All markets were closed yesterday due to the federal holiday marking

Martin Luther King Day.

Last week saw the markets continue to trade off of concerns over Apple, and just what might happen in Washington DC concerning the debt limit negotiations.

Earnings season will hit high gear this week.

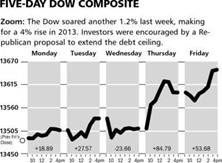

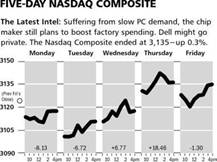

As the charts above illustrate, the Dow Jones Industrial Average gained 1.2% while the NASDAQ Composite moved higher only slightly.

The Markets & Economy

News of a possible three-month resolution to the debt ceiling negotiations fueled a rally on Friday. This, combined with the rather aggressive money printing that Japan has recently embarked upon, has set the stage for a continuation of the liquidity-fueled rally in stocks.

The question is can all of this money floating around sustain the move, and more importantly, can it help the global economy? I believe the case for money flowing into stocks is a better one to make than a renewed case for global growth.

It is becoming increasingly clear to most everyone that the global economy is barely sputtering along. That is why the Central Banks of the world, now including Japan, continue to worry much more about deflation rather than inflation. In the case of Japan, their new government has come to power with the mandate of doing whatever possible (read that to mean printing money) to stave off deflation and try to jumpstart inflation.

This is creating a sea of liquidity, which along with our own Central Bank is creating the fodder to fuel the rally in stocks. We have described this many times in the past as being good for investors, but the impact on the real economy is de minimus.

This also explains why corporations are reluctant to expand and instead are more interested in raising dividends, buying back stock, or even going private as is the case for Dell Computer. These steps at financial engineering are great for shareholders but do not create jobs or growth in the economy, and ironically exacerbate the trend towards the “have and have not’s” in our society. Not good.

What to Expect This Week

As mentioned above this is a holiday shortened week, but still important. Apple reports their numbers tomorrow evening, and it has now become the most important report of the earnings season.

The debate continues on as to the health of the economy, and this week’s reports on new home sales (Friday) or the leading economic indicators (Thursday) will give people more insight into 2013.

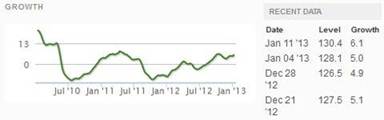

The weekly update from the Economic Cycle Research Institute as shown below shows no sign of the recession they have been calling for since September of 2011. Importantly, given the higher taxes facing us this year there is no indication that growth for 2013 will step up. Europe is in recession, and the news on the global terrorist front is keeping oil prices much higher than they should be which also is pinching the outlook.

Again we keep coming back to the same key item: The Federal Reserve Board here at home and the central bankers globally all want stocks to go higher and

that is hard to argue with at this point.

![]()

SYMBOL: FCX

Shares of Freeport-McMoRan are trading higher this morning after reporting better than expected fourth-quarter earnings results. Revenues rose by 8.5 percent from a year ago to $4.51 billion, as copper production came in higher than Wall Street was expecting. Earnings per share also came in at $0.74, which was 2 cents higher than expectations. Management also raised its copper and gold production outlook for next year.

This is the best quarterFreeport has reported in more than a year, so we are encouraged by the better operations at the Company. Not only was the Company able to increase its copper production to 3.66 billion pounds in 2012, but they expect to produce more than 5 billion pounds a year by 2015. The cost of producing a pound of copper also decreased to $1.54, which indicates much better labor conditions. We expect the cost of producing copper to continue to decline, as operations in Indonesia have drastically improved since ending the strike at its largest mine .

Shares of Freeport have recovered since announcing its buyout of two energy companies this year. These results help to give this management team more credibility, and we still expect Wall Street to warm up to the Company’s move into the energy markets. The conference call is later today, and we expect the tone to be positive. We maintain our belief that shares of Freeport will reach $45 by the end of this year.

![]() Three-Month Chart

Three-Month Chart

![]()

SYMBOL: BRCD

Last week Brocade announced that they had hired Lloyd Carney to take over the CEO role. Former CEO Mike Klayko had reported in August that he would be resigning once a formidable candidate was found to replace him. We believe Mr. Carney is the perfect fit for this job and expect Wall Street will be pleased to have him take over control of the Company.

Mr. Carney has worked in the technology industry for more than 30 years and has had success selling his companies to larger players. The last two companies that he ran were purchased by IBM and Oracle. We believe that he was brought into this position to sell Brocade, and his connections in the industry are extremely valuable. We believe a buyout of Brocade would happen at $10 per share, although timing of any transactions are hard to predict.

![]() Three-Month Chart

Three-Month Chart

© McIntyre, Freedman & Flynn