4 Sensational Facts About Gold Investing That You Might Not Know

4 Sensational Facts About Gold Investing That You Might Not Know

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

|

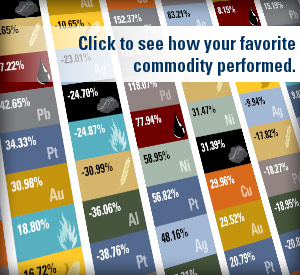

Our ever-popular Periodic Table of Commodity Returns has been updated through 2012. Investor Alert readers love this chart as it shows a decade of results across 14 different commodities, providing strikingly rich information in a very familiar format.

Last year, 11 commodities rose in value, with wheat rising as the top crop after seeing a significant decline in 2011. It was a similar rags-to-riches story for the next few leaders: lead, zinc, natural gas and platinum all climbed double digits in 2012 after falling in 2011.

Only three commodities declined over the year: Crude oil fell by 7 percent after rising 8 percent the previous year. Nickel declined for the second year in a row. In 2012, the metal lost 9 percent and in 2011, nickel fell another 24 percent.

Coal was the worst-performing commodity in 2012, falling nearly 17 percent. Coal’s been going through a rough spell lately; in fact, the commodity has not been king for five years (although it did record a 31 percent increase in 2010). As Global Resources Fund Portfolio Manager Evan Smith explained to listeners during our recent presentation, for the first time ever in the U.S., natural gas provided more electricity and power than coal did.

As you can see from the table, commodities often have wide price fluctuations from year to year given the many factors affecting supply and demand, such as government policies, union strikes, and currency volatility. That’s why when it comes to commodities and commodity producers, many investors “leave the driving” to active money managers who understand these specialized assets and the global trends affecting them.

Take gold and gold companies, for example. After investing in the mining industry for decades, we’ve taken note of several facts about gold that continue to surprise our investors. Here are four of the latest:

1. Gold Has Been A Consistent Performer Over The Decade

While the precious metal did not shoot the lights out in 2012, gold’s bull rally goes on. It ended the year up 7 percent, making it a phenomenal 12th year in a row that gold rose in value. In a special gold bar version of the Periodic Table below, you can easily see gold’s rotation among the commodities from year to year.

What’s fascinating is the three-year rising pattern relative to other commodities that emerges when you focus on the bars. Over the past 10 years, gold has risen in position compared with the others for three years in a row, then fallen in relative position in the fourth year before repeating the cycle. Will it follow the same pattern and be in the top half of the Periodic Table in 2013?

2. Gold Should Remain A Hot Commodity In 2013

Considering the global easing cycle and the continuous running of monetary printing presses, I believe the Fear Trade will continue to be a driver of gold over the next several months. Take a look at the projected rise in the balance sheets as a percent of GDP from the European Central Bank, the Bank of Japan, the Federal Reserve and the Bank of England over 2013. The ECB is estimated to have a balance sheet that is nearly 50 percent of its GDP by the end of the year. The Bank of Japan is right behind the ECB, with its balance sheet projected to be nearly 35 percent of GDP. As Mike Shedlock of Mish’s Global Economic Trend Analysis said, “The race is on to see which central bank can load up its balance sheet with the most garbage the fastest.”

My friend Ian McAvity also summed it up well in his Deliberations on World Markets: “Gauging from the panicky actions of the major central banks, I would still prefer to own gold than their paper.” With the monetary printing presses warm and real interest rates in the red, gold will likely glimmer for another year.

3. Gold Is The Least Volatile Commodity On The Table

Given the fact that every gold move is analyzed and dissected by the media, it may surprise you that this precious metal was actually the least volatile of the 14 commodities. Its rolling 12-month standard deviation (sigma) over the past 10 years has been 14 percent, compared to the most volatile commodity, (nickel), which has a rolling 12-month sigma of nearly 60 percent.

Here’s another way to look at the surprisingly low volatility of gold. Take a look at the frequency of 10 percent moves up or down over any 20 trading days. The metal is only slightly more volatile than the S&P 500. Gold companies, crude oil and the MSCI Emerging Markets Index have all experienced more up and down moves than gold.

Measuring Monthly Volatility as of 12/31/12

Calculated over rolling 20-trading day periods in past 10 years

|

Number of +10% moves |

Number of -10% moves |

Frequency of +/-10% moves |

|

| NYSE Arca Gold BUGS Index (HUI) | 490 | 296 | 30% |

| WTI Crude Oil | 434 | 302 | 29% |

| MSCI Emerging Markets (MXEF) | 139 | 169 | 11% |

| Gold Bullion | 130 | 60 | 7% |

| S&P 500 Index (SPX) | 33 | 72 | 4% |

Whereas card counting at a Blackjack table can get you booted from casinos and barred for life, as an investor, you are allowed to take full advantage of counting the 10 percent moves.

Over 2013, you can count on gold moving in either direction, so even if the metal experiences extreme volatility to the downside, regardless of what the headlines report, Investor Alert readers know that any dip in price offers potential buying opportunities. Keep in mind though, that it’s prudent to invest only 5 to 10 percent of your total portfolio in gold and gold stocks.

4. The Last 4 Years Were Better Than You Thought

Last week, I showed how the S&P 500 Index and gold bullion significantly outperformed the iShares Core Total US Bond ETF. Many investors asked about gold stock performance. As you can see below, the NYSE Arca Gold BUGS Index (HUI) experienced quite a gain, increasing more than 50 percent on a cumulative basis since the beginning of 2009. Both considerably outperformed the bond investment.

What’s sensational news to precious metals investors sometimes doesn’t make the cut as breaking news. We emailed a message to our readers earlier today, asking you to tune in to CNBC to see me talk about silver. I’m pleased to hear that there were many of you who tried to tune in (Thank you!), but I’m sorry to say the reporters preempted my investing insights for what was viewed as a more sensational story about millionaire and fugitive John McAfee.

In the meantime, I’ll continue sharing these fascinating facts about gold, silver and other commodities with investors at Cambridge House’s Resource Investment Conference in Vancouver. Hope to see you there!

Index Summary

- The major market indices all finished higher this week. The Dow Jones Industrial Average rose 1.20 percent. The S&P 500 Stock Index increased 0.95 percent, while the Nasdaq Composite gained 0.29 percent. The Russell 2000 small capitalization index closed the week with a 1.37 percent gain.

- The Hang Seng Composite Index rose 1.46 percent; Taiwan fell 1.10 percent, while the KOSPI fell 0.44 percent.

- The 10-year Treasury bond yield fell 3 basis points this week, to 1.84 percent.

Domestic Equity Market

The market ended higher for the third week in a row as the quarterly earnings season began but will kick off in earnest next week. Cyclical areas outperformed, with energy, industrials and consumer discretionary leading the way, while telecommunications services was a notable laggard.

Strengths

- The energy sector led the way this week after lagging modestly last week. Oil rose nearly 2 percent this week, supporting the gains. Gains in the sector were broad-based with most stocks moving higher. Refiners led the way, followed by coal and oil & gas drillers.

- Industrials were strong this week in what was also a broad-based rally. General Electric reported earnings on Friday which exceeded expectations for both earnings per share and revenue. The stock rose nearly 3.5 percent on Friday.

- Dell was the best performer in the S&P 500 this week, rising 18.2 percent. The company is in discussions with private equity firms regarding a leveraged buyout to take the company private.

Weaknesses

- The telecommunications service sector was the worst performer for the second week in a row as AT&T reported a $10 billion charge for its pension plan and smartphone discounts.

- The technology sector underperformed even on the back of Dell’s strength. Index heavyweights such as Google, Apple and Intel were among the worst performers. Intel negatively surprised the market with a significant increase in its capital expenditure budget for 2013.

- Capital One Financial was the worst performer in the S&P 500 this week, losing 8.1 percent. The company reported earnings on Friday which missed analysts’ estimates. Revenue guidance for 2013 was also disappointing.

Opportunity

- The focus will be on earnings over the next few weeks, with Apple, Google, McDonald’s and Starbucks, among others, set to report next week.

- It appears Congress will kick the can a little farther down the road and pass temporary debt ceiling relief until mid-April.

Threat

- The dysfunctional political process brings little hope for the U.S. to regain its AAA credit rating and more credit downgrades are possible if Washington remains acrimonious.

The Economy and Bond Market

Treasury bond yields fell slightly this week as market-moving economic data was light and the equity market was unusually subdued as it awaited a heavy earnings calendar next week. The most impactful news from this week was the surprising acceleration in housing starts, which rose 12.1 percent in December. The economy is beginning to “feel” better and housing is a key piece to that puzzle, possibly setting up the economy to positively surprise in 2013.

Strengths

- December housing starts rose a robust 12.1 percent. Housing starts rose 28.1 percent in 2012, the biggest annual increase since 1983.

- Initial jobless claims fell to 335,000, a five-year low.

- December retail sales rose a better-than-expected 0.5 percent. Auto sales rose 1.6 percent and were a key driver of the stronger-than-expected reading.

Weaknesses

- The University of Michigan Consumer Confidence Index unexpectedly fell to 71.3 from 72.9; expectations were for a rise. Higher payroll taxes were cited as the driver behind the fall.

- Eurozone industrial production fell for the third straight month in November.

- German GDP contracted by 0.5 percent in the fourth quarter and the government cut its 2013 growth forecast to a meager 0.4 percent.

Opportunity

- The debt ceiling debate appears to be pushed into April, allowing the market to focus on economic fundamentals.

- While some Federal Reserve members expressed concerns over continued quantitative easing, the Fed still remains committed to an extremely accommodative policy until the economy improves.

- Globally, central banks are increasing their stimulative policies, with Japan’s recently elected prime minister vowing to take on deflation and deflating the Yen.

Threat

- Earnings season will kick into high gear next week. With mixed results from the few companies that reported this week, focus will be on the outlooks for 2013.

Gold Market

For the week, spot gold closed at $1,684.30, up 21.5 per ounce, or 1.29 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, lost 0.60 percent. The U.S. Trade-Weighted Dollar Index gained 0.60 percent for the week.

Strengths

- The Central Bank of Russia (CBR) bought 650,000 ounces of gold in December, its largest monthly purchase since September 2010. The CBR’s policy is generally to maintain a gold-to-FX reserve ratio of around 10 percent and as of year-end 2012, that ratio stood at 9.5 percent.

- Silver reached a one-month high as the U.S. Mint sold out of 2013 American Eagle silver coins. The silver coin sale will resume on or about the week of January 28 once inventory is replenished.

- A report by the Official Monetary and Financial Institution Forum (OMFIF) suggests that demand for gold will increase as central banks of emerging economies become increasingly interested in gold in the gradual transition out of a single global reserve currency system.

Weaknesses

- Two central security guards were killed at Tahoe Resources’ silver project in Guatemala when their patrol was ambushed by armed criminals. It is the third act of violence against projects or operations in Guatemala this month.

- Germany’s Bundesbank has announced a phased relocation of all its gold held in France and 300 tons of its gold held in the Unites States, to be moved to Frankfurt by 2020.

- Rio Tinto, the world’s second-largest mining company, will take about an additional $14 billion of write-downs for failed deals in aluminum and coal. Chief Executive Officer Tom Albanese, behind the deals, will be leaving the company after six years in charge.

Opportunities

- Peru approved Rio Alto Mining, the developer of the La Arena copper and gold mine in Peru, as an investment for domestic pension funds.

- Centerra reported 2012 gold production of 387,076 ounces while providing its production outlook for the current year. Ian Atkinson, President and CEO, stated that Centerra’s Kumtor mine had disappointing results, but he expects 2013 production to almost double between 605,000 and 660,000 ounces.

- According to Thomson Reuters GFMS, gold will likely climb toward $1,900 an ounce and average a record in the first half of this year as central bank stimulus boosts investment demand. Central banks added the most gold to their respective reserves in 48 years over the course of 2012, and will likely buy another 280 metric tons in the first half of 2013.

- Anglo American Platinum announced the closure of its Rustenburg mine, slashing expected annual platinum production by 400,000 ounces. Both the South African government and its labor unions are unhappy with the plan, but it is a positive for the price of platinum.

Threats

- Senator Tom Udall, D-NM, and others are seeking to overhaul the General Mining Law of 1872, originally signed into law by President Ulysses S. Grant to promote mining in the West. If successful, the U.S. government could gain hundreds of millions of dollars in the next decade by collecting royalties from gold, silver and other mines otherwise exempt under the 1872 mining law.

- One suggested proposal is to charge a 12.5 percent royalty fee, which would generate about 3 billion over 10 years, estimates Representative Edward Markey from Massachusetts.

- CanaccordGenuity cut its one-year peak gold forecast to $1,850 from $2,000, and silver to $35 from $40. They see potential for two-year peak gold at $2,000 and silver at $40.

Energy and Natural Resources Market

Strengths

- Natural gas climbed to a six-week high on Friday, as colder temperatures in the Eastern U.S. boosted home-heating demand and reduced inventories by greater-than-expected levels. Stockpiles declined by 148 billion cubic feet (bcf) last week, a bigger drop than analysts' expectations of 137 bcf.

- The China State Electricity Regulatory Commission said that power consumption grew 7.45 percent in the fourth quarter, up from 3.9 percent in the third quarter, and that it is expected to grow more than 9.9 percent in 2013, up from the 5.5 percent increase in 2012, but below the 12 percent seen in 2011. This would be in line with a forecast of improving GDP growth, but not a dramatic re-acceleration.

- Coal exports from Queensland's four largest coal terminals were 17.1 million tons in December, up 15 percent from the prior month, 13 percent year-over-year, and the highest since August 2010.

- China’s December coal imports hit a new record of 36.3 million tons, up 25.3 percent month-over-month, and up 35.5 percent from the prior year, and, as a result, imports for all of 2012 jumped to 290 million tons (+30.4 percent from 2011).

Weaknesses

- The CRU Weekly assessment shows the benchmark steel price at $624 per short ton, down $11 per ton for week ending January 16, and following a $4 per ton drop last week. This is compared to fourth quarter and third quarter averages of $615 per ton and $638 per ton.

- Rio Tinto replaced CEO Tom Albanese after the company reported a $14 billion impairment charge for 2012. The impairment charges include approximately $3 billion relating to Mozambique coal operations, and a $10-11 billion reduction in the carrying value of aluminum assets.

- Very large crude carriers from the Middle East-to-Asia route fell the most since November 28, sliding 12 percent to $11,595. Rates are down 30 percent since the start of the year and resumed a decline after gaining yesterday for the first time since December 19.

Opportunities

- BP's Energy Outlook highlights the importance of emerging markets as non-OECD economies constitute 90 percent of population growth, 70 percent of GDP growth, and 93 percent of energy consumption growth to 2030. While non-OECD energy consumption is expected to grow by 61 percent from 2011 to 2030 and rise on a per capita basis by 1.5 percent per year, OECD energy consumption is expected to grow by only 6 percent and fall on a per-capita basis by 0.2 percent per year.

- Chile’s copper output is expected to reach 5.8 million tons in 2013 versus 5.4 million tons last year and 5.2 million tons in 2011, according to Sonami Mining Association. The country is seen attracting $100 billion in mining investment in the next 10 to 12 years.

Threats

- Europe continues to threaten global growth as the Bank of Italy slashed its forecast for the country's shrinking economy on Friday. The central bank said it now expects GDP to slump by 1.0 percent this year rather than the 0.2 percent contraction it forecast in July.

Emerging Markets

Strengths

- China’s fourth-quarter GDP grew 7.9 percent, better than the 7.8 percent estimate and up from 7.4 percent for the third quarter. December industrial production grew 10.3 percent versus the consensus of 10.2 percent, and up from 10.1 percent in November. Retail sales were 15.2 percent versus the consensus of 15.1 percent, up from 14.9 percent in November and the highest in the last 10 months. Fixed asset investments in December rose 20.6 percent, versus the consensus of 20.7 percent. Finally, power output rose to 432.7 kilowatt hour in December, a four-month high. Those numbers confirmed China’s growth recovery has momentum coming into 2013.

- The Bank of Thailand, the central bank, revised its forecast for GDP growth this year to 4.9 percent from 4.6 percent, citing strong domestic demand, especially private investment. Infrastructure projects connecting within the country and with Myanmar and urbanization in northern Thailand are catalysts for developers and construction engineering and materials businesses.

- Chinese A-share defense names declined on Thursday, indicating Chinese investors expected no military clash with Japan over disputed islands in the East China Sea.

- The Philippines’ manufacturing production index grew 9.6 percent in November last year, with structural catalysts in fiscal spending and upbeat consumption.

- Citigroup expects China A- and H-shares to rise 15-20 percent more in the first half of 2013, while UBS expects A-shares to rally 20 percent in 2013.

- Turkey’s economy is clearly accelerating: the Purchasing Managers’ Index (PMI) reading is at 53, December industrial production was 11.3 percent higher than last year, and annualized credit growth is now around 20 percent.

Weaknesses

- China’s GDP grew 7.8 percent in 2012. It was the lowest in the last 13 years, though the highest growth rate in the world. Essentially, China is entering a modest high growth stage.

- China’s Ministry of Railway announced its 2013 railway infrastructure investment target of 520 billion renminbi (RMB), up 1 percent from 2012, slightly below the market expectation. Nevertheless, a large proportion of China’s infrastructure investments are still in highways and urban transit improvements.

- Jakarta was flooded this week with more than 200,000 people displaced from their homes and businesses halted, showing the need for infrastructure improvement.

- The Thai policy rate was expected to remain unchanged at 2.75 percent, though no inflation risk is expected.

- Smog in Beijing was so bad that people had to put on masks to walk in the street, but it also drove up environment-related stock prices.

Opportunities

- The chart above shows that floor space sold has been leading floor space started since summer last year in China. With the running down of inventory and shrinking supply, demand and supply are reaching equilibrium, which will be supportive to housing sales and prices, and hence the stock price of H-share developers.

- China’s final consumption contributed 51.8 percent of GDP growth in 2012, while the contribution of net goods and services exports was negative 2.2 percent, according to China’s statistics, which showed progress in China’s transition to a consumption-driven economy.

- Historically, emerging markets dividend yields have largely been in line with the developed world. But dividend growth has cumulatively been stronger in emerging markets. The compound annual growth rate (CAGR) since 2004 was 8.3 percent in emerging markets and 4.8 percent in developed markets.

Threats

- Pollution in China, as demonstrated by Beijing’s smog this week, resulted in increased costs in health and economic growth. China may tighten pollution criteria, which is good for long-term development, but negative for auto and manufacturing sectors in the short term.

- Russian GDP has been decelerating since the second quarter of 2012. The December data out next week will likely present a picture similar to the previous month.

- Industrial production in Poland dropped 12.2 percent in December, another signal to ease policy. As in the U.K., most loans in Poland are not fixed rate but floating, which means banks will be hurt and not helped by lower interest rates.

© US Global Investors