- The National Association of Home Builders' Housing Market Index has staged a record-breaking run higher.

- Home prices have been rising and are feeding into real mortgage rates, consumer confidence, household net worth … and pushing fence-sitters off the fence.

- Housing's contribution to job growth could push the unemployment rate down more quickly than many believe.

A year ago I penned a report titled, "Rock Bottom: Housing May Have Already Hit It." It's time for another housing update given the tremendous amount of progress toward recovery since then. This report, as typical of my housing-related reports, is quite a bit more chart-heavy than usual, but the pictures are compelling … and telling.

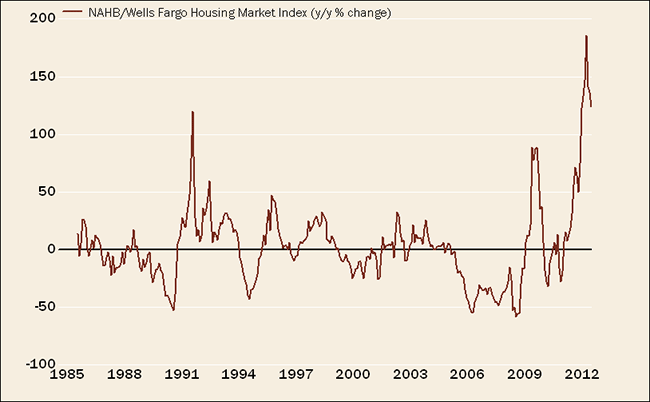

Some long-time readers may recall my pessimistic writings about housing in 2006—notably my September 2006 report titled, "Housing: ARMed and Dangerous." One of the key indicators that troubled me most at that time was the Housing Market Index from the National Association of Home Builders (NAHB). We were in the midst of what at that time was an unprecedented drop in that measure of homebuilder sentiment. Up until then, the HMI and stock market were also fairly tightly correlated with about a one-year lag, which is why we were also quite pessimistic about both the economy and the stock market looking ahead.

HMI on a tear

So, how's the HMI been faring more recently? After an unprecedented drop during the bursting of the housing bubble, it recently staged a record-breaking move higher in percentage terms, as you can see below. Its level is now 47 (seen in two charts at the end of this report)—the highest reading since April 2006. It was the eighth consecutive increase, the longest streak ever. Notable strength was seen in the Northeast in the aftermath of Hurricane Sandy.

HMI's Record-Breaking Surge

Source: FactSet, National Association of Home Builders, as of December 31, 2012.

Caveat: The huge surge in the HMI has helped elevate optimistic sentiment about housing's recovery. This admittedly sets up the possibility for disappointments if the trajectory falters in the near term.

NAHB's new data series

One of the NAHB's new data series incorporates employment, house prices and housing permits for 385 metro areas in the United States. Just after the downgrade of US debt by Standard & Poor's in September of 2011, only 12 metro areas were positive for all three components—the reading for this January had 242 positive for all three.

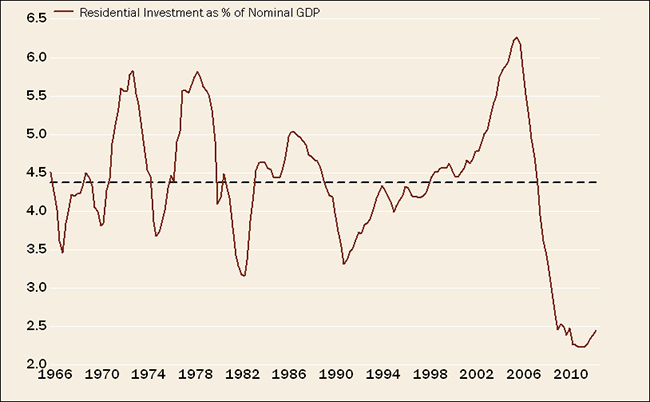

Many of my more-macroeconomic reports the past few months have cited the positive offsets in play to counteract the deleterious effects of fiscal contraction coming this year, and housing has been key among them. It begs the obvious question of how much of an offset housing could possibly be given its diminished weigh in US gross domestic product. As you can see in the chart below, from a high over 6% of GDP at the peak in the housing bubble, housing remains less than 3% today, though it is working its way up from the bottom.

Housing Has Bottomed as % of GDP

Source: Bureau of Economic Analysis, FactSet, as of September 30, 2012. Dotted line represents average.

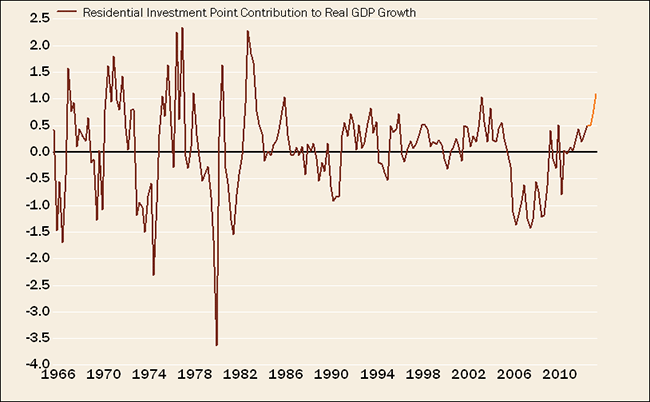

As an impact on GDP growth, the numbers are a tad more compelling—a testament to just how strong the housing recovery has become. In the chart below, you can see the recent trajectory of housing's contribution to GDP, inclusive of ISI Group's forecast over the next few quarters. In an economy that continues to grow at a pace below trend, the lift from housing will become very important.

Housing's Growing Contribution to GDP

Source: Bureau of Economic Analysis, FactSet, ISI Group, as of September 30, 2012. Orange line represents estimates from the fourth quarter of 2012 through the third quarter of 2013, courtesy of ISI Group.

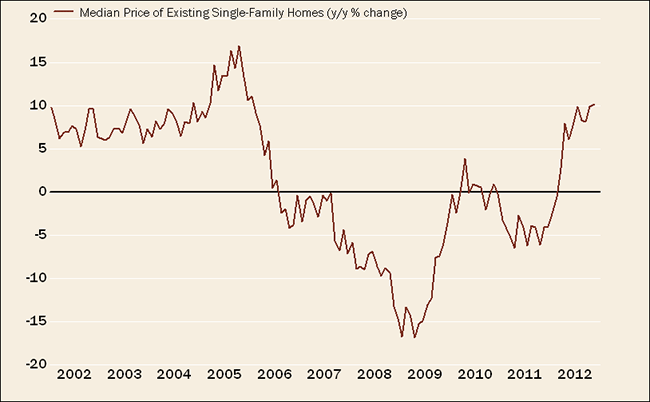

Prices and the feeder mechanism

We're clearly seeing an improvement in home prices, which is feeding into several important areas, including real mortgage rates (see below), consumer confidence and household net worth, while also pushing fence-sitters off the fence.

Home Prices Well Up From Lows

Source: FactSet, National Association of Realtors, as of November 30, 2012.

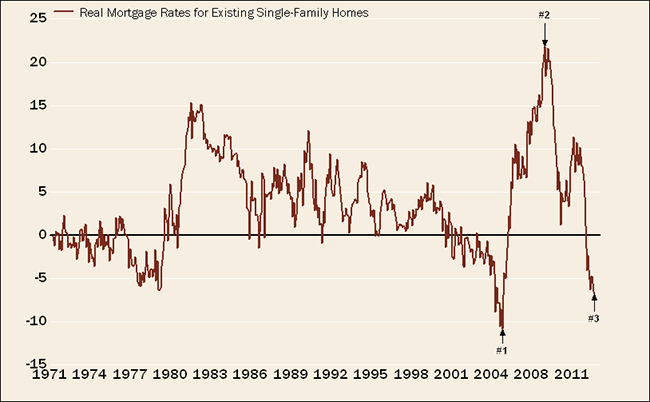

The aforementioned effect on real mortgage rates is probably one of the most important forces under housing's improvement. It's a concept I've discussed and written about for years, and it's always worth an update in these reports. Just like "real" GDP is the difference between nominal GDP and inflation, the real mortgage rate is the difference between nominal mortgage rates (e.g., the 30-year fixed rate) and the rate of inflation (or deflation) in home prices. After all, the rate at which we can borrow to buy a house isn't the only crucial factor; another is what's happening to the price of the asset we're borrowing to buy.

Real Mortgage Rates Have Plunged

Source: FactSet, Federal Reserve, National Association of Realtors, as of November 30, 2012.

Let me explain the chart above for those new to the concept. It's a chart of the real mortgage rate over the past 40+ years. At the peak of the housing cycle in 2005 (point #1), nominal mortgage rates were around 6% and homes were appreciating at about a 17% annual rate. That meant real mortgage rates were a record-low -11% [6% - 17% = (11%)]. In other words, you could borrow at a 6% rate to buy a home appreciating at a 17% annual rate … a pretty good deal.

Fast-forward to point #2, during the trough in the housing cycle during the recession in 2009. At that point mortgage rates had begun to retreat—but so had home prices. With rates around 5%, but homes depreciating at a 17% annual rate, the math became ugly [5% - (17%) = 22%]. That's why I thought it was remarkable there were so many prognosticators at that time who felt that if the Fed could just engineer mortgage rates even lower it would help initiate the healing process.

Indeed, lower rates have helped, but the real key to recovery was getting the asset to stop depreciating. Prices were the part of the equation that was most damaged during the housing bust.

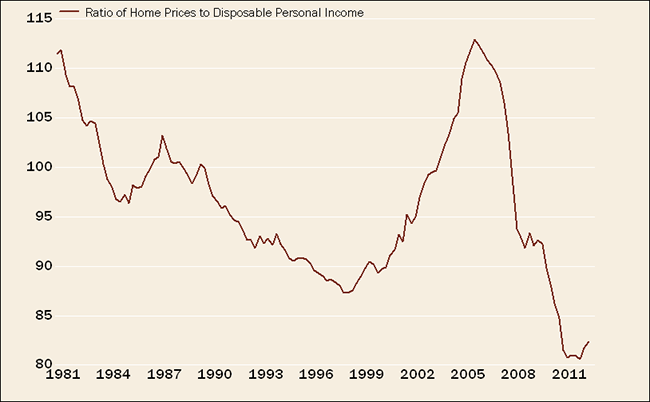

Today, mortgage rates have descended toward 3% while prices are increasing again at a double-digit pace. As seen at point #3, the real mortgage rate has gone back into negative territory—a very good thing for demand. And homes remain very cheap relative to income levels, suggesting a prop of support that likely won't wane for some time.

Homes Cheap Relative to Income

Source: FactSet, Federal Finance Housing Board, as of September 30, 2012.

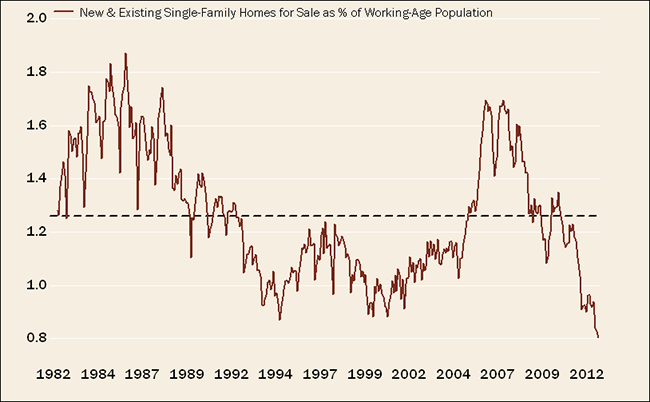

Inventories have plunged

Another reason prices have recovered so nicely is that inventories have fallen to record low levels, particularly relative to the working-age population, as you can see below.

Rock-Bottom Inventories

Source: FactSet, National Association of Realtors, Organization for Economic Cooperation and Development, US Census Bureau, as of November 30, 2012. Dotted line represents average.

Source: FactSet, National Association of Realtors, Organization for Economic Cooperation and Development, US Census Bureau, as of November 30, 2012. Dotted line represents average.

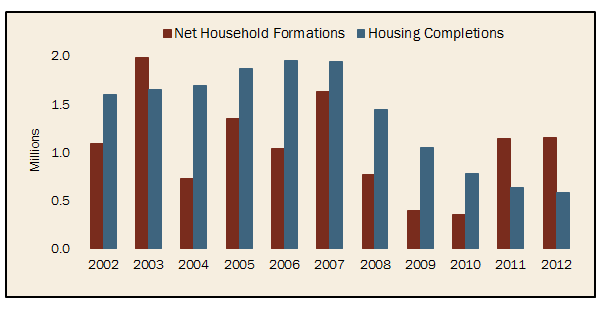

Boomerang effect waning

Household formations are also moving back up again. For those of you with "boomerang" kids that moved back in after college due to the sluggish economy, this is good news indeed. As the economy has improved, so has the economic incentive to start a household by moving out of your parents' home and/or kicking out your two roommates with whom you share a one-bedroom apartment.

As you can see in the chart below, although formations have been surging off the lows, housing completions have not been keeping pace—meaning we're building a significant demand-supply imbalance that should support sales and prices for some time. Rising demand with still-weak supply additions will also support mortgage lending, which has picked up alongside overall bank lending, recently growing at a 6% annual rate.

Home Completions Lagging Household Formations

Source: FactSet, ISI Group, US Census Bureau, as of December 31, 2012.

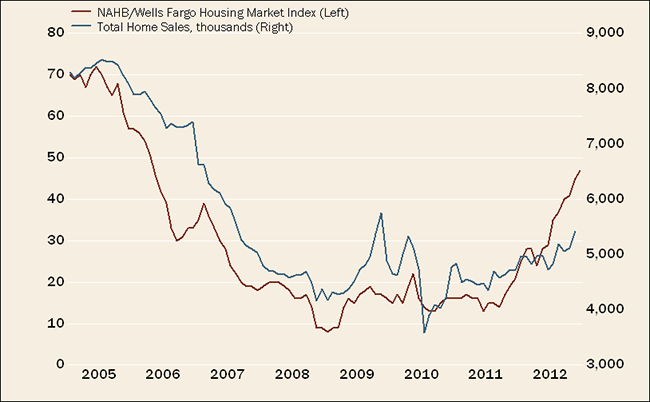

Ending where I started, let's look again at the surge in the HMI—this time, we'll look at the level, not the percentage change. Over time, movements in the HMI have correlated very closely with movements in home sales and, most importantly, jobs (with a lag). The chart below suggests we still have a bit of catch-up to do in terms of home sales—a very healthy sign for this year.

HMI Surge Suggests Higher Home Sales

Source: FactSet, National Association of Home Builders, National Association of Realtors, US Census Bureau. HMI as of December 31, 2012. Total home sales (existing and new) as of November 30, 2012.

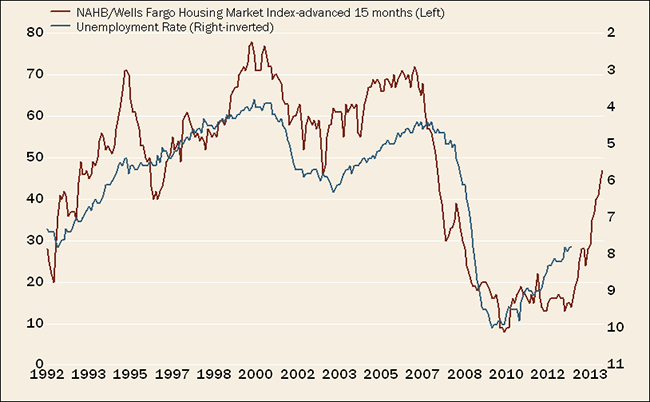

We're are also now in the sweet spot in the relationship between the HMI, which tends to improve first, and the unemployment rate, which tends to follow with about a 15-month lag. Assuming the two remain closely aligned, we should continue to see a nice downward trajectory in the unemployment rate.

HMI Surge Suggests Higher Employment

Source: Department of Labor, FactSet, National Association of Home Builders, as of December 31, 2012.

Housing has bottomed, and we're heading into the typically strongest part of the home-buying season (spring). The multiplier effects are powerful and beginning to gain traction. There remain naysayers, but a lot fewer than there were a year ago.

For what it's worth, if the recent pace of improvement in the unemployment rate continues, we'll get to the Fed's unemployment-rate threshold of 6.5% sooner than mid-2015, which is when the Fed originally thought rates would begin to rise. We'll undoubtedly write more on this topic this year, but in the meantime, keep it as food for thought.

Important Disclosures

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

© Charles Schwab