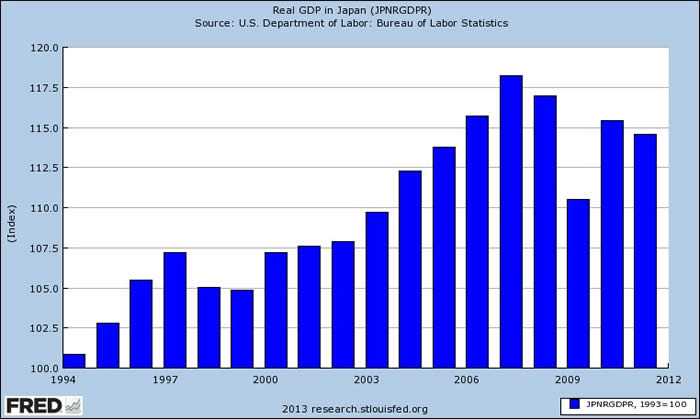

Yes, you knew we were going to talk about Japan. It's all the rage and the big standout in market performance in the last few weeks. Since November the broad Nikkei-225 average has risen 24% because there's new thinking in town. It's hard to describe Japan's 20 year malaise. Once proud companies shaken, the shattering of a property market and total collapse of stocks. Even if the market rises at the same level of the last few months, it will take six years to re-reach its peak. A more reasonable 10% growth rate will take 14 years. Weird things happen when economies enter deflation. Real growth of 2% with a deflator of 2% allows 4% revenue increases. And if you click along at that rate then GDP growth looks like this:

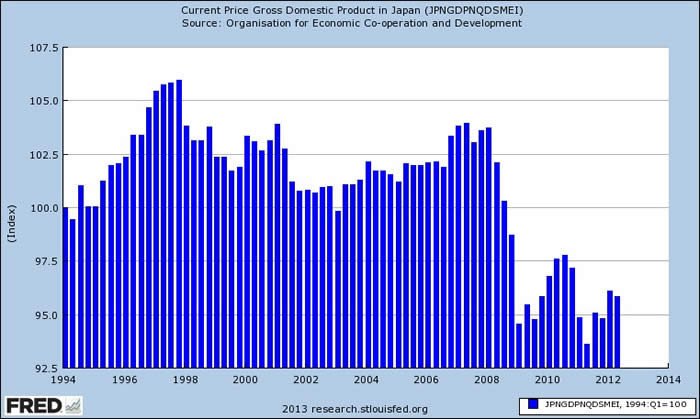

Which is the headline story in Japan and kind of looks ok. But if real growth is 2% and there is more and more price deflation, then real growth looks unchanged but your nominal growth looks like this:

Source: Federal Reserve Bank of St. Louis, Economic Research

Which is 20 years of catastrophe. No one wants to lend in deflation. The real value of any long-term obligation increases and collateral values decrease. Professor Bernanke was very worried about this in 1999 when he talked about Japan's liquidity trap, output gap and the dangers of zero inflation. What he didn't point out was that this also gets particularly dangerous when there is a large, moneyed rentier class that in the absence of higher nominal rates, demands price deflation. And that usually strangles any nominal growth bursts at birth. Bernanke also went on to recommend a close collaboration of theMOFandBOJ. That's something that never happened and explains why he urges policymakers in the US to do the same.

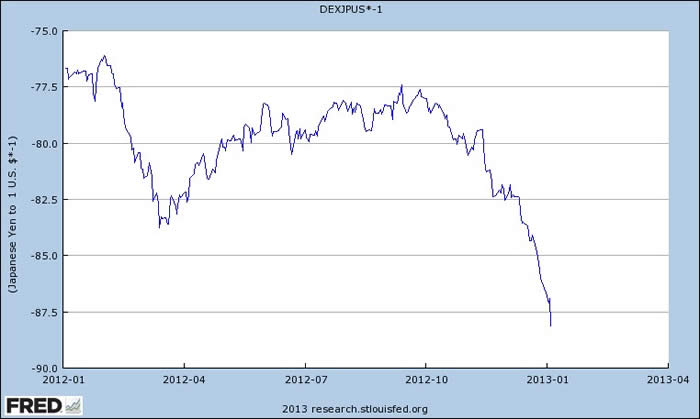

But wind on to today. There's an unfolding strategy of Abenomics, named after the new Prime Minister, who campaigned on i) getting the BOJ to buy eurozone denominated bonds to weaken the yen ii) a higher inflation target in the form of an “anti deflation” program and iii) a large fiscal stimulus plan. Last week this was announced as a ¥10tr ($117bn) stimulus with added local government and private sector programs to lift the entire package to ¥20tr or around 3.8% of GDP. Stimulus packages have come and gone in Japan before but this one is different because of size, the lift to confidence, the parliamentary super majority and the yen. Here's the latest on the yen:

Source: Federal Reserve Bank of St. Louis, Economic Research

For the first time in years, we have clear guidance on a policy to competitively devalue the yen. This helps the economy greatly at time when both trade and current account surpluses are under pressure (and yes, there are limits to FX manipulation). Some are worried about the potential loss of central bank independence in all this. We're not. The bank has seen a nail in every problem for the last 20 years and applied the same hammer every time. They've worn out their stay. If relationships between fiscal and monetary authorities are dynamic over time, then this is overdue. So for now we like the triple play in Japan: easy money, fiscal expansion and growth.

Two Central Banks

The Fed remains steady and despite theFOMCminutes from a few weeks ago is on a dovish, accommodatory course. Last week we had presidents Bullard of the St. Louis Fed and George of Kansas again raise the risk of inflation. Bullard's approach is to keep inflation forecasts at the top end of the range. The St. Louis forecast forPCEis 2.0% compared to the Fed's 1.5% to 2.0% range. He also curiously stated that the FOMC can not target unemployment which is spiritually, if not semantically, at odds with the “foster maximum employment and price stability” mandate that precedes every FOMC minutes. George's comments are more traditional balance sheet imbalance issues which we don't buy into because money bought by any central bank need never be released. Sure, any high powered money will add to bank reserves and allow them to expand liabilities through loans. But if loan demand isn't there, then the cycle of excess money to inflation can never start.

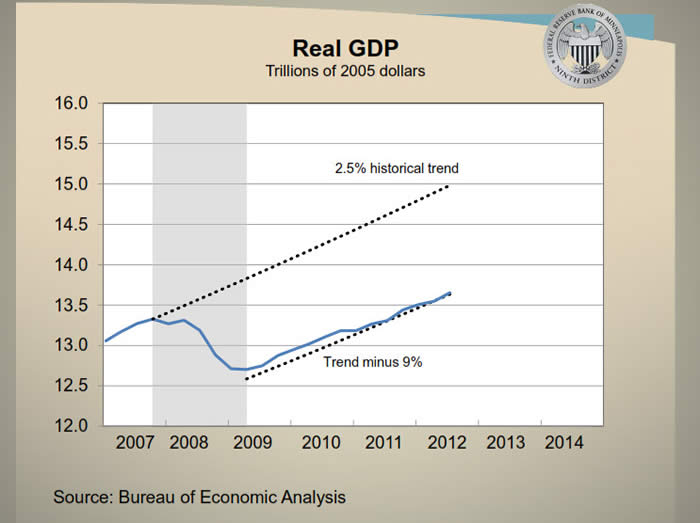

Much closer to the mark is hawk turned pragmatist Kocherlakota of the Minneapolis Fed. We like this from his presentation which clearly shows how much of an output gap the US labors under:

Source: Federal Reserve Bank of Minneapolis

And with remarkable clarity he concludes that “…if anything monetary policy is currently too tight, not too easy.” Which neatly reminds us of Friedman's point that it is fallacious to identify tight money with high rates and easy money with low rates. Today's rates suggest that may be the case with the gap between nominal GT10 and 10-yearTIPSbasically unchanged.

Source: Federal Reserve Bank of St. Louis, Economic Research

TheECBmade no changes to policy. But Draghi's tone was very upbeat. And so it should be. Since the mid-year announcements bond yields andCDSare lower, stocks up, capital inflows higher, deposits in peripheral banks up,Target2balances down and the ECB balance sheet smaller. He recognized that this has yet to flow through to the real economy and, indeed, many major economic indicators are in rough shape. But it has been quite an achievement to keep Spanish bond yields low. Last week Spain issued 2-year paper at 2.47% compared to 3.95% in October and 15-year bonds at 5.55% compared to 5.76%. It's probable that we have seen the last of rate action for a while but this at least puts a floor under more worries in the banking sector and should also underpin the spectacular equity gains we've seen in recent months.

US

It was generally a quiet week for economic stats. TheNFIBwas pretty bad but at least didn't worsen. Small business took it on the chin for pre-cliff uncertainty and they're not about to start hiring or building out inventory of any kind. Trade was a bigger deficit than it has been in seven months and saw a big jump in imports of consumer goods, particularly of cell phones (not from China!) and autos, possibly post Sandy replacements. The net result is a possible downside revision of Q4GPD of around 0.4%. But December trade numbers are still a month away.

Bonds and Equities

Yields stayed between 1.85% and 1.95%. New issue flows have eased as we go into the reporting cycle. We seem to be flat. Equities remain well pinned. The big story in equities remains dividend growth and, no, don't give up on it. An average stock with an average 10% growth rate in dividends will end up with a running yield of 3.5% in five years. Even assuming no change in price, that's a return that will not come through bonds. In last year's search for yield (always a bad strategy), high dividend stocks performed well. But we currently see dividend growth stocks trading at their biggest discount to high dividend stocks in at least two decades.

Bottom Line: Fine with a moderate overweight to equities and corporates even at the 1470 level. So far earnings have been good, especially from some financials where we see growth in fee income, expense control, growing capital ratios and a surprisingly stable mortgage banking resurgence.

Sources: Bloomberg, Bureau of Economic Analysis, Bureau of Labor Statistics, Capital Economics, Congressional Budget Office, CRT Ader, Federal Reserve Bank of St. Louis, Federal Reserve Board, FT Alphaville, FT Money Supply, High Frequency Economics, ISM Chicago, J.P. Morgan Market Intelligence, Pantheon MacroEconomic Advisors, TrendMacro, Citigroup Capital Markets, Federal Reserve Bank of Minneapolis, Sentinel Asset Management, Inc.

© Sentinel Investments