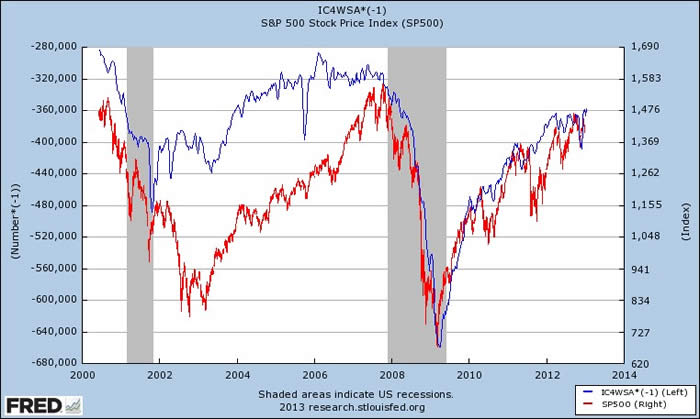

Another good sign was a big drop in jobless claims to 335,000. The market is very sensitive to employment statistics and part of last week's action is because of the improved trend. Here's the four week moving average of claims against the S&P:

Source: Federal Reserve Bank of St. Louis, Economic Research

Four Key Numbers

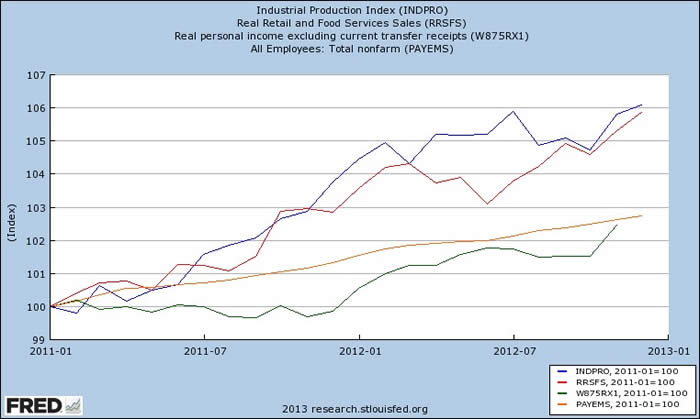

Growth will be slow for Q4. The recent trade numbers did it in for any robust growth and retail sales were soft. Q1 has the payroll tax hike to contend with but there's some slow recovery in corporate confidence. Here are four key numbers that came in last week: industrial production up 2.2%, retail sales up 2.5% (but core was weak) and real personal income eking out small gains. There all at two year highs. They're also all coincident indicators that tell us more where we are than where we're heading but, hey, it's good news.

Source: Federal Reserve Bank of St. Louis, Economic Research

Confidence is still fragile.

The Empire and Philly Fed indexes are the first indicators we have of 2013 data (most others are from December). The news was not good. The Empire showed its sixth straight month of negative conditions and the Philly Fed had new orders dropping to -4.3 from +4.9, reversing almost all the December increase. Worse news is probably coming as tension over the debt ceiling rises (HTPantheon Economics). The Beige Book, which covers all twelve Fed reporting districts, described growth as modest or moderate with almost no wage pressure.

Another casualty of the debt plight was the University of Michigan confidence index which dipped to 71.3 from 72.9. The rise in the payroll tax also did some damage to confidence and this may worsen as the month unfolds.

International

In Europe we have much better reads on financial conditions. Spreads have tightened and stabilized, equity markets sustained their gains and current accounts surpluses improved. This has greatly helped the euro but the real economy is worsening. Bund yields look way over bought and if there's any fiscal stimulus in Germany later this year (and odds are good), equities will perform well. Bonds will not. That's the trade we're on.

Japan…see the report we put out on Japan last week. We think this stimulus is different because 1) it comes with a loosening inflation target 2) PM Abe has a majority and clear mandate 3) the yen weakening and possible eurozone government bond buying look sustainable.

The China rebalancing story is stalled. Friday's GDP numbers show that infrastructure spend remains the driver. The speculation of new companies coming to market is way overdone. It may be a contrarian indicator as company owners are finding ways to off load their investments and diversify out of the renminbi.

Bonds

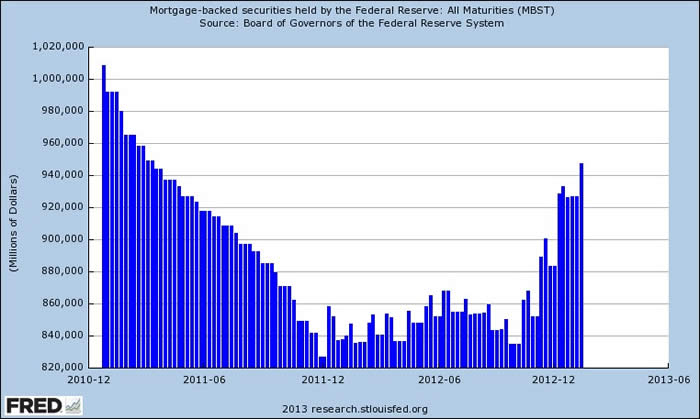

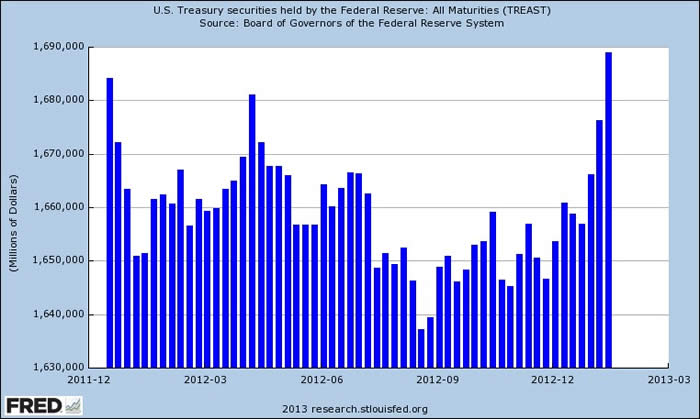

We saw the GT10s trade around 1.82% for much of the week. We recently had auctions of 3s/10s/30s with the 30s bid at 3.07% and the 10s at 1.86%. The 30s saw a rally to 2.98%. The treasury market has no supply for two weeks and we have nine buy-backs of which five are in the 30-year part of the curve. So we have tended to buy treasuries later in the day and hold overnight. Remember the buy-backs from the NY Fed come in the mornings. Some of the Fed's recent buying is shown in theMBSholdings here:

Source: Federal Reserve Bank of St. Louis, Economic Research

And in the Treasury holdings here:

Source: Federal Reserve Bank of St. Louis, Economic Research

We also had a week where regional Fed presidents mostly confirmed the buying program. Dallas president Fisher talked about buying having a "lesser impact" but did not go so far as to talk of any policy change. Hyper hawk turned dove, Minneapolis Fed president Kocherlakota, gave three speeches in as a many days confirming that while "ultra low rates" were no panacea, the target was 6.5% unemployment and there was little change needed until that was achieved. So last week's misplaced fear of a possible early cessation of the bond buying program looks over for now.

Credit is probably overbought in the short-term. Spreads feel a little tight. There are lots of well subscribed deals but the Dell news put some frighteners in the market. While M&A activity can be good for equities, it's decidedly bearish for credit when a private equity firm takes over. The standard business model is to leverage the balance sheet and narrow the interest cover. The bond market remains very headline sensitive and, given how well it's done in recent months, prone to sell-offs.

Equities

We have a rotation into equities. This is everything from 401(k) rebalancing, financial advisors adjusting down bond over-weights and some "catch up" from the equity rally in 2012 that did not have lot of participation. Expect more sprints on the market. Probably to around 1500. We're still early in earnings season but banks leading so far have been good.

Bottom Line: Range definition for treasuries remains in the 1.75% to 1.95% level. This is a quiet earnings season so far. Around 70 of the S&P companies have reported and earnings surprises are a very modest 9%. This coming week sees more action but for now the amount of flows and general calm in the market should keep things well supported.

Sources: Bloomberg, Bureau of Economic Analysis, Bureau of Labor Statistics, CRT Ader Capital Economics, Federal Reserve Bank of St. Louis, Federal Reserve Board, FT Alphaville, J.P. Morgan Market Intelligence, High Frequency Economics, Pantheon MacroEconomic Advisors, Tim Duy's Fed Watch, US Treasury Department, Sentinel Asset Management, Inc.

[1] Standard & Poor's 500 Index is an unmanaged index of 500 widely held US equity securities chosen for market size, liquidity, and industry group representation. An investment cannot be made directly in an index.

© Sentinel Investments