The severity of damage determines the length and intensity of rehabilitation. Some setbacks can be overcome quickly. Others, like those endured by the Jersey shore and Lance Armstrong’s reputation, will take longer to mend.

It has therefore been surprising to get a sense from monetary officials in Europe and the US that economic rehabilitation efforts are nearing an end. Given the severity of the challenges faced in each location, one might have thought that more extended therapy was in order.

Amid a deepening recession and uncertain financial markets, several members of the European Central Bank (ECB) Governing Council proposed cutting rates late last year. Yet at its January meeting, that possibility was taken off the table unanimously. As justification, ECB President Draghi cited “a significant improvement in financial market conditions and a broad stabilization of cyclical indicators.”

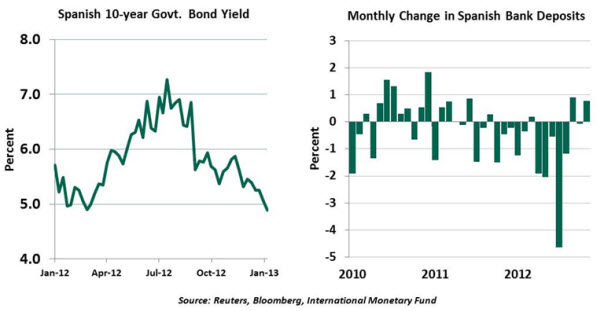

To be sure, some of the more troubling trends in Europe seem to have been arrested for now. Taking Spain as a leading example, government bond yields have fallen dramatically since last summer and deposit outflows from the nation’s banks have ceased.

The statements and programs crafted by ECB officials have certainly helped to allay fears. But without concrete steps to build on these grand plans and pronouncements, the Continent may find itself facing another round of financial instability before 2013 is long underway.

The Eurozone economy has contracted for three consecutive quarters, and is likely to continue downward for much of this year. That trend will diminish tax revenues and challenge delicate budget dynamics. Sustained investor forbearance is linked to the ability of countries to meet targets for reducing debt; a shortage of collections would increase the need for spending reductions. Austerity has already challenged the stability of political coalitions and the patience of the populace; calls for more sacrifice will not be well-received.

Further, many still believe that European governments will eventually be forced to write down the value of Greek debt held in the official sector. That won’t aid the cause.

The ECB’s Open Market Transaction (OMT) program was announced last September, promising to purchase sovereign debt if investor reception was less than robust. The presence of this structure, along with Mr. Draghi’s pledge to do “whatever it takes,” has been credited with improving the results of recent European debt auctions.

But no country has stepped forward to request help under the OMT, which comes with conditions like fiscal discipline and external oversight. Troubled countries have been reluctant to allow increased outside involvement in their domestic affairs.

Interestingly, the comfort provided by calm financial markets has allowed some retreat from the difficult measures that many deem necessary. Fiscal targets are not being strictly enforced, and support for the plan to consolidate European bank supervision under the ECB umbrella is fraying a bit at the edges.

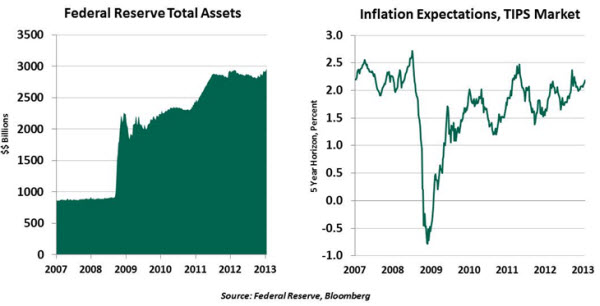

In the US, Federal Reserve officials have been particularly vocal over the past few weeks. A frequent topic has been the appropriate duration of the current quantitative easing program, which has the Fed’s balance sheet on its way to exceeding $4 trillion at the end of this year.

The minutes of the December Federal Open Market Committee meeting stated that “a few members expressed the view that ongoing asset purchases would likely be warranted until about the end of 2013, while…several others thought that it would probably be appropriate to slow or to stop purchases well before the end of 2013, citing concerns about financial stability or the size of the balance sheet.”

Many had assumed that the Fed would continue its unconventional policy for a much longer period of time, given that it has been tied to substantial improvement in the labor market. While we seem a long way from that objective, FOMC members may be reaching the conclusion that the value of pressing on may be diminishing and the risks of pressing on may be rising.

While inflation seems well-contained for now (as my colleague Asha Bangalore discusses later on), inflation expectations have been moving up gradually for the last two years. While the Fed has plans for an orderly exit strategy, its success is not guaranteed. And while the Fed would certainly like to see lower joblessness, monetary policy may ultimately be limited in its ability to achieve this aim.

So we have two central banks who may be taking steps to retreat from the accommodation that they have been providing. The question is whether the underlying economies are healthy enough to move ahead without additional treatment.

An Update from Washington

In the US capital, preparations are underway for next week’s inauguration. If austerity is the watchword for politicians, it certainly isn’t evident in the scale of the parades and parties that will commemorate the occasion.

Discussions during several days in DC this week yielded the following insights:

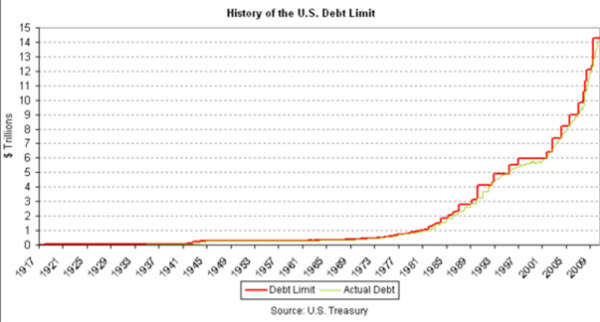

- Few expect the Congress to allow us to hit the debt ceiling with force. Instead, however, a series of very small and short-term extensions are possible. This is not an unusual strategy; of the more than 100 increases in the debt limit over the last century, several came only weeks apart.

- Short-term extensions would buy time, but extend the drama. Financial markets have held up well during recent budget tensions, but business and consumer confidence remains at risk.

- There are those in Washington who feel that the broad spending cuts (the sequester) which had been postponed for two months will be allowed to take hold on March 1. This would have a negative economic impact, harming defense contractors most prominently. But it wouldn't immediately jeopardize the continuity of interest payments on Treasury debt.

- The Federal government is currently operating on what is known as a continuing resolution (CR). This authorizes continued spending even in the absence of a formal budget being passed. The current CR will run out very shortly, and will have to be reauthorized. This could be a dicey process given larger issues in the background. A short government shutdown may not be such a remote possibility.

- If the debt ceiling is not increased, the Treasury will have to prioritize payments. Most expect that interest on the national debt will be given top priority. But that choice could hinder the continuity of other disbursements such as, perhaps, Social Security checks. If interest is not fully paid, the Treasury could be in technical default, potentially roiling the financial markets. Some officials appear less troubled by the prospect of a technical default on Treasuries. "Where are investors going to take their money?" they ask. A fair point, but mixed with worrisome hubris.

Serious discussions over spending and the debt ceiling may still be weeks away. There is consensus that resolution, if it comes, will likely arrive only at the last minute.

Inflation – To Worry, or Not to Worry

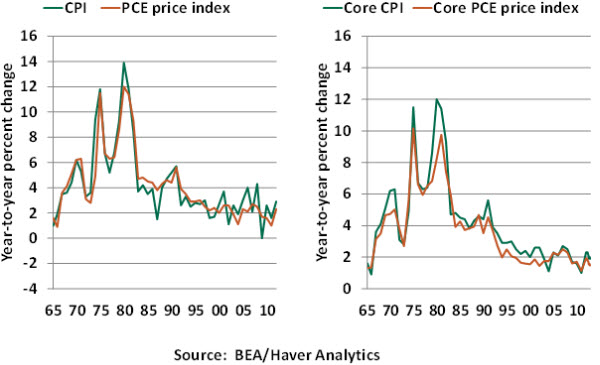

The US Consumer Price Index (CPI) rose 1.7% in all of 2012, one of the most benign readings in the past fifty years. The deflator on personal consumption expenditures (PCE), the Fed’s preferred inflation measure, was similarly muted. A decline in energy prices last year was an important part of the story, but the core CPI, which excludes food and energy, moved up only 1.9% in 2012. So current inflation is very modest; will it stay that way?

Some members of the FOMC have signaled concerns about the inflationary potential of continued large scale asset purchases. In our opinion, unease about future inflation is natural and healthy, but the timing of these worries is premature when placed in the context of current economic conditions.

Identifying signs of impending inflation involves tracking demand and cost pressures, commodity price trends, and possible signals from components of the CPI itself.

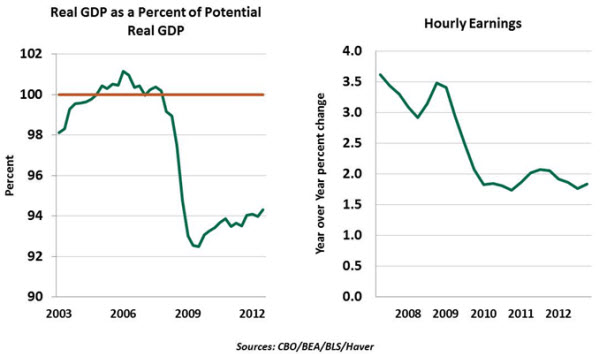

The modest increase in real GDP during the 14 quarters of the current expansion has left real GDP nearly 6% short of the potential GDP (see chart below). This suggests that there exists considerable unused economic capacity, as evidenced by a jobless rate (7.8%) that is noticeably higher than the level consistent with full employment. The resulting slack in the labor market has translated into sluggish growth in hourly earnings and little pressure on labor costs.

As the US is overwhelmingly a service economy, it would be difficult for inflation to break out of its recent range until joblessness declines meaningfully.

Commodity price trends are reflected very quickly in price gauges like the CPI. Commodity prices have retreated considerably over the past two years, and projections of lackluster global economic growth point to a subdued trend of commodity prices in the months ahead.

Shelter (which represents housing costs) is the most significant element of the core CPI, accounting for roughly 45% of the index. The shelter price index has risen noticeably in the last two years, amid rising demand for rental property. We will be tracking the shelter component of CPI closely as employment conditions improve and household formation moves up.

Thus far, potential sources of an inflationary threat are well-contained, suggesting that concerns can stay on the back burner for a while. This supports the view that the Fed’s choice to focus on growth in the inflation-growth debate is not misguided.

© Northern Trust